How To Partner With An Existing Business

Unlock rapid growth: Partnering with established businesses is your express lane to scaling up. Learn the key strategies now to expand your market reach and accelerate success.

This article provides actionable steps and crucial insights for entrepreneurs aiming to leverage existing business infrastructure. It focuses on immediate, implementable strategies to forge mutually beneficial partnerships that drive revenue and market penetration.

Identify Synergistic Opportunities

Begin by pinpointing businesses that complement your own, avoiding direct competition. Look for companies serving a similar customer base or operating in adjacent markets.

Consider their strengths, such as established distribution networks, strong brand recognition, or access to specific customer segments.

For example, a small artisanal food producer could partner with a larger grocery chain to gain wider distribution.

Craft a Compelling Partnership Proposal

Your proposal must clearly articulate the value proposition for both parties. Detail how the partnership will generate increased revenue, reduce costs, or improve operational efficiency.

Quantify the potential benefits with specific data and projections. Highlight the "win-win" scenarios created by the collaboration.

A tech startup might offer a cutting-edge software solution to a traditional company in exchange for access to their existing client base.

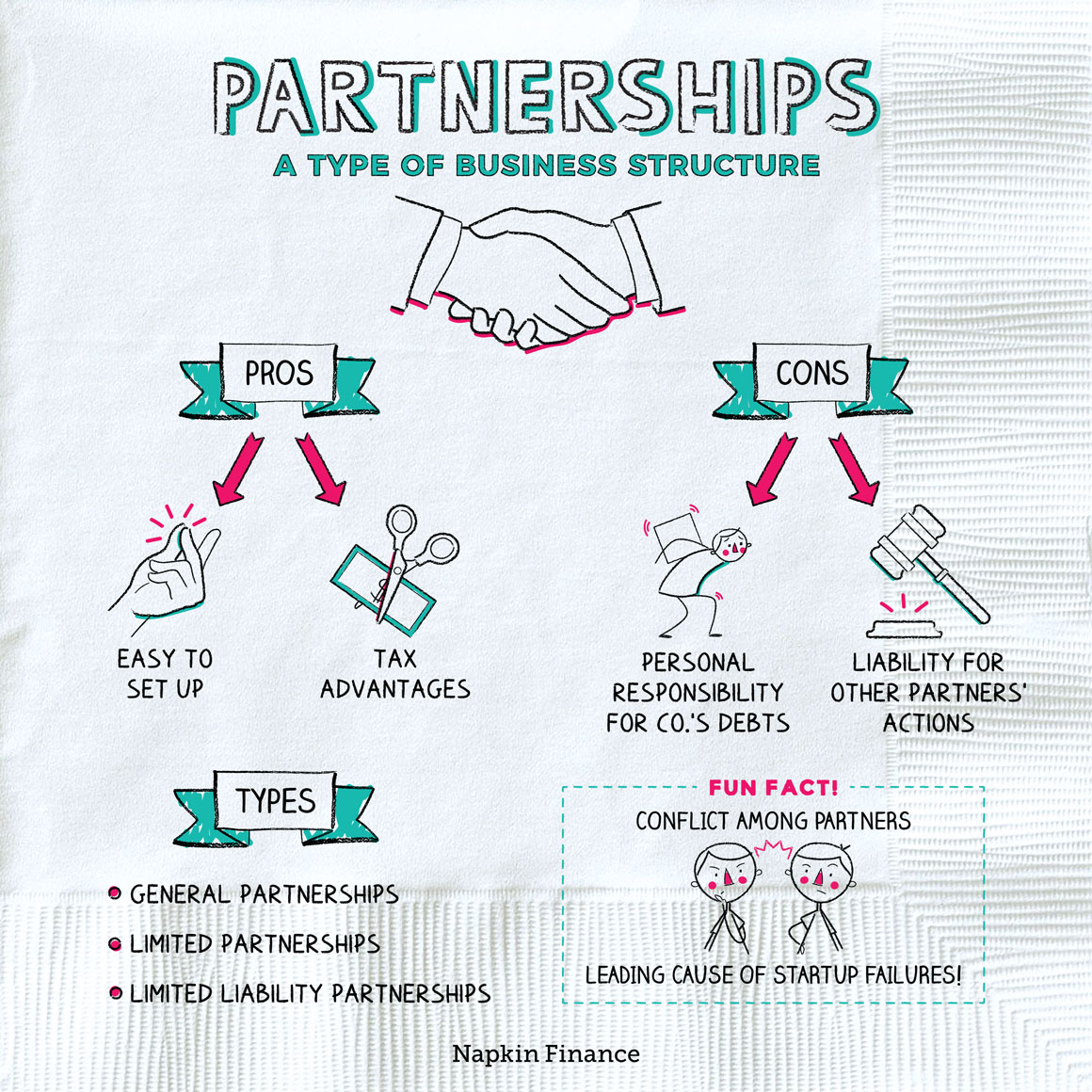

Structure the Partnership Agreement

Define the scope of the partnership with utmost clarity. Specify each partner's responsibilities, obligations, and contributions.

Address key aspects like revenue sharing, intellectual property rights, and termination clauses. Secure legal counsel to ensure the agreement is legally sound and protects your interests.

Common partnership structures include joint ventures, licensing agreements, and strategic alliances.

Negotiate Favorable Terms

Be prepared to negotiate to secure terms that align with your business objectives. Understand your leverage and the other party's priorities.

Consider offering incentives or concessions to sweeten the deal. Focus on building a long-term, mutually beneficial relationship.

Data from a Small Business Administration (SBA) study indicates that successful partnerships involve open communication and a willingness to compromise.

Implement and Monitor the Partnership

Establish clear communication channels and reporting mechanisms. Track key performance indicators (KPIs) to measure the success of the partnership.

Regularly review the partnership's performance and make adjustments as needed. Address any challenges or conflicts promptly and professionally.

According to a Harvard Business Review study, partnerships that are actively managed and monitored are significantly more likely to succeed.

Leverage Resources and Support

Utilize resources from organizations like the Chamber of Commerce and industry associations. These organizations often provide guidance and support for businesses seeking partnerships.

Attend networking events and industry conferences to connect with potential partners. Seek advice from experienced entrepreneurs and business advisors.

Consider exploring government grants and programs designed to support collaborative business ventures. The U.S. Department of Commerce offers resources for businesses seeking to expand their reach through partnerships.

Next Steps

Begin identifying potential partners today using online directories and industry databases. Develop a concise and compelling partnership proposal outlining the mutual benefits of collaboration.

Schedule meetings with potential partners to discuss opportunities and explore potential synergies. Consult with legal and financial advisors to ensure the partnership is structured appropriately and protects your interests.

Ongoing developments in the business landscape are constantly creating new partnership opportunities, so stay informed and adaptable.