Guaranteed Approval Payday Loans No Credit Check

The allure of quick cash can be irresistible, especially when facing unexpected financial emergencies. But promises of "Guaranteed Approval Payday Loans No Credit Check" are rapidly becoming a siren song, luring vulnerable individuals toward potentially devastating debt traps. These types of loans, heavily advertised online and in some storefronts, circumvent traditional lending practices, raising serious concerns about consumer protection and long-term financial stability.

This article will delve into the mechanics of guaranteed approval payday loans, exploring the inherent risks, regulatory landscape, and potential alternatives. We will examine why these loans are marketed so aggressively, who they target, and the devastating consequences they can inflict on borrowers already struggling with financial hardship. Finally, we will look at what borrowers need to know, and the potential impact of this lending model on the broader financial system.

What Are Guaranteed Approval Payday Loans?

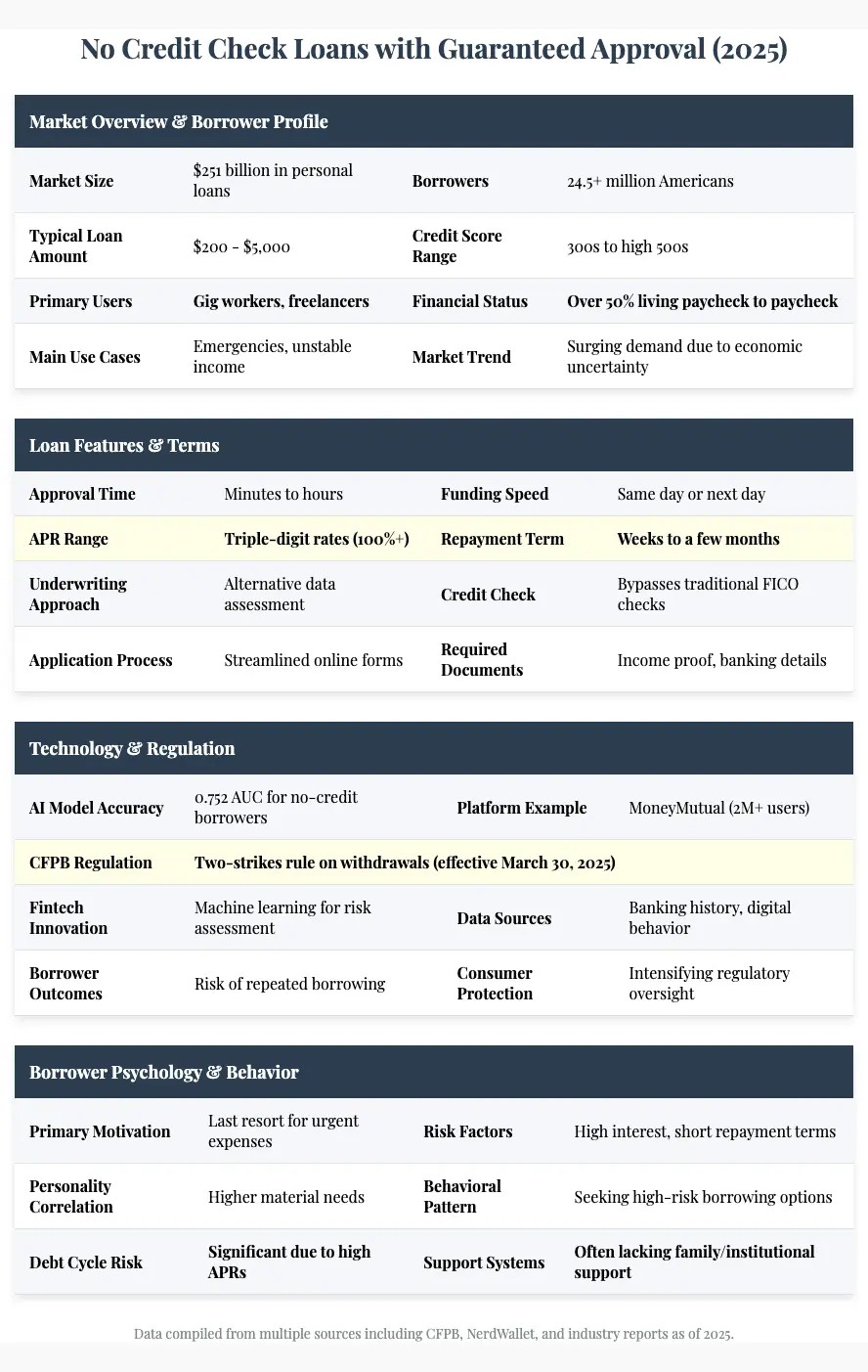

Guaranteed approval payday loans are short-term, high-interest loans marketed to individuals with poor or nonexistent credit histories. The core promise is simple: regardless of your credit score, you will be approved for a loan. This is often framed as a lifeline for those who cannot access traditional credit due to past financial missteps.

