If You Cosign A Loan Does It Affect Your Credit

The act of cosigning a loan can seem like a simple act of goodwill, a way to help a friend or family member achieve a financial goal. However, the seemingly straightforward decision carries significant implications for your own creditworthiness.

This article delves into the intricacies of cosigning, exploring how it affects your credit score, the risks involved, and what you need to know before putting your name on the dotted line.

Understanding the Basics of Cosigning

Cosigning a loan essentially means you are guaranteeing the debt of another person. As a cosigner, you are legally obligated to repay the loan if the primary borrower defaults.

This obligation is a crucial point to understand, as it directly impacts your credit health.

How Cosigning Impacts Your Credit Score

The act of cosigning itself doesn't immediately affect your credit score. However, the loan appears on your credit report, just as if you were the primary borrower.

This means several factors related to the loan can influence your credit score, according to Experian, one of the three major credit bureaus.

Payment History: If the primary borrower makes timely payments, it can positively reflect on your credit report, albeit less significantly than if you were the primary borrower. However, missed or late payments are reported to the credit bureaus and can negatively impact your credit score.

Credit Utilization Ratio: Even though you are not actively using the credit, the cosigned loan contributes to your overall credit utilization ratio. This is the amount of credit you're using compared to your total available credit.

A high credit utilization ratio can signal to lenders that you're overextended, potentially lowering your credit score.

Credit Mix: Having a variety of credit accounts (e.g., installment loans, credit cards) can positively influence your credit score. A cosigned loan can contribute to your credit mix, but its impact is generally less significant than accounts you manage directly.

