How Much Money Is Financially Stable

The concept of financial stability is often touted as a cornerstone of a secure and comfortable life, yet quantifying it remains a challenge. What exactly does it mean to be financially stable, and how much money does it take to achieve this coveted state? This question, while seemingly simple, is fraught with complexities, as the answer varies dramatically depending on individual circumstances, location, and lifestyle.

The definition of financial stability centers around having enough resources to meet current and future needs and wants. This includes covering essential expenses like housing, food, and healthcare, while also having a financial buffer for unexpected emergencies and the ability to pursue long-term goals. The amount required to reach this state, however, isn't a fixed number but rather a personalized equation.

The Variables at Play

Location plays a significant role. The cost of living varies dramatically from city to city and state to state, impacting the income needed to maintain a certain standard of living. For example, according to a recent report by the Economic Policy Institute, a family of four needs roughly $107,000 per year for a modest but adequate standard of living in Washington, D.C., compared to around $90,000 in Houston, Texas.

Lifestyle choices also heavily influence financial stability. Someone who prefers to dine out frequently and travel extensively will naturally require a higher income and greater savings than someone who leads a more frugal lifestyle. Individual needs, such as healthcare requirements or childcare costs, also play a critical part.

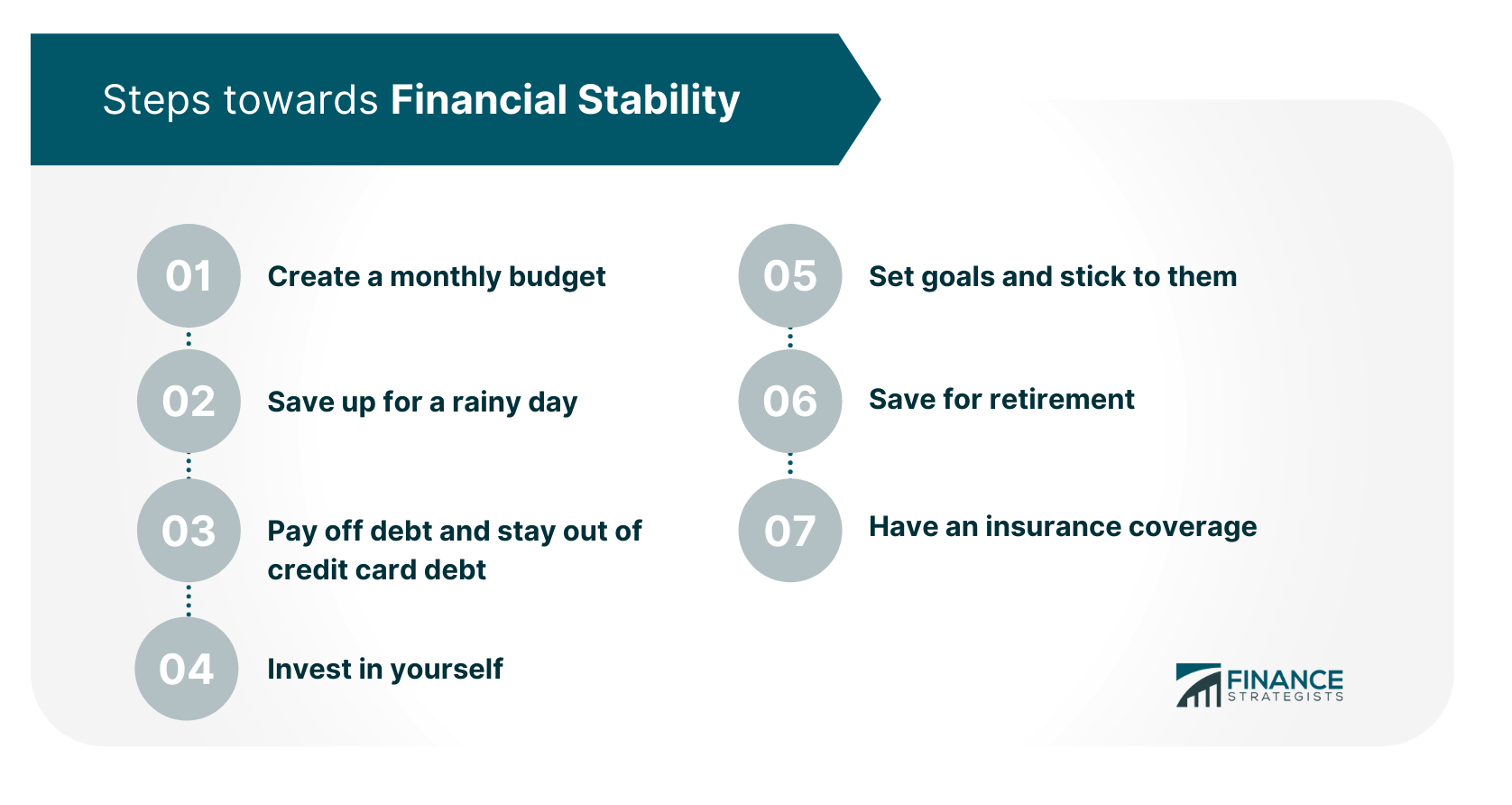

Debt is another major factor. High levels of debt, particularly high-interest debt like credit card balances, can severely undermine financial stability, even with a relatively high income. Prioritizing debt repayment is often a crucial step in achieving financial security.

Expert Perspectives

Financial advisors often suggest focusing on specific financial ratios and metrics to assess stability. One common metric is the emergency fund, which should ideally cover three to six months' worth of living expenses. This provides a cushion to weather unexpected job loss or medical emergencies.

Another key indicator is the debt-to-income ratio, which measures monthly debt payments as a percentage of gross monthly income. A ratio below 36% is generally considered healthy.

“Financial stability isn't about hitting a specific net worth number, it's about having control over your finances and being able to withstand financial shocks," says Jane Doe, a certified financial planner with XYZ Financial Services.

Saving for retirement is also a critical component of long-term financial stability. Experts generally recommend saving at least 15% of one's income for retirement, starting as early as possible to take advantage of the power of compounding. The specific amount needed will depend on individual retirement goals and expected lifespan.

Beyond the Numbers: A Sense of Security

While numerical benchmarks are helpful, financial stability also has a significant emotional component. It's about having a sense of security and peace of mind, knowing that you can manage your finances effectively and cope with unexpected challenges. This sense of security can improve overall well-being and reduce stress.

For Michael Brown, a single father of two, financial stability meant finally paying off his student loans and building a small emergency fund. "It wasn't about being rich, it was about being able to sleep at night knowing that I could take care of my kids if something happened," he said.

Financial literacy plays a crucial role in achieving and maintaining financial stability. Understanding basic financial concepts, such as budgeting, investing, and debt management, empowers individuals to make informed decisions and take control of their finances. Many resources are available to improve financial literacy, including online courses, workshops, and financial counseling services.

Conclusion

Ultimately, the amount of money required to be financially stable is a deeply personal calculation. It depends on a complex interplay of factors including location, lifestyle, debt levels, and long-term goals. Focusing on building a solid financial foundation through budgeting, saving, and debt management is essential. Striving for financial stability isn’t just about accumulating wealth; it is about securing peace of mind and building a secure future.