Largest Pension Funds In The Us

Imagine a bustling city filled with hardworking individuals, each contributing diligently to their careers, dreaming of a secure and comfortable retirement. Behind the scenes, quietly and diligently managing their futures, are colossal financial institutions, the guardians of their retirement dreams: the largest pension funds in the United States. These behemoths of finance wield immense power, shaping not just individual lives, but also the economic landscape of the nation.

These pension funds represent the bedrock of retirement security for millions of Americans. This article delves into the world of the largest US pension funds, exploring their size, scope, and significance in safeguarding the financial futures of public sector employees and private sector workers alike.

The Titans of Retirement Security

Let's begin by identifying some of the key players. These are the pension funds that manage hundreds of billions, even trillions, of dollars in assets. They are the pillars upon which many Americans base their retirement hopes.

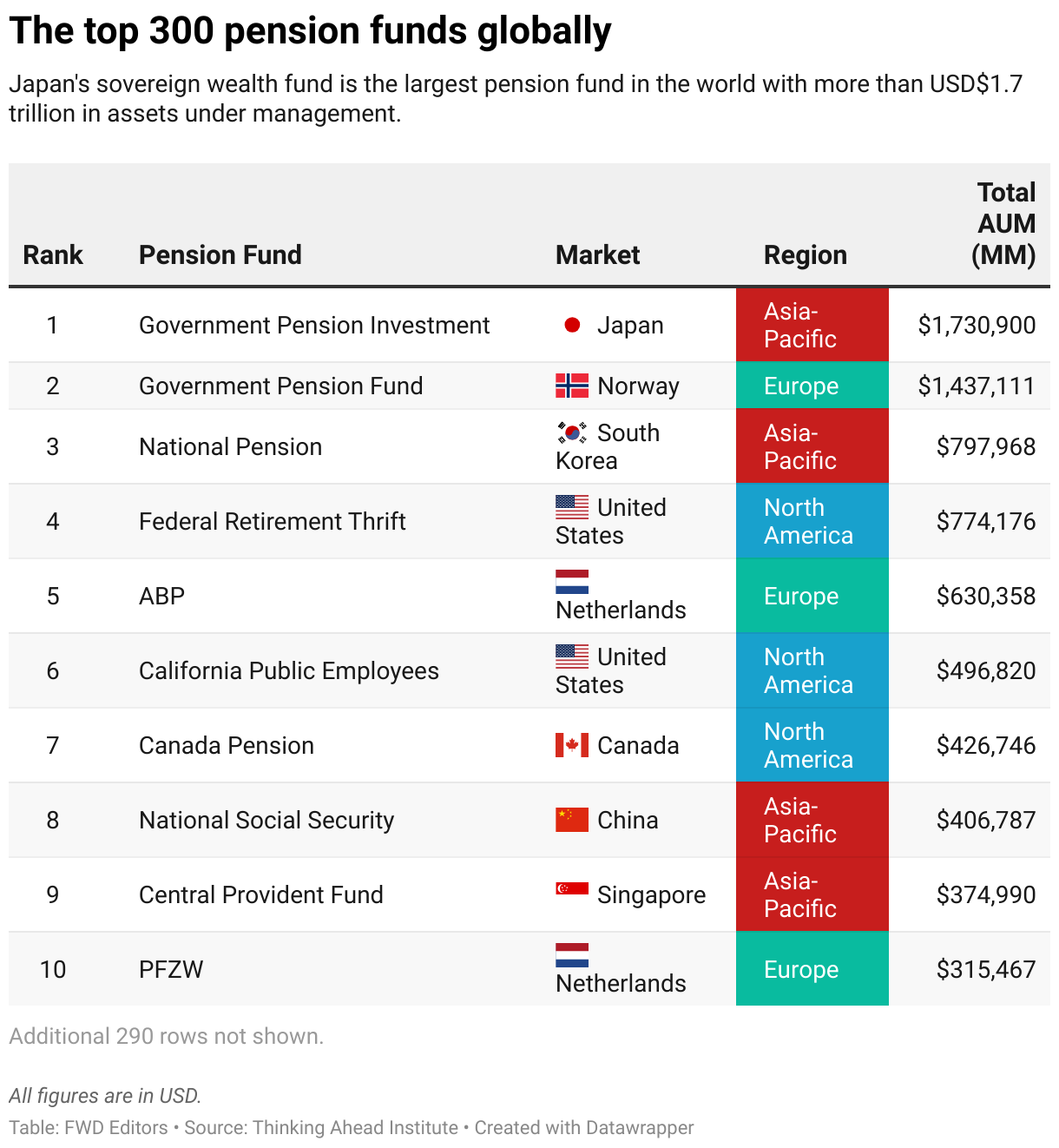

At the forefront is the Federal Retirement Thrift Investment Board, managing the Thrift Savings Plan (TSP). The TSP serves federal employees and uniformed services members, providing a defined contribution plan akin to a 401(k). Its enormous scale reflects the vast workforce it serves.

Another major player is the California Public Employees' Retirement System (CalPERS). CalPERS is the largest public pension fund in the US, providing retirement benefits to California state, school, and public agency employees.

Closely following is the California State Teachers' Retirement System (CalSTRS). CalSTRS focuses specifically on providing retirement, disability, and survivor benefits to California's public school educators.

These are just a few examples. Other significant funds include the New York State Common Retirement Fund and the Texas Teacher Retirement System (TRS).

A Historical Perspective

The rise of pension funds in the US is intertwined with the evolution of labor laws and societal attitudes towards retirement. Before the mid-20th century, retirement security was largely a personal responsibility.

The introduction of Social Security in 1935 marked a turning point. It created a baseline of retirement income for many Americans. However, it was not designed to be a complete replacement for earned income.

This led to the growth of employer-sponsored pension plans. These plans offered a supplemental source of retirement income, further bolstering financial security for workers. Over time, these plans grew in size and sophistication, eventually becoming the massive pension funds we see today.

The Mechanics of Pension Funds

Pension funds operate on the principle of pooling contributions from employers and/or employees, investing those funds, and then distributing benefits to retirees. The goal is to grow the assets sufficiently to meet future obligations.

There are two primary types of pension plans: defined benefit and defined contribution. Defined benefit plans promise a specific benefit amount at retirement, typically based on salary and years of service.

