Payday Loans That Don't Use Plaid

Consumer advocates are urgently warning borrowers about the dwindling options for payday loans that don't rely on Plaid, a third-party data aggregator. This shift raises significant privacy and security concerns, particularly for vulnerable individuals seeking short-term financial relief.

The increasing reliance on Plaid within the payday loan industry presents a double-edged sword: faster access to funds versus heightened risk of data breaches and unauthorized access to sensitive banking information. Borrowers need to be aware of alternatives and the potential consequences of sharing their financial data through third-party platforms.

The Plaid Problem: Data Access and Privacy Concerns

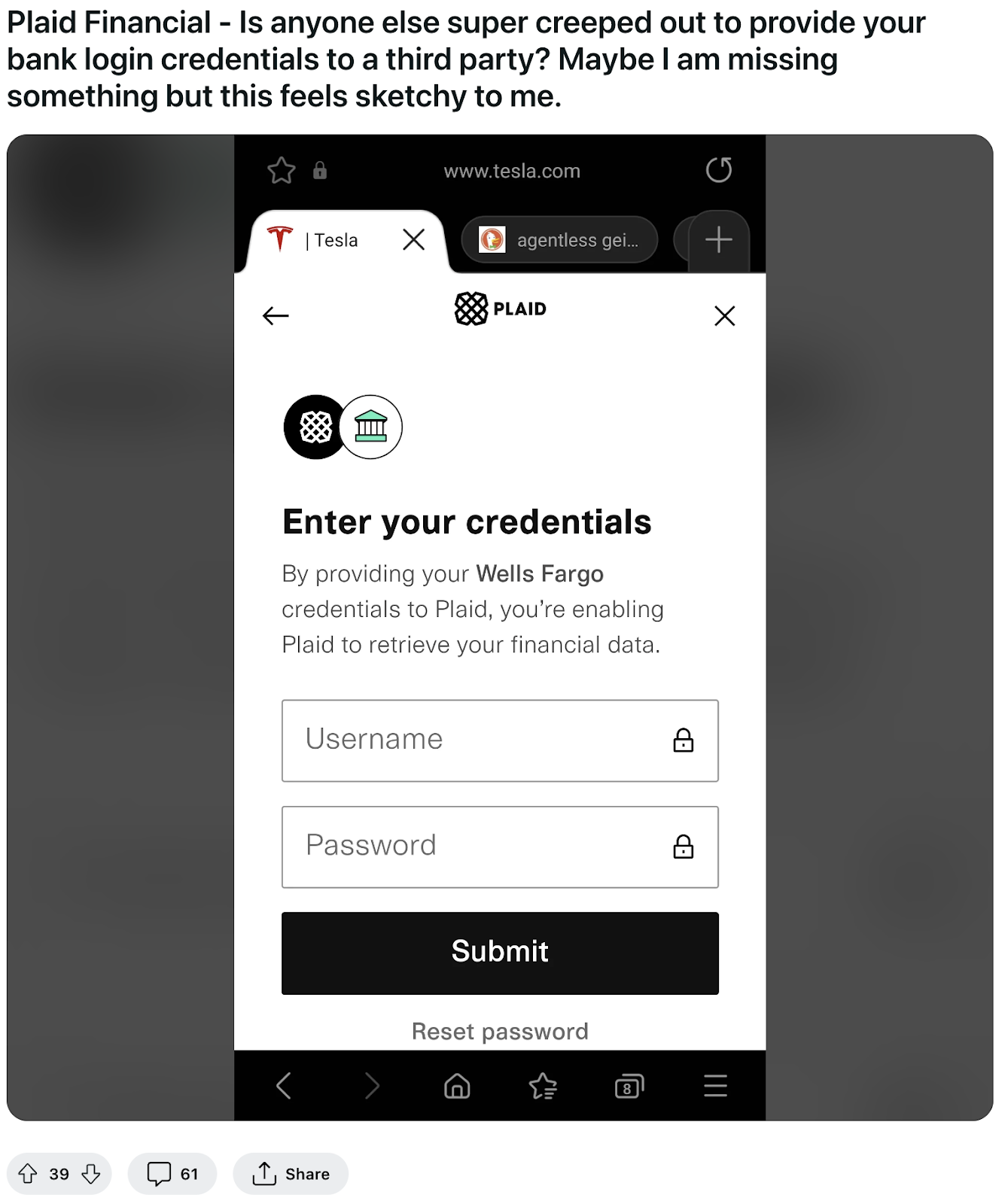

Plaid connects apps to users' bank accounts, enabling lenders to verify financial information quickly. However, this convenience comes at a cost: borrowers grant Plaid access to their transaction history, account balances, and other personal details.

Critics argue that this level of access is excessive and poses a significant privacy risk. Data breaches involving Plaid or lenders using the platform could expose sensitive financial information to malicious actors.

Furthermore, some borrowers may be uncomfortable sharing such detailed data with a third party, especially given the potentially predatory nature of some payday lenders.

