What Does A Strong Economy Depend On The Most

In an era defined by economic volatility and global interconnectedness, the question of what truly underpins a strong economy is more critical than ever. From Main Street businesses grappling with inflation to policymakers wrestling with growth strategies, the foundations of economic prosperity are constantly scrutinized and debated. Understanding these fundamental drivers is not merely an academic exercise; it is the key to navigating the complexities of the modern economic landscape and building a more resilient and prosperous future.

This article delves into the core elements considered vital for a robust economy. We will explore the roles of factors such as a skilled workforce, technological innovation, stable institutions, and effective demand management, examining how these components interact to foster sustainable economic growth. We will also consider differing viewpoints on the relative importance of these factors, drawing on insights from leading economists and empirical data to present a balanced perspective.

The Pillars of Economic Strength

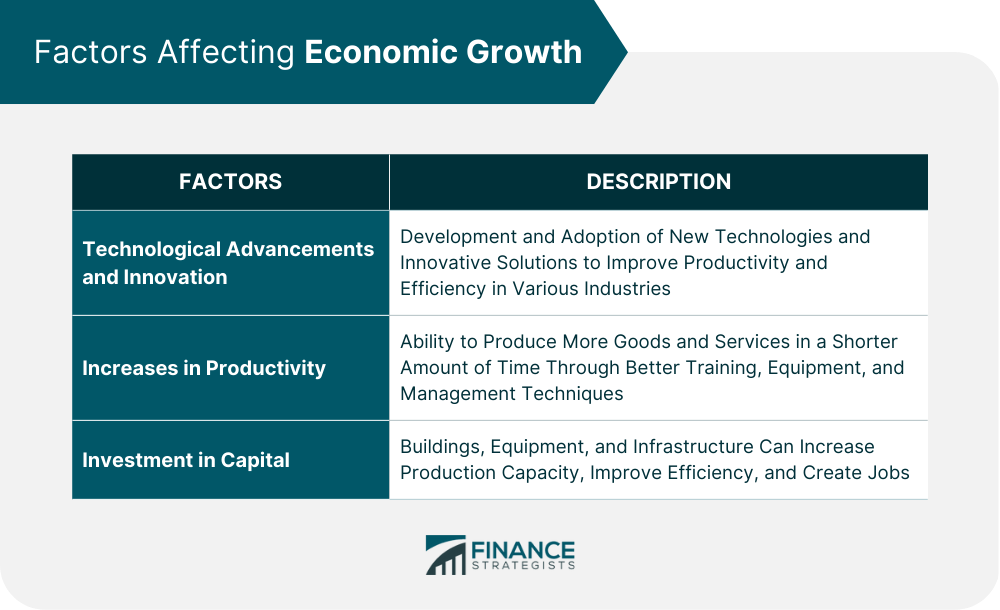

Human Capital: A Skilled and Adaptable Workforce

A well-educated and skilled workforce is arguably the most critical asset for any economy. Investment in education, training, and healthcare directly translates into higher productivity and greater innovation.

As Gary Becker, Nobel laureate in economics, emphasized, human capital is a key driver of economic growth. Countries with strong education systems and robust vocational training programs consistently outperform those that lag in these areas.

For instance, nations like South Korea and Singapore, which prioritized education and skills development, have experienced remarkable economic transformations in recent decades, becoming high-income countries with advanced industries.

Technological Innovation and Productivity Growth

Technological progress is a powerful engine of economic growth, driving productivity gains and creating new industries. Innovation allows businesses to produce more goods and services with fewer resources, leading to higher living standards.

According to the OECD, investments in research and development (R&D) are crucial for fostering innovation and driving long-term economic growth. Governments can play a significant role in supporting R&D through funding for basic research, tax incentives for private sector innovation, and intellectual property protection.

The rise of Silicon Valley and other technology hubs demonstrates the transformative potential of innovation. These regions attract talented individuals, foster collaboration, and generate new ideas that fuel economic growth.

Stable Institutions and Sound Governance

Stable political and legal institutions are essential for creating a predictable and secure environment for businesses and investors. Strong rule of law, protection of property rights, and transparent governance are crucial for fostering trust and encouraging investment.

As highlighted by Daron Acemoglu and James Robinson in their book "Why Nations Fail," inclusive political and economic institutions are fundamental for long-term economic success. Countries with corrupt or authoritarian governments often struggle to attract investment and achieve sustained economic growth.

The World Bank's Doing Business indicators provide a useful measure of the ease of doing business in different countries, highlighting the importance of regulatory efficiency and legal frameworks for economic performance.

Effective Demand Management and Monetary Policy

Managing aggregate demand and maintaining price stability are crucial for preventing recessions and fostering sustainable economic growth. Central banks play a key role in this regard through monetary policy, adjusting interest rates and managing the money supply to influence inflation and economic activity.

John Maynard Keynes emphasized the importance of government intervention to stabilize the economy during periods of recession. Fiscal policy, including government spending and taxation, can be used to stimulate demand and support economic recovery.

However, excessive government debt and inflation can also undermine economic stability. Striking the right balance between demand management and fiscal responsibility is a critical challenge for policymakers.