Defined contribution plans, like the TSP, specify the amount of contributions made to an individual's account. The ultimate benefit depends on the investment performance of the account.

Pension funds invest in a wide range of assets, including stocks, bonds, real estate, and private equity. The investment strategy aims to balance risk and return, ensuring that the fund can meet its long-term obligations.

The Significance and Impact

The impact of these large pension funds is far-reaching. They are not only responsible for the retirement security of millions of Americans, but also play a significant role in the financial markets.

Their investments influence stock prices, bond yields, and the overall economy. As major shareholders in numerous companies, they also have a voice in corporate governance.

Furthermore, the existence of robust pension systems can contribute to a more stable and secure society. Knowing that they have a reliable source of income in retirement allows individuals to plan for the future with greater confidence.

Challenges and Opportunities

Despite their importance, pension funds face numerous challenges. These include increasing longevity, volatile investment markets, and underfunding.

People are living longer than ever before. This puts increased pressure on pension funds to provide benefits for a longer period of time. Market downturns can erode investment returns, making it harder to meet future obligations.

Many pension funds are underfunded, meaning they do not have enough assets to cover their projected liabilities. This is a serious issue that requires careful management and, in some cases, difficult decisions.

However, there are also opportunities for pension funds to adapt and thrive. Investing in new asset classes, improving risk management practices, and working with policymakers to address funding shortfalls are all potential solutions.

Technological advancements also present opportunities. Fintech solutions can help streamline operations, improve investment decision-making, and enhance communication with members.

The Future of Retirement Security

The future of retirement security in the US is closely linked to the health and stability of these large pension funds. Ensuring their long-term sustainability is crucial for the well-being of millions of Americans.

This requires a collaborative effort from policymakers, fund managers, employers, and employees. Open communication, transparent governance, and a commitment to responsible investing are essential.

As the economic landscape continues to evolve, pension funds must adapt and innovate to meet the challenges of the future. By doing so, they can continue to serve as pillars of retirement security for generations to come.

The story of the largest pension funds in the US is a testament to the power of collective action and the importance of planning for the future. These institutions, though often unseen, play a vital role in the lives of countless Americans, shaping their retirement dreams and contributing to the overall economic well-being of the nation. Their continued success is paramount to ensuring a secure and prosperous future for all.