Who Makes Economic Decisions In A Market Economy

In a market economy, the intricate web of economic decisions isn't dictated by a single entity, but rather emerges from the decentralized actions of countless individuals and businesses. Understanding this dynamic is crucial for anyone seeking to navigate the complexities of modern economic systems.

At the heart of the matter lies the fundamental question: who truly steers the economic ship? The answer, as this article will explore, is multifaceted and involves a constant interplay of supply, demand, and individual choice.

The Core Players: Individuals, Businesses, and the Market

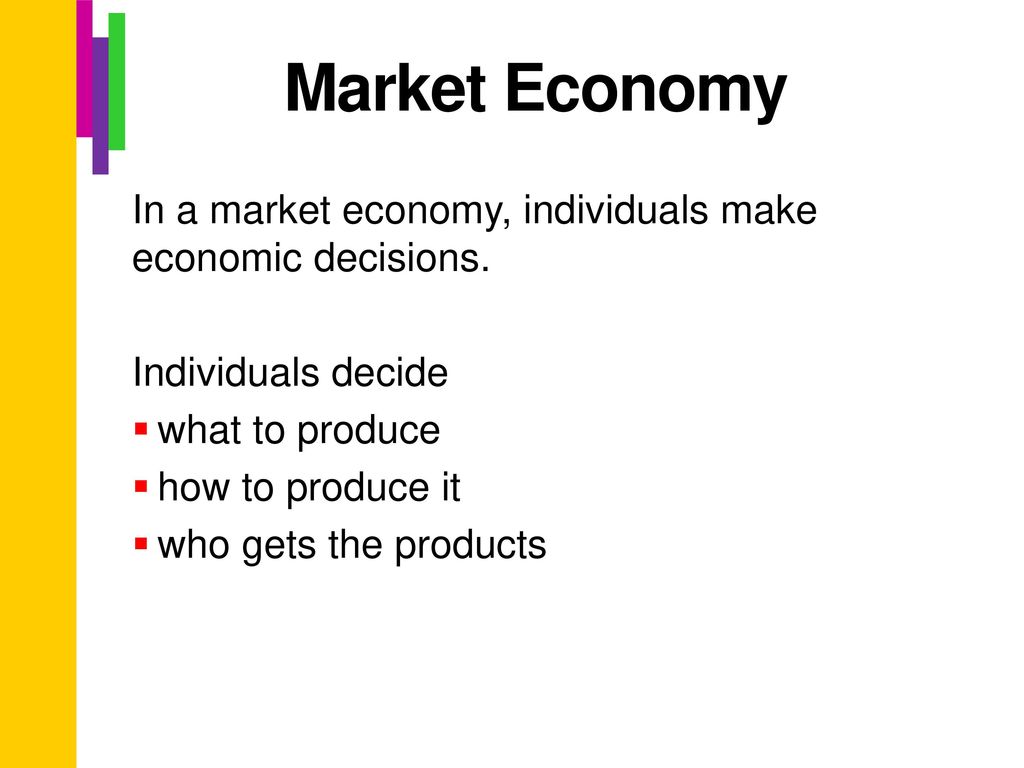

The market economy operates on the principle of decentralized decision-making, where economic choices are distributed among various actors, primarily individuals and businesses. These actors interact within markets, driving the allocation of resources and the determination of prices.

Individuals, as consumers and laborers, play a pivotal role. Their purchasing decisions signal demand, guiding businesses on what to produce and at what quantity.

Likewise, their choices regarding employment influence the supply of labor available to companies.

Consumers: The Demand Drivers

Consumers, through their choices, effectively cast "votes" in the marketplace. These votes signal their preferences for goods and services.

A surge in demand for a product, for example, will typically lead to increased production and potentially higher prices. Conversely, a decline in demand can result in reduced output and price cuts.

These individual choices, aggregated across millions of consumers, create the overall demand landscape that shapes business strategies.

Businesses: Supply and Innovation

Businesses, driven by the pursuit of profit, respond to consumer demand by producing and supplying goods and services. They decide what to produce, how to produce it, and at what price to offer it.

Competition among businesses encourages innovation and efficiency, leading to a wider variety of products and potentially lower prices for consumers. Innovation, therefore, becomes a crucial driving force within a market economy.

Businesses also make critical decisions about hiring, investment, and expansion, further impacting the overall economic landscape.

The Price Mechanism: A Guiding Force

The price mechanism serves as a critical communication tool within a market economy. Prices reflect the relative scarcity and desirability of goods and services.

High prices typically signal strong demand and limited supply, incentivizing businesses to increase production. Low prices, on the other hand, often indicate weak demand or excess supply, prompting businesses to reduce output or lower prices.

