One Characteristic Of Incremental Budgeting Is That It

Across municipalities and governmental agencies, a budgetary method quietly shapes resource allocation: incremental budgeting. While seemingly straightforward, this approach, characterized by adjustments to existing budgets rather than zero-based evaluation, carries significant implications for fiscal policy and the distribution of public funds.

At its core, incremental budgeting operates on the principle of making marginal changes to the previous year’s budget. This means that rather than constructing a budget from scratch, departments typically request a small percentage increase (or occasionally a decrease) based on their prior allocation. The practice is widespread, influencing resource distribution in sectors ranging from education and infrastructure to defense and social services.

The Core Trait: Reliance on the Status Quo

The defining characteristic of incremental budgeting is its inherent reliance on the existing budget baseline. This baseline serves as the starting point, with adjustments made based on perceived needs or anticipated changes in circumstances. Such a method assumes the previous budget was largely appropriate and effective.

This is not always the case. Critics argue that this reliance can perpetuate inefficiencies and misallocations from previous budget cycles, as programs may continue to receive funding even if their effectiveness is questionable.

The process often involves negotiation between departments and the central budget authority, with departments advocating for increased funding and the authority seeking to maintain fiscal responsibility. The outcome is typically a compromise that reflects both the perceived needs of the departments and the overall fiscal constraints.

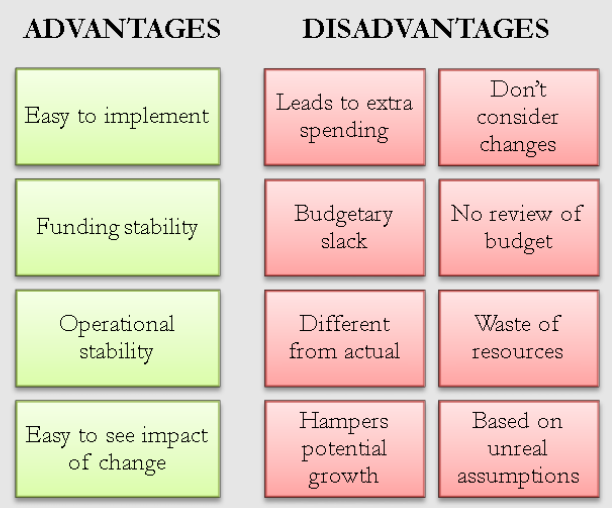

Simplicity and Stability

Incremental budgeting offers several practical advantages. It is relatively simple to understand and implement, requiring less extensive analysis and justification than more comprehensive budgeting methods. This simplicity reduces administrative overhead and streamlines the budget process.

Furthermore, the incremental nature of the process provides a degree of stability and predictability. Departments can reasonably anticipate their funding levels for the upcoming year, allowing for more effective planning and resource management.

However, this stability can also be a drawback. It can discourage innovation and hinder the reallocation of resources to more pressing priorities.

Potential Drawbacks and Criticisms

The reliance on the previous year's budget can lead to a phenomenon known as "budget creep," where budgets gradually increase over time without a corresponding increase in performance or value. This can result in a misallocation of resources, with funds directed towards less effective programs simply because they have historically received funding.

Another criticism is that incremental budgeting tends to favor established departments and programs. New initiatives or programs may struggle to gain traction, as they must compete with existing programs that already have a secured place in the budget.

Moreover, incremental budgeting can be resistant to significant changes in policy or priorities. If a new administration takes office with a dramatically different agenda, it may be difficult to implement those changes within the framework of incremental budgeting.

The Human Impact: A Case Study

In the city of Midvale, the Parks and Recreation department provides a tangible example. For years, the department's budget had increased incrementally, primarily to cover rising maintenance costs for existing parks. However, a growing need for new recreational facilities in underserved neighborhoods went unmet.

Residents of these neighborhoods felt marginalized, arguing that the incremental approach favored the upkeep of older, more affluent parks at the expense of their communities' needs. The Midvale case illustrates how incremental budgeting, while seemingly neutral, can have disparate impacts on different segments of the population.

Eventually, community activists successfully lobbied for a shift towards a needs-based budgeting approach, resulting in a greater allocation of resources to the underserved areas. This demonstrates that while incremental budgeting provides stability, it may necessitate revisiting existing systems to meet evolving societal needs.

Looking Ahead

Incremental budgeting remains a prevalent method in many organizations, but its effectiveness hinges on careful monitoring and evaluation. Regular reviews of program performance are crucial to ensure that resources are being used efficiently and effectively. Transparency in the budgeting process is also essential, allowing stakeholders to understand how decisions are made and hold decision-makers accountable.

While simplicity and stability are advantages, it’s important to recognize the potential drawbacks. A balanced approach, possibly incorporating elements of zero-based budgeting or other more dynamic resource allocation methods, may be necessary to overcome the limitations of relying solely on incremental adjustments to the status quo. The goal should be a budget that reflects current priorities, promotes efficiency, and addresses the evolving needs of the community it serves.