Where to Find Payday Loans That Bypass Plaid

The landscape of payday lenders offering alternatives to Plaid is shrinking, but some options remain. Credit unions and smaller, local lenders may still offer payday loans without requiring third-party data access.

Direct lenders who verify information manually, though potentially slower, represent another route. These lenders typically request bank statements or other documentation directly from the borrower.

Online searches using specific keywords like "payday loans no Plaid" or "payday loans without third-party verification" can help identify these lenders. However, extreme caution is advised: thoroughly vet any lender before sharing personal information.

The Risk of Predatory Lending Practices

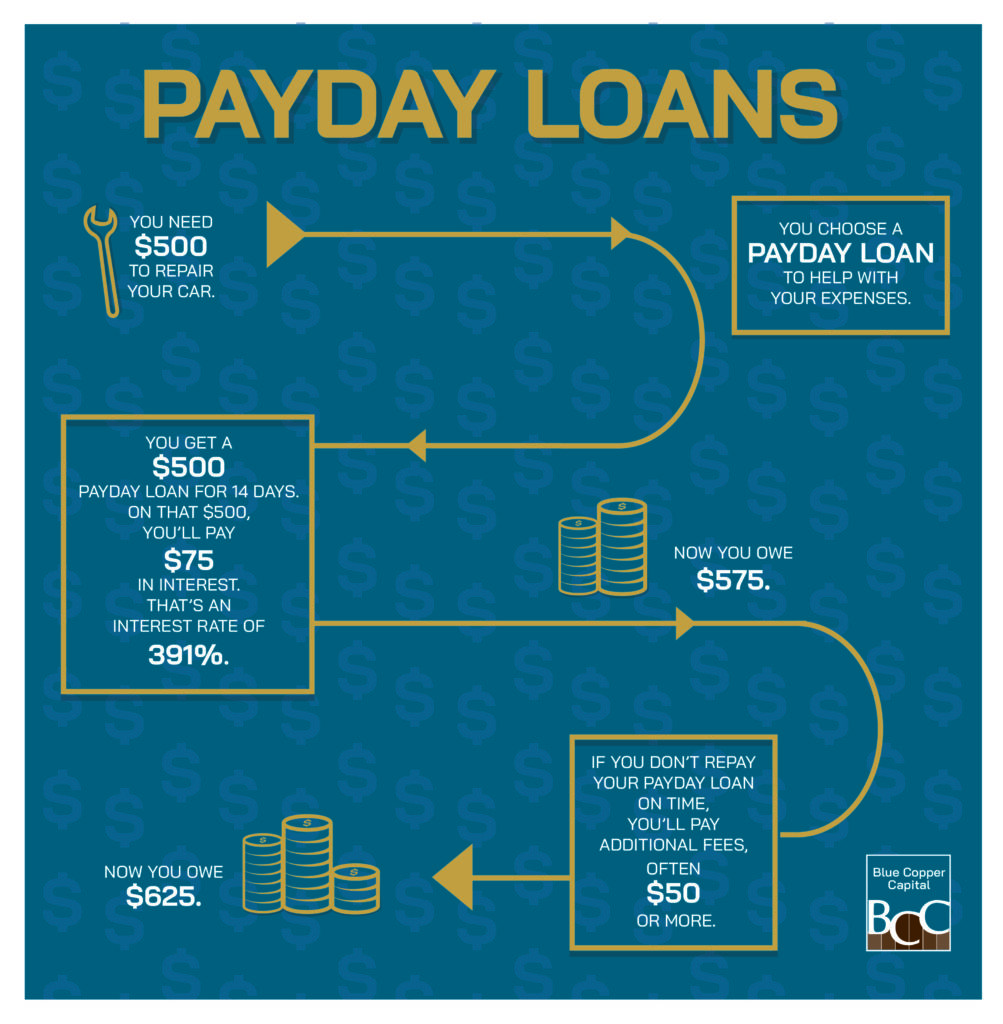

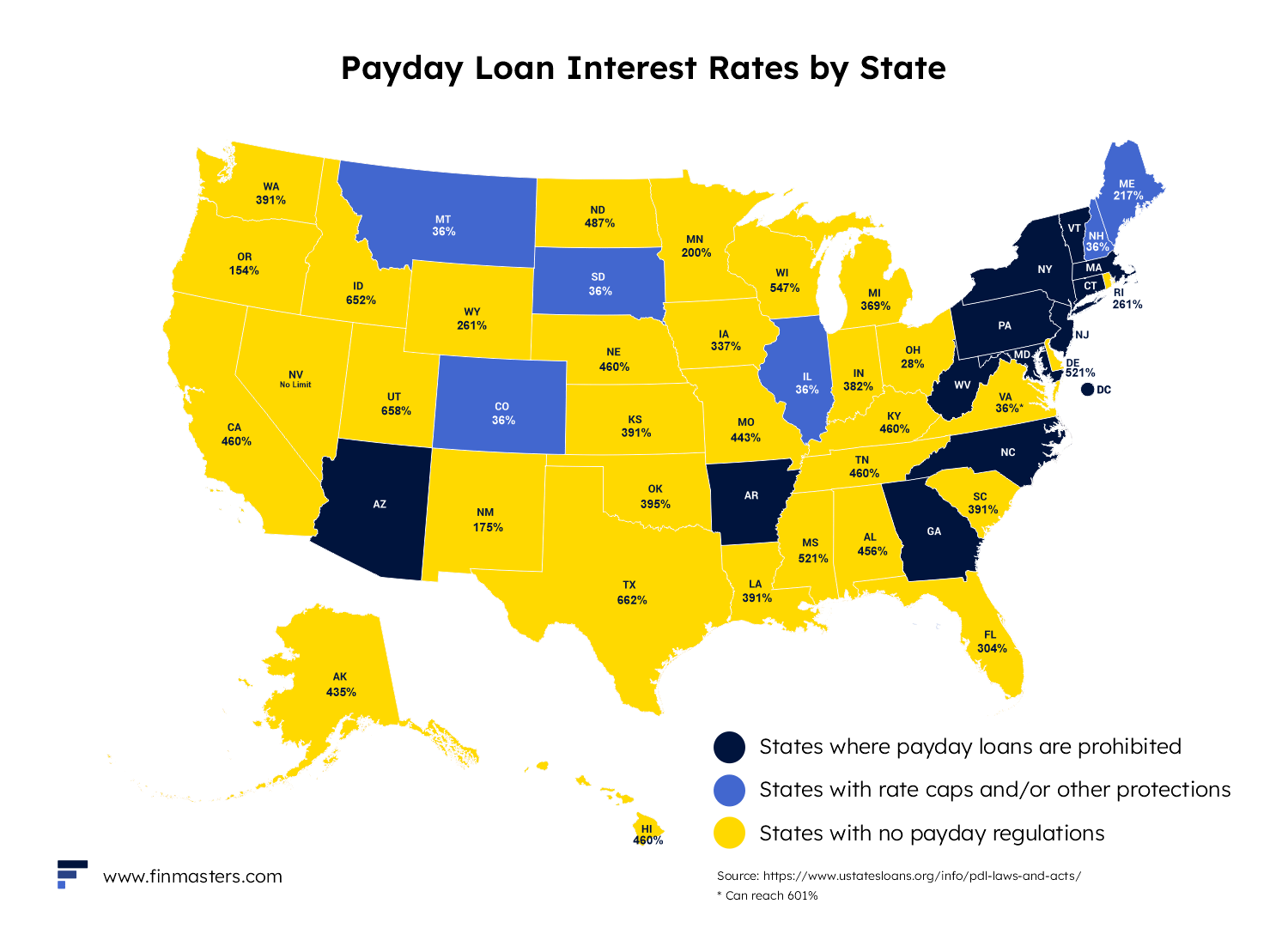

Regardless of whether a lender uses Plaid, it's crucial to be aware of predatory lending practices. Payday loans often come with exorbitant interest rates and fees, trapping borrowers in a cycle of debt.

Before taking out a payday loan, explore all other options, including borrowing from friends or family, seeking assistance from community organizations, or negotiating a payment plan with creditors.

According to the Consumer Financial Protection Bureau (CFPB), the average payday loan borrower ends up paying $520 in fees for a $375 loan. This highlights the extreme cost of these loans.

Manual Verification: A Slow but Safer Route

Lenders who manually verify information offer a more secure, albeit slower, alternative to Plaid. This process typically involves the borrower providing bank statements, pay stubs, and other documentation directly to the lender.