This constant feedback loop, driven by price signals, helps to allocate resources efficiently across the economy.

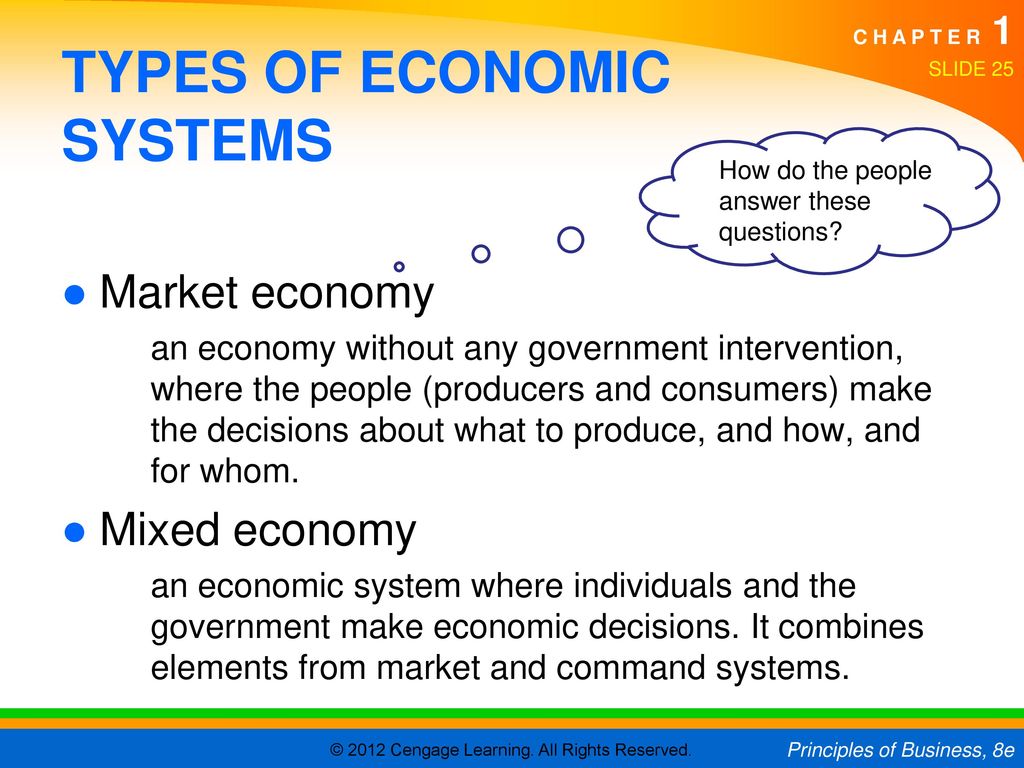

The Role of Government: Setting the Stage

While the market economy emphasizes decentralized decision-making, the government plays an important role in establishing the rules of the game. This includes enforcing contracts, protecting property rights, and ensuring fair competition.

Governments may also intervene in the market to address market failures, such as pollution or the provision of public goods. These interventions can take the form of regulations, taxes, or subsidies.

However, excessive government intervention can stifle innovation and distort market signals, potentially leading to inefficiencies.

The Impact on Society

The decentralized decision-making process of a market economy can lead to both positive and negative outcomes. On the one hand, it can foster innovation, efficiency, and a wide variety of choices for consumers.

On the other hand, it can also lead to inequality, market failures, and instability. Addressing these challenges requires careful consideration of the appropriate role for government intervention.

Ultimately, the success of a market economy depends on the ability of individuals, businesses, and the government to work together to create a stable and prosperous society.

A Human Perspective

"The beauty of the market is that it allows individuals to pursue their own self-interest, while simultaneously contributing to the overall well-being of society," says Dr. Anya Sharma, an economist at the Institute for Economic Research. "But it's crucial to remember that markets are not perfect, and they require careful oversight to ensure fairness and sustainability."

Consider Maria Rodriguez, a small business owner who started a bakery in her local community. Her decision to open the bakery was driven by her passion for baking and her belief that there was a demand for her products.

Through her business, she not only provides goods and services to her community but also creates jobs and contributes to the local economy. Her story exemplifies the power of individual initiative and the potential for entrepreneurship to thrive in a market economy.

Conclusion: A Constant Evolution

Economic decision-making in a market economy is a dynamic and ever-evolving process. It involves the constant interaction of individuals, businesses, and the government, each playing a vital role in shaping the overall economic landscape.

Understanding the principles of market economics is essential for navigating the complexities of the modern world and for making informed decisions about our own economic lives.

By embracing the principles of free markets, while also addressing the challenges and inequalities that can arise, we can create a more prosperous and equitable future for all.

+make+the+decisions.jpg)