Can You Get Money Back On A Fha Loan

The possibility of recouping funds after closing on a home with an FHA loan is a question weighing heavily on the minds of many homeowners and prospective buyers. While not a straightforward refund, certain circumstances and programs can lead to homeowners receiving money back or reducing their overall housing costs.

Understanding the nuances of FHA loans, including refinancing options, escrow account management, and potential refunds after paying off the mortgage, is crucial for navigating the complexities of homeownership. This article delves into the specific situations where homeowners might be eligible for financial returns related to their FHA loan, providing a comprehensive overview of the process.

Understanding FHA Loan Basics

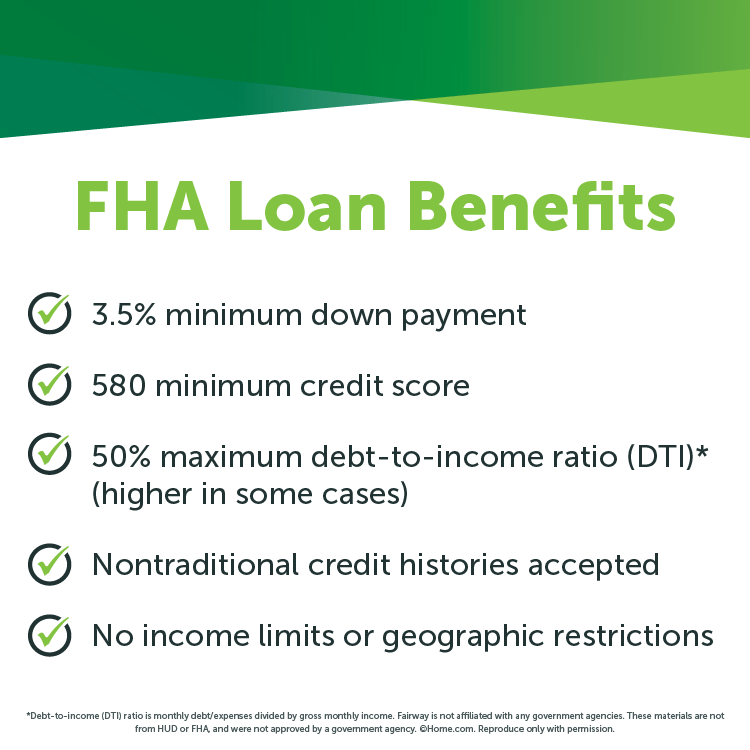

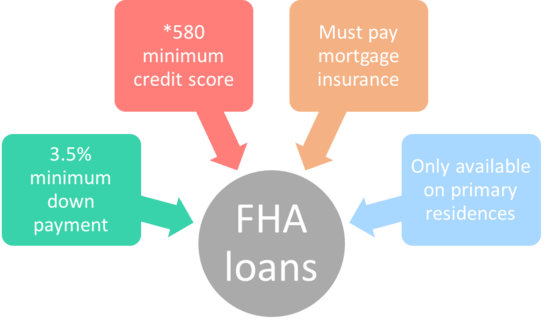

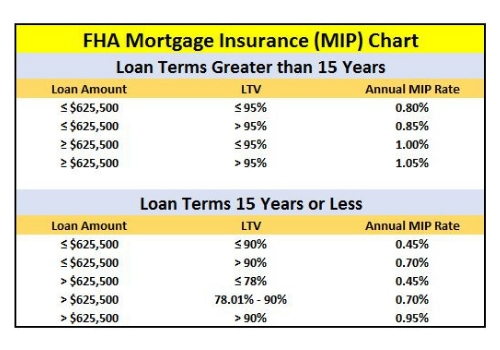

FHA loans, insured by the Federal Housing Administration, are designed to make homeownership accessible, particularly for first-time buyers and those with limited down payments. These loans often require mortgage insurance premiums (MIP), which protect the lender if the borrower defaults.