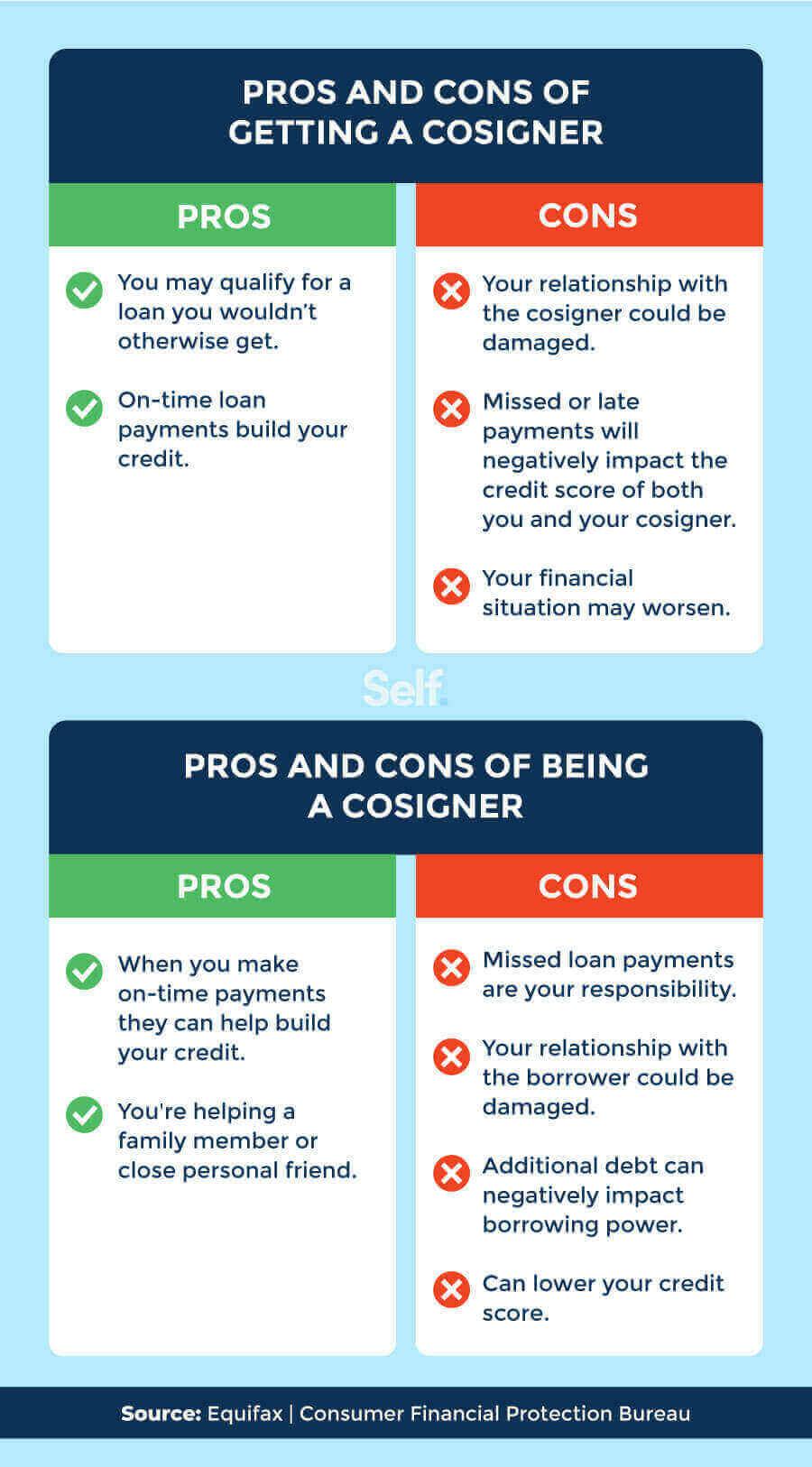

The Risks of Cosigning

The most significant risk of cosigning is the potential for the primary borrower to default. If this happens, you are responsible for repaying the entire loan, including any outstanding interest and fees.

This can strain your finances and potentially lead to debt collection actions. Defaulting on a cosigned loan will have a substantial negative impact on your credit score, potentially making it difficult to obtain credit in the future.

Another risk is the impact on your ability to obtain your own credit. Lenders consider the debt you are obligated to repay, including cosigned loans, when evaluating your creditworthiness.

This can limit the amount of credit you can access for your own needs, such as a mortgage or car loan.

Consider this hypothetical: Sarah cosigned a $20,000 auto loan for her brother. While he made payments initially, he eventually lost his job and defaulted. Sarah was then responsible for the remaining balance, which strained her budget and negatively affected her credit score when she couldn't keep up with the payments on the cosigned loan and her own debts.

Mitigating the Risks

Before cosigning a loan, carefully consider the potential risks and take steps to protect yourself. First, thoroughly evaluate the primary borrower's financial situation.

Assess their ability to repay the loan and their history of managing debt. Second, understand the terms of the loan agreement, including the interest rate, repayment schedule, and any penalties for late payments or default.

You can also explore options like a co-borrower arrangement where both parties benefit and take responsibility for the debt. According to the Federal Trade Commission, cosigners have rights, including receiving a copy of the loan agreement and being notified if the borrower misses payments.

Negotiate a limit to your liability: If possible, negotiate with the lender to limit your liability to a specific amount or a specific time period.

Consider alternative solutions: Explore whether there are other ways to help the borrower, such as providing financial counseling or helping them improve their credit score before applying for a loan.

The Human Element

Often, the decision to cosign stems from a desire to help a loved one. However, it's crucial to separate emotional considerations from financial realities.

Open and honest communication with the borrower is essential. Discuss their financial situation, their plans for repayment, and what will happen if they encounter difficulties.

Remember, cosigning a loan is a significant financial commitment. It should not be taken lightly.

Cosigning a loan can have both direct and indirect impacts on your credit. While responsible payment by the primary borrower can have a slightly positive impact, defaults can be devastating to your creditworthiness.

Careful consideration, thorough evaluation, and open communication are vital before making the decision to cosign.

.jpg)

.jpg)

![If You Cosign A Loan Does It Affect Your Credit Short-Term Loans and Credit Ratings [What You Need to Know]](https://powerfinancetexas.com/wp-content/uploads/2019/12/PowerFinan_Avoid-a-Lower-Credit-Score-_inf-1-1.jpg)

:max_bytes(150000):strip_icc()/how-will-debt-settlement-affect-my-credit-score.asp_Final-5338c75878d3481cba132e2b34a97fd1.jpg)