While this method requires more effort from both the borrower and the lender, it reduces the risk of data breaches and unauthorized access to financial information. It also allows borrowers to maintain greater control over their data.

However, be prepared for longer processing times and potentially stricter approval requirements. Direct lenders may require a higher credit score or proof of stable income.

Warning Signs of a Shady Lender

Beware of lenders who guarantee approval regardless of credit history or income. These lenders may be operating illegally or engaging in predatory lending practices.

Avoid lenders who demand upfront fees or pressure you to borrow more than you need. Always read the fine print carefully and understand the terms and conditions of the loan before signing anything.

Report any suspected scams or predatory lending practices to the Federal Trade Commission (FTC) or your state's attorney general's office.

The Future of Payday Lending and Data Security

The trend toward greater reliance on third-party data aggregators like Plaid is likely to continue. However, consumer advocacy groups are pushing for stronger data privacy regulations and increased transparency.

The CFPB is also actively monitoring the payday lending industry and taking enforcement actions against lenders who violate consumer protection laws. Borrowers should stay informed about their rights and available resources.

In the meantime, borrowers seeking payday loans should carefully weigh the risks and benefits of sharing their financial data with third-party platforms. Explore all available alternatives and prioritize data security and privacy.

:max_bytes(150000):strip_icc()/How-can-i-borrow-money-my-life-insurance-policy_final-fa1474645da94b368bb3f5452392b0c0.png)