Direct Payday Loan Lenders No Credit Check

The allure of quick cash without the hassle of traditional credit checks has fueled the rise of direct payday loan lenders. These lenders promise immediate financial relief, but their practices are drawing increased scrutiny from consumer advocates and regulators alike.

This article delves into the world of direct payday loan lenders offering "no credit check" loans, exploring their operational methods, the risks they pose to borrowers, and the ongoing debate surrounding their regulation. Understanding the intricacies of these loans is crucial for consumers seeking short-term financial solutions.

What are Direct Payday Loan Lenders?

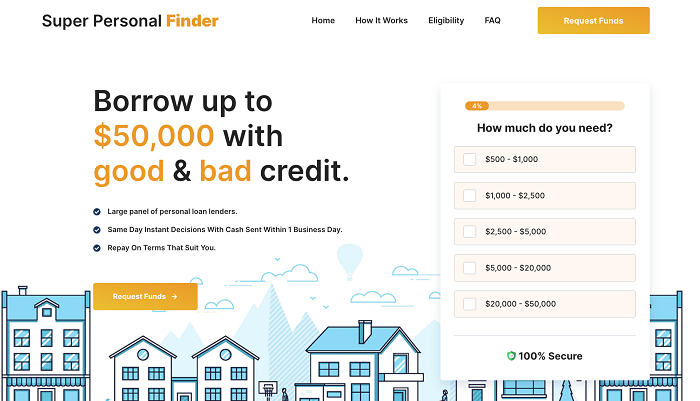

Direct payday loan lenders provide small, short-term loans directly to borrowers, bypassing intermediaries like loan brokers. They often advertise "no credit check" loans, suggesting that credit history is not a factor in loan approval.

This contrasts with traditional lenders, such as banks and credit unions, which typically conduct thorough credit checks before approving loans. The apparent ease of access is a major draw for individuals facing urgent financial needs, especially those with poor or limited credit.

The "No Credit Check" Claim: What Does It Really Mean?

While these lenders may advertise "no credit check," it's important to understand that this doesn't necessarily mean no assessment of the borrower's ability to repay. Instead, they often rely on alternative methods of evaluation.

These methods may include verifying income through pay stubs, bank statements, or employment verification. Some lenders might also access databases that track short-term lending activity, allowing them to see if an applicant has outstanding loans with other payday lenders.

The Risks Associated with Direct Payday Loans

The convenience of direct payday loans comes at a significant cost. The primary risk is the exceptionally high interest rates and fees associated with these loans.

According to the Consumer Financial Protection Bureau (CFPB), payday loans often carry Annual Percentage Rates (APRs) of 400% or higher. These exorbitant rates can quickly trap borrowers in a cycle of debt, where they are forced to take out new loans to cover existing ones.

Another significant risk is the short repayment period, typically just a few weeks. This leaves borrowers with limited time to gather the necessary funds, increasing the likelihood of default and additional fees.

Predatory Lending Concerns

Consumer advocacy groups like the National Consumer Law Center (NCLC) have long criticized payday lenders for engaging in predatory lending practices. They argue that these lenders target vulnerable populations, trapping them in debt cycles and exacerbating their financial difficulties.

The "no credit check" aspect, while seemingly beneficial, can mask the true cost and risks associated with these loans. Borrowers may not fully understand the terms and conditions until it's too late.

Regulation and Legal Landscape

The regulation of payday lenders varies significantly from state to state. Some states have banned payday lending altogether, while others have strict regulations on interest rates and loan terms.

The CFPB has also attempted to implement federal regulations on payday lending, but these efforts have faced legal challenges and regulatory changes. The current regulatory landscape remains complex and evolving.

Ongoing debates focus on the need to balance consumer protection with access to credit, particularly for individuals who may have limited options. Critics argue that stricter regulations are needed to prevent predatory lending practices and protect vulnerable borrowers.

Alternatives to Payday Loans

For individuals facing urgent financial needs, exploring alternatives to payday loans is crucial. These alternatives may include:

- Personal Loans: Offered by banks and credit unions, personal loans typically have lower interest rates and longer repayment terms than payday loans.

- Credit Card Cash Advances: While still carrying high interest rates, cash advances may be a better option than payday loans for some individuals.

- Borrowing from Friends or Family: This can be a less expensive option, but it's important to establish clear terms and repayment plans.

- Seeking Assistance from Local Charities or Non-Profits: Many organizations offer financial assistance and counseling services to individuals in need.

It is important to consider the long-term financial implications of taking out any loan. Careful budgeting, financial planning, and exploring alternative solutions can help individuals avoid the debt trap associated with high-cost payday loans.

The Future of Direct Payday Lending

The future of direct payday lending is uncertain, with ongoing legal and regulatory challenges. Increased scrutiny from consumer protection agencies and growing awareness of the risks associated with these loans may lead to further restrictions and changes in the industry.

As consumers become more informed about the alternatives available and the potential dangers of payday lending, the demand for these high-cost loans may decline. However, the need for short-term financial solutions will likely remain, highlighting the importance of developing responsible and affordable lending options.

Ultimately, informed decision-making and responsible financial practices are crucial for navigating the complex landscape of short-term lending and avoiding the pitfalls of predatory lending.

![Direct Payday Loan Lenders No Credit Check 1 Hour Payday Loans No Credit Check | [year] Guide](https://avocadoughtoast.com/wp-content/uploads/2022/02/1-Hour-Payday-Loans-No-Credit-Check.png)