These loans bypass traditional credit checks, relying instead on factors such as proof of income and a bank account. The amounts are typically small, ranging from a few hundred to a thousand dollars, and are intended to be repaid on the borrower's next payday.

The catch? Exorbitant interest rates and fees that can quickly spiral out of control.

The High Cost of "Guaranteed Approval"

The absence of a credit check doesn't translate to a borrower-friendly deal. In fact, it often masks predatory lending practices. Payday loans, in general, are infamous for their high Annual Percentage Rates (APRs), sometimes exceeding 300% or even 400%.

When lenders offer "guaranteed approval," they are essentially accepting a higher risk of default. To compensate, they drastically inflate interest rates and tack on a variety of fees, including origination fees, late payment fees, and rollover fees. These fees can quickly dwarf the original loan amount.

For instance, borrowing $500 with a 400% APR means the borrower could owe hundreds of dollars in interest and fees in just a matter of weeks. This creates a cycle of debt where borrowers are forced to take out new loans to repay the old ones, digging themselves deeper into financial hardship. The Consumer Financial Protection Bureau (CFPB) has consistently highlighted the dangers of these practices.

Targeting Vulnerable Populations

The marketing of guaranteed approval payday loans often targets individuals who are already financially vulnerable. This includes low-income earners, those with damaged credit, and individuals facing unexpected emergencies, such as medical bills or car repairs. The ease of access and the promise of immediate relief can be incredibly appealing to those who feel they have no other options.

Aggressive online advertising and storefront locations in underserved communities further contribute to the problem. These lenders often capitalize on the desperation of their target audience, presenting themselves as the only solution to their immediate financial woes. Studies have shown a disproportionate concentration of payday lenders in lower-income neighborhoods and communities of color.

Predatory lending practices are often exacerbated by a lack of financial literacy. Many borrowers are unaware of the true cost of these loans and the long-term consequences of relying on them.

The Regulatory Landscape and Consumer Protection

The regulation of payday loans varies significantly from state to state. Some states have capped interest rates or banned payday lending altogether, recognizing the inherent risks to consumers. Others have more lenient regulations, allowing lenders to charge exorbitant rates and fees.

At the federal level, the CFPB has attempted to implement regulations to protect consumers from predatory lending practices. However, these efforts have faced political challenges and legal battles. The current regulatory landscape is fragmented, leaving many consumers vulnerable to abuse.

Consumer advocacy groups play a crucial role in raising awareness about the dangers of payday loans and advocating for stronger consumer protections. They provide resources and support to borrowers who are struggling with debt and work to educate the public about responsible borrowing practices.

Alternatives to Guaranteed Approval Payday Loans

For individuals facing financial emergencies, there are often better alternatives to guaranteed approval payday loans. These options may not be as readily available or as heavily advertised, but they can provide a safer and more sustainable path to financial stability.

Consider options such as credit union loans, personal loans from banks, or even borrowing from friends or family. These options typically have lower interest rates and more flexible repayment terms. Another option is to seek help from local charities or non-profit organizations that offer financial assistance.

Building an emergency fund, even a small one, can provide a crucial buffer against unexpected expenses. Even setting aside a small amount each month can make a significant difference in the long run. Credit counseling agencies can also provide valuable assistance in managing debt and developing a budget.

The Long-Term Impact

The proliferation of guaranteed approval payday loans has broader implications for the financial system. These loans can contribute to a cycle of debt that traps individuals and families in poverty. They can also undermine financial stability and hinder economic growth. The Center for Responsible Lending offers research and insights on the wider economic implications.

The high default rates associated with payday loans can negatively impact credit scores, making it even more difficult for borrowers to access traditional credit in the future. This can limit their opportunities for homeownership, education, and other investments.

Furthermore, the predatory lending practices of some payday lenders can erode trust in the financial system and discourage responsible borrowing. This can have a chilling effect on economic activity and make it harder for individuals to achieve financial security.

Conclusion

The promise of "Guaranteed Approval Payday Loans No Credit Check" is often too good to be true. While these loans may seem like a quick fix for immediate financial needs, they carry significant risks and can lead to a cycle of debt that is difficult to escape.

Borrowers should exercise extreme caution when considering these loans and explore all available alternatives. Stronger regulations, increased consumer education, and access to affordable financial services are essential to protect vulnerable individuals from predatory lending practices. Ultimately, a more responsible and equitable financial system is needed to ensure that everyone has the opportunity to achieve financial security.

As the digital landscape continues to evolve, so too must the vigilance of regulators and consumers alike. It's important to stay informed, understand the risks, and advocate for policies that promote financial well-being for all.