Personal Loan For Bad Credit With Cosigner

Urgent action is needed: Millions with damaged credit are finding a lifeline in personal loans secured with a cosigner, offering access to funds otherwise unavailable. But be warned, these loans carry significant risks for both borrower and cosigner, demanding careful consideration.

These loans are emerging as a crucial, yet potentially dangerous, option for those excluded from traditional lending due to poor credit history. Weigh the pros and cons before making a decision.

The Rising Demand for Cosigned Loans

What: Personal loans for bad credit with a cosigner are seeing increased demand nationwide.

Who: Individuals with low credit scores (typically below 630), often rejected by conventional lenders, are seeking these loans. According to Experian, nearly 34% of Americans have a credit score that falls within the “fair” or “poor” range.

Where: This trend is observed across the US, with online lenders and credit unions increasingly offering these products.

When: The surge in demand is linked to rising living costs and increased debt burdens following recent economic fluctuations.

How Cosigned Loans Work

A cosigner, typically a family member or close friend with a good credit score, agrees to be equally responsible for the loan. This significantly increases the borrower's chances of approval and often results in a lower interest rate.

If the borrower defaults, the lender will pursue the cosigner for the outstanding debt. This can severely damage the cosigner's credit score and their relationship with the borrower.

The Risks Involved

Risk to the Borrower: Failure to repay the loan will not only further damage the borrower’s credit but also negatively impact the cosigner.

Risk to the Cosigner: The cosigner's credit score is directly impacted by the borrower’s repayment behavior. Late or missed payments are reported to credit bureaus, lowering the cosigner’s creditworthiness.

According to a 2023 study by the Consumer Financial Protection Bureau (CFPB), cosigners often underestimate the risks involved and are surprised when they are held liable for the debt.

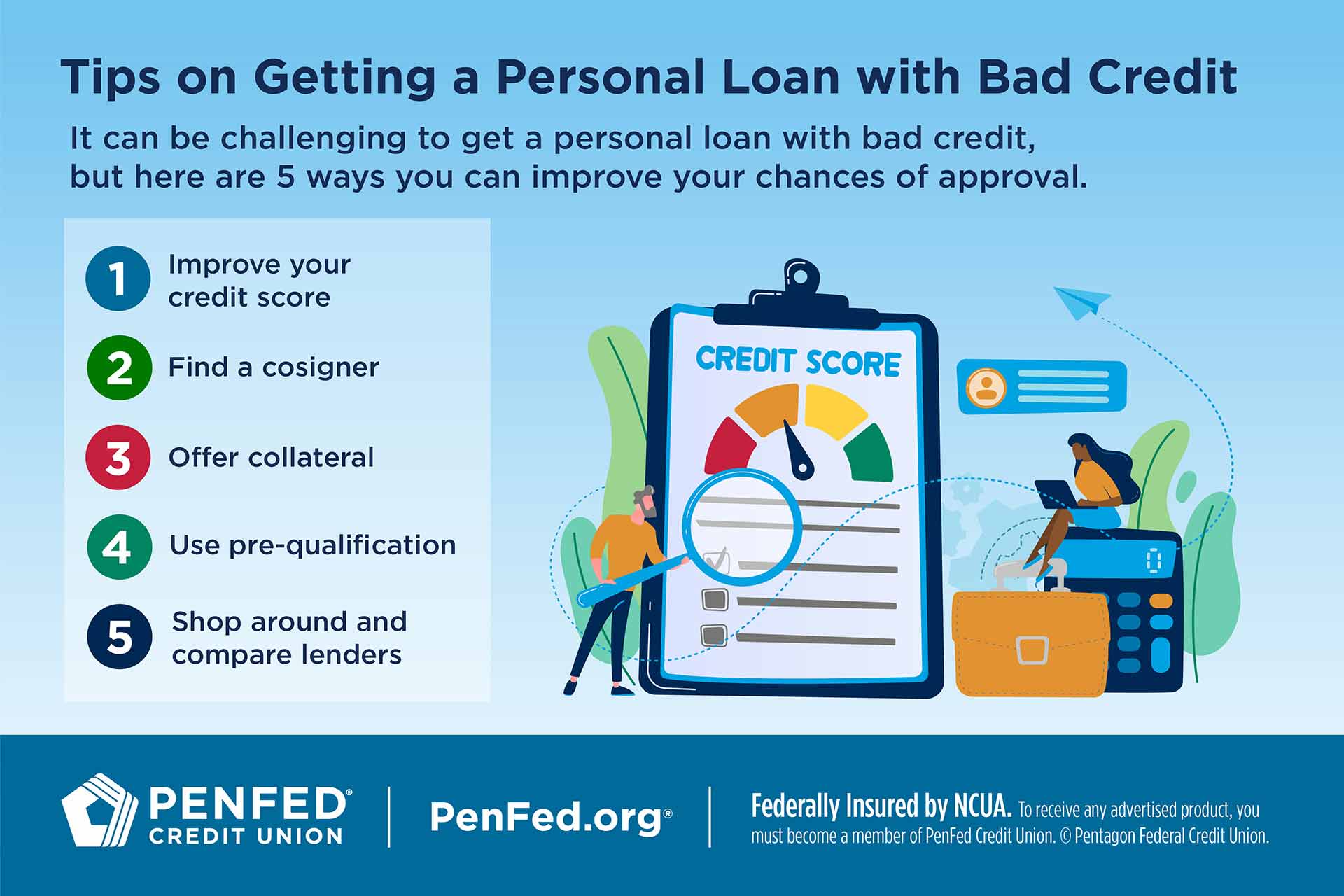

Finding a Reputable Lender

Do Your Research: Compare interest rates, fees, and loan terms from multiple lenders before committing.

Check Lender Reviews: Look for complaints or negative feedback on the lender’s customer service and lending practices.

Read the Fine Print: Carefully review the loan agreement, including the terms and conditions, before signing. Pay close attention to late payment penalties and default provisions.

Alternatives to Cosigned Loans

Secured Loans: Consider secured loans, which require collateral, such as a vehicle or savings account. While collateral is at risk, it eliminates the need for a cosigner.

Credit Repair: Work on improving your credit score through responsible financial habits, such as paying bills on time and reducing debt. Credit repair services can also assist in challenging inaccuracies on your credit report.

Credit Builder Loans: These loans are specifically designed to help individuals with bad credit improve their creditworthiness. The lender holds the loan amount in an account, and the borrower makes monthly payments. Upon completion of the loan term, the borrower receives the funds and has established a positive payment history.

Real-World Impact

Maria Rodriguez, a single mother with a credit score of 580, needed $5,000 for urgent car repairs. After being denied by several banks, she turned to a cosigned personal loan. Her sister, Elena Rodriguez, agreed to cosign.

Unfortunately, Maria lost her job three months later and struggled to make payments. Elena was then contacted by the lender and forced to pay the remaining balance to protect her own credit.

This situation, though fictionalized, highlights the potential financial and emotional strain cosigned loans can create within families and friendships.

Expert Advice

"Cosigning a loan is a serious financial commitment," warns Sarah Chen, a certified financial planner. "Before agreeing to cosign, understand the potential risks and ensure you can afford to repay the loan if the borrower defaults. Consider it a gift, not a loan."

The Bottom Line

Cosigned personal loans offer a pathway to funding for individuals with bad credit, but they come with significant risks. Both borrowers and cosigners must fully understand their obligations before entering into such agreements.

Evaluate all available options and seek professional financial advice to determine the best course of action. The CFPB is actively monitoring the market for potential predatory lending practices related to cosigned loans, offering resources and guidelines for consumers.