The upfront MIP is typically financed into the loan, while an annual MIP is paid monthly as part of the mortgage payment. These premiums are a significant factor in the overall cost of an FHA loan.

Refinancing for Potential Savings

One common way to potentially receive money back or lower housing costs with an FHA loan is through refinancing. If interest rates have decreased since the original loan was obtained, refinancing to a lower rate can reduce monthly payments and overall interest paid over the life of the loan.

Homeowners can also explore refinancing from an FHA loan to a conventional loan if they have built sufficient equity in their homes and meet the lender's credit requirements. This can eliminate the need for MIP, leading to substantial savings.

Escrow Account Management and Refunds

FHA loans often involve escrow accounts to cover property taxes and homeowner's insurance. Lenders collect these funds monthly as part of the mortgage payment and then pay the expenses on behalf of the homeowner.

If the amount collected in the escrow account exceeds the actual expenses, the lender is required to refund the overage to the borrower. These refunds are usually issued annually after an escrow analysis.

Escrow Analysis Explained

An escrow analysis ensures that the lender is collecting the correct amount to cover property taxes and insurance. If the analysis reveals a surplus, the lender must refund the excess funds to the borrower within a specified timeframe.

Conversely, if there is a shortage, the lender may increase the monthly escrow payment to cover the deficit. Homeowners have the right to review their escrow account statements and dispute any discrepancies.

Mortgage Insurance Premium (MIP) Refunds

The rules regarding MIP refunds have evolved over time. For FHA loans originated before 2013, the annual MIP was typically refundable on a pro-rated basis if the loan was paid off or refinanced within the first few years.

However, for FHA loans originated after 2013, the rules changed, making MIP less likely to be refundable. For most loans originated after this date, the annual MIP is required for the life of the loan or until the loan-to-value ratio reaches a certain threshold, depending on the loan terms.

The specific refundability of MIP depends on the date the loan was originated and the loan terms. Contacting the FHA or the loan servicer can provide clarity on individual eligibility.

Claiming Refunds After Paying Off the Loan

After paying off an FHA loan, homeowners may be eligible for a partial refund of the upfront MIP if certain conditions are met. Typically, this requires the loan to be paid off within a specific timeframe, such as within three years of origination.

The refund amount is calculated based on the remaining unearned portion of the upfront MIP. To claim the refund, homeowners must contact the FHA directly and provide documentation verifying the loan payoff.

It's important to note that the process for claiming an MIP refund can be complex and may require specific documentation.

Potential for Legal Recourse in Cases of Misconduct

In rare instances, homeowners may be entitled to compensation if they have been victims of lender misconduct or predatory lending practices related to their FHA loan.

Such cases might involve inflated appraisals, hidden fees, or misrepresentation of loan terms. Consulting with a real estate attorney can help homeowners understand their legal options.

Staying Informed and Seeking Professional Advice

Navigating the intricacies of FHA loans and potential refunds requires staying informed and seeking professional advice. Homeowners should regularly review their loan statements, escrow account statements, and any communications from their loan servicer.

Consulting with a mortgage professional, financial advisor, or real estate attorney can provide personalized guidance based on individual circumstances. Understanding your rights and responsibilities as a homeowner is crucial for maximizing financial benefits and avoiding potential pitfalls.

While directly getting "money back" on an FHA loan isn't always guaranteed, strategic refinancing, careful escrow management, and understanding MIP refund possibilities can lead to significant savings and financial returns for homeowners. Proactive engagement with loan terms and available resources is key to achieving the best possible outcome.

:max_bytes(150000):strip_icc()/FHAnew-V1-a128f12bf4584ae8a9a5b7d0214cd8e4.png)

:max_bytes(150000):strip_icc()/whats-difference-between-fha-and-conventional-loans_final-ede6be99eeb344c0860e12ba19c41bff.png)

/text-sign-showing-hand-written-words-fha-home-loan-1179800155-9e745cb5bb5f49279651d7a9e76096ac.jpg)