Does Cosigning For Someone Affect Your Credit

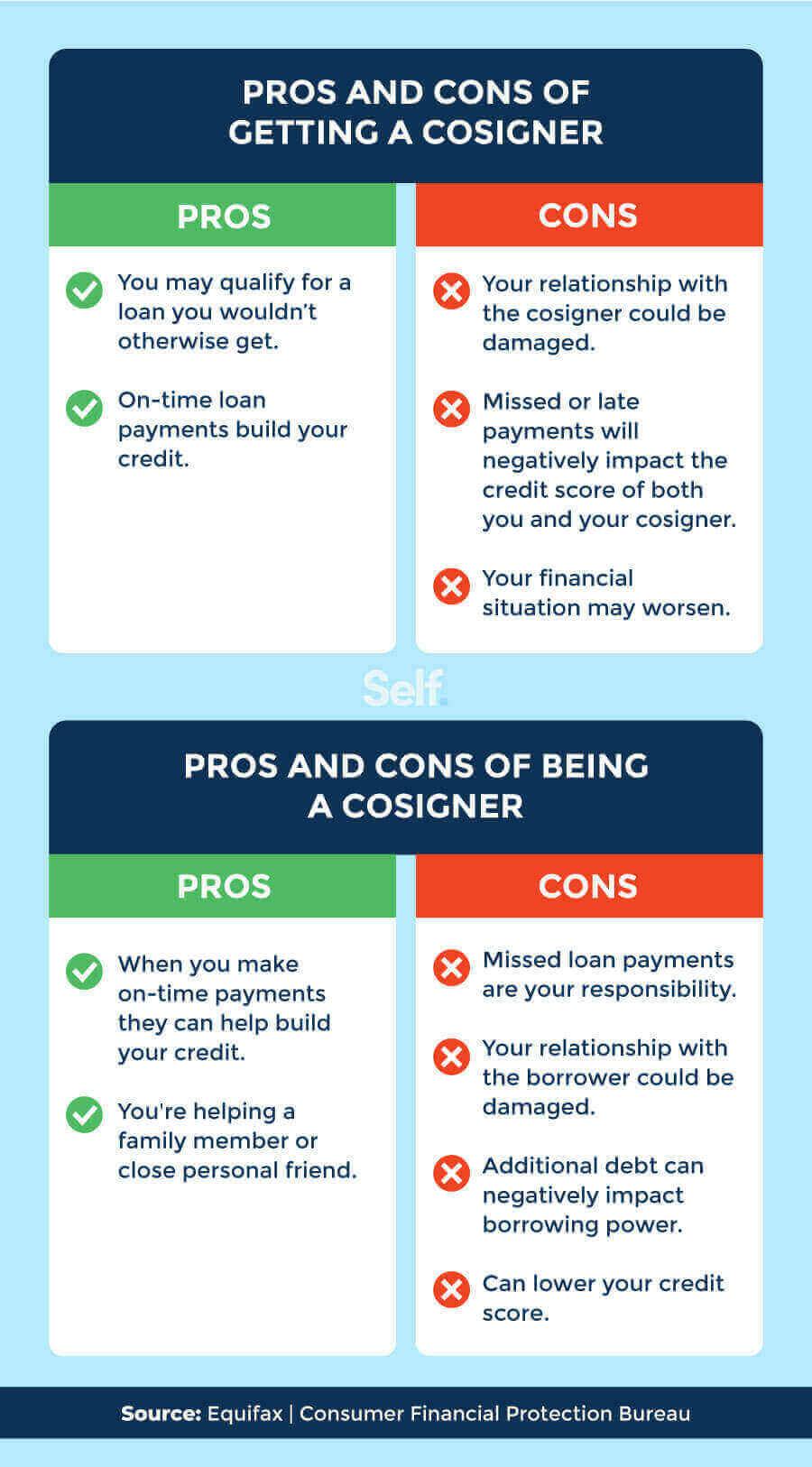

Cosigning a loan can significantly impact your credit score, potentially jeopardizing your financial stability. This common practice, often undertaken for loved ones, carries substantial risks that require careful consideration.

The Stark Reality of Cosigning

Cosigning essentially makes you equally responsible for the debt. If the primary borrower fails to pay, the lender will come after you.

This action affects your credit report and overall financial health, regardless of whether you make the payments yourself. Understand the potential consequences before agreeing to cosign.

How Cosigning Impacts Your Credit

Cosigning adds the debt to your credit report. Experian, Equifax, and TransUnion all track this debt as your own.

Even if payments are current, the increased debt-to-income ratio can lower your credit score. Lenders see you as a higher risk because of the increased financial burden.

Credit Utilization and Score

Your credit utilization ratio—the amount of credit you're using compared to your total available credit—is a crucial factor in credit scoring. Adding a cosigned loan can substantially increase this ratio.

For example, if you have a credit card with a $5,000 limit and you carry a $1,000 balance, your credit utilization is 20%. A cosigned loan, even with timely payments, can push this ratio higher, potentially damaging your score.

Payment History and Default

Late payments or default by the primary borrower will directly impact your credit. Lenders report payment activity to credit bureaus. Any missed or late payments reflect negatively on your credit history.

A default on the cosigned loan can lead to collection actions, lawsuits, and even wage garnishment. These severe actions can remain on your credit report for up to seven years.

Credit Inquiries

When you cosign, the lender will run a credit check. This inquiry can slightly lower your credit score, although the impact is usually minor.

However, multiple credit inquiries within a short period can have a more significant effect, especially if you're already working to improve your credit.

Who is Most Affected?

Individuals with already high debt-to-income ratios are particularly vulnerable. Cosigning can push them over the edge, making it harder to qualify for their own loans or credit cards.

According to a Federal Trade Commission (FTC) study, cosigners often underestimate the risk involved. Many are surprised to discover that they are held liable for the debt.

Where and When Does This Occur?

Cosigning most frequently occurs for auto loans, student loans, and personal loans. These types of loans often require a cosigner when the primary borrower has limited credit history or low income.

The impact on your credit occurs throughout the life of the loan. Your credit score is continuously updated based on payment history and outstanding balances.

What Can You Do?

Thoroughly evaluate the borrower's ability to repay the loan before cosigning. Assess their income, expenses, and existing debt obligations.

Consider the potential consequences for your own financial well-being. Can you comfortably afford to repay the loan if the primary borrower defaults?

Alternatives to Cosigning

Explore alternatives such as gifting money for a down payment or offering financial advice. These options can support the borrower without directly jeopardizing your credit.

Encourage the borrower to explore secured loans or credit-building products. These alternatives may help them establish credit without relying on a cosigner.

Next Steps and Ongoing Developments

If you've already cosigned a loan, regularly monitor the borrower's payment history. Stay informed about any potential issues that could impact your credit.

You can check your credit reports from Experian, Equifax, and TransUnion for free annually at AnnualCreditReport.com. Dispute any inaccuracies promptly.

"Cosigning is a generous act, but it's essential to understand the potential consequences," advises Ted Rossman, a senior industry analyst at Bankrate. "Carefully weigh the risks before agreeing to cosign a loan."

Consider seeking legal or financial advice before cosigning any loan agreement. Understanding your rights and obligations can help you make an informed decision.

The Consumer Financial Protection Bureau (CFPB) offers resources and educational materials on cosigning and credit management. Use these resources to protect your financial future.

+fails+to+pay+it..jpg)