Which Of These Statements Regarding The Extended Term Insurance

The intricacies of life insurance policies often leave beneficiaries and policyholders grappling with complex options. Extended Term Insurance (ETI), a non-forfeiture benefit, is one such area causing widespread confusion. Misunderstandings about its benefits, limitations, and application are rampant, leading to potential financial pitfalls for those unfamiliar with its nuances.

This article aims to clarify the common misconceptions surrounding Extended Term Insurance. It will provide a fact-driven examination of its mechanics. We will focus on identifying the accurate statements regarding its functionality and application, thereby empowering policyholders to make informed decisions about their life insurance coverage.

Understanding Extended Term Insurance

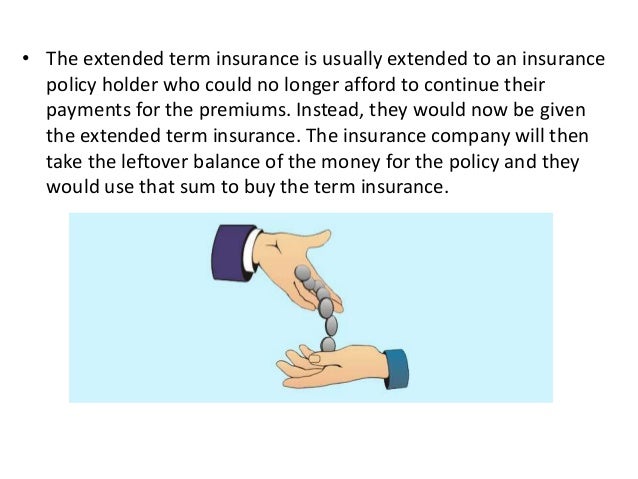

Extended Term Insurance is a provision in most whole life insurance policies. It activates when a policyholder stops paying premiums. Instead of surrendering the policy for its cash value, the policy's cash value is used as a single premium payment to purchase term life insurance for a specific duration.

The duration of this term coverage is determined by the amount of cash value available. This also affects the original death benefit amount stated in the whole life policy. It is not a new policy, but rather a continuation of coverage using the accumulated cash value.

Common Misconceptions and Accurate Statements

One widespread misconception is that Extended Term Insurance maintains the same premium payment schedule as the original whole life policy. This is false. ETI eliminates the need for ongoing premium payments as it is purchased with the cash value.

A correct statement is that the death benefit under Extended Term Insurance remains the same as the original policy's death benefit. The cash value is sufficient enough to purchase a term policy for the same face amount for a certain period.

Another common error is to assume ETI provides coverage indefinitely. The coverage period is finite and determined by the cash value and the insured's age. Once the term expires, the coverage ceases entirely.

A true statement about ETI is that it does not continue to accumulate cash value. The policy's existing cash value is used to purchase the term coverage. Future cash value growth is not possible under ETI.

Often, beneficiaries mistakenly believe that the Extended Term Insurance option is the default when premiums are unpaid. While it is a standard non-forfeiture option, policyholders often have to actively elect it, rather than have it automatically applied.

Furthermore, understanding the conditions for reinstatement is crucial. A correct statement is that the original whole life policy can usually be reinstated within a specific timeframe. This depends on satisfying certain requirements, such as repaying back premiums and proving insurability.

The Role of Cash Value

The cash value of a whole life policy is pivotal in determining the length of the Extended Term Insurance coverage. A higher cash value equates to a longer term of coverage at the same death benefit. This is because more cash value can purchase a term policy for a more extended period.

However, policy loans can impact the cash value. Any outstanding loans against the policy will reduce the cash value. This subsequently reduces the duration of the term coverage that can be purchased under the ETI option.

Comparing ETI to Other Non-Forfeiture Options

Reduced Paid-Up Insurance is another common non-forfeiture option. Under this option, the policyholder receives a fully paid-up life insurance policy. This results in a reduced death benefit, but no further premiums are required and the policy lasts for the remainder of the insured's life.

Cash Surrender Value involves the policyholder receiving the policy's cash value in a lump sum payment. The life insurance coverage then terminates. Comparing these options can help a policyholder decide the best path.

Implications for Policyholders

Understanding the implications of Extended Term Insurance is essential for responsible financial planning. It is important to understand that ETI provides coverage for a limited time, and after that the coverage expires.

Policyholders should carefully consider their financial needs and long-term goals when choosing ETI. It's important to assess whether the term coverage aligns with their desired coverage period. The policyholder must also consider the possibility of reinstating the original policy, if this is the desired outcome.

Seeking Professional Guidance

Navigating the complexities of life insurance policies can be challenging. It's essential to consult with a qualified financial advisor or insurance professional. They can provide personalized advice. They can also help the policyholder decide which non-forfeiture option best suits their circumstances.

Independent experts can also offer unbiased assessments of policy terms and conditions. They can also highlight potential risks and benefits associated with different coverage choices. It's best to make an informed choice, rather than take the first option provided.

Looking Ahead

The insurance industry is evolving. Transparency and clarity are increasingly important in policy design and communication. Insurance companies should improve their disclosures. They should also aim to help policyholders better comprehend options like Extended Term Insurance.

By promoting financial literacy and accessible information, the life insurance industry can empower individuals to make informed decisions. This will ensure that policies meet the needs of policyholders and their beneficiaries. Also, it can avoid confusion and potential financial hardship.

Ultimately, a better understanding of Extended Term Insurance will ensure individuals use life insurance policies effectively. This will lead to better financial planning and secure the financial future of their loved ones.

:max_bytes(150000):strip_icc()/dotdash-031005-Medicaid-vs-Long-Term-Care-Insurance-Final-96bd18c9639a483696cb6e2049e37650.jpg)