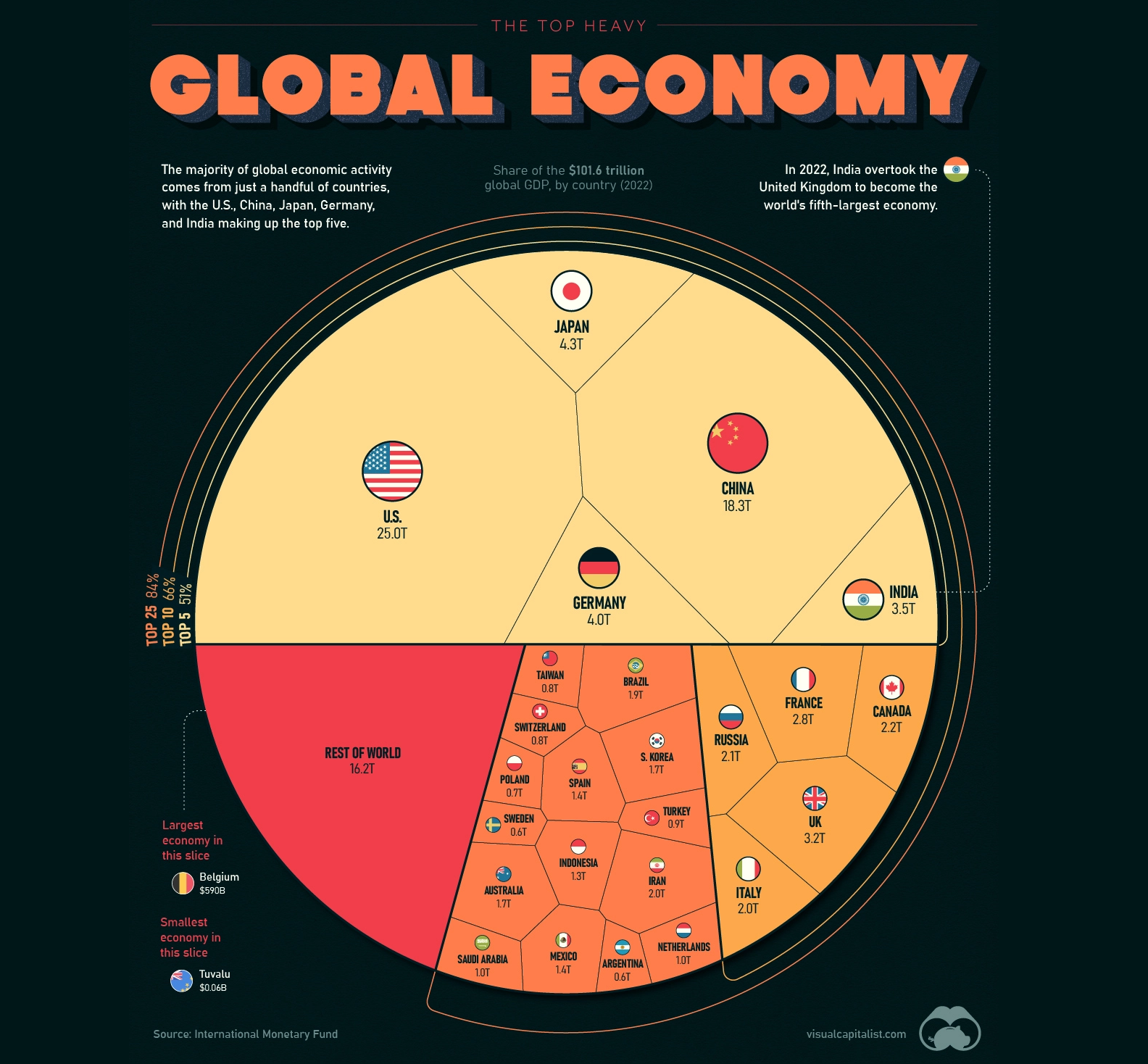

Open Trade and Global Integration

Open trade policies can foster economic growth by allowing countries to specialize in the production of goods and services in which they have a comparative advantage. Access to larger markets can increase competition, drive innovation, and lower prices for consumers.

According to the World Trade Organization (WTO), trade liberalization has contributed significantly to global economic growth over the past several decades. However, trade can also have distributional effects, and policymakers need to address the concerns of workers and industries that may be negatively impacted.

Recent trends toward protectionism and trade wars pose a threat to global economic growth. Maintaining a rules-based international trading system is crucial for ensuring that all countries can benefit from trade.

Contrasting Perspectives and the Importance of Balance

While there is broad consensus on the importance of these factors, economists often disagree on the relative importance of each. Some argue that technological innovation is the primary driver of long-term economic growth, while others emphasize the role of institutions and human capital.

Furthermore, different economic schools of thought may prioritize different policy interventions. For example, supply-side economists often advocate for tax cuts and deregulation to stimulate investment and production, while demand-side economists emphasize the role of government spending and social safety nets in supporting aggregate demand.

A balanced approach that recognizes the interconnectedness of these factors is essential for building a strong and sustainable economy.

Looking Ahead: Adapting to New Challenges

The global economy faces a number of significant challenges in the years ahead, including climate change, demographic shifts, and technological disruptions. Adapting to these challenges will require ongoing investment in education, innovation, and infrastructure.

Furthermore, policymakers need to address growing inequality and ensure that the benefits of economic growth are shared more broadly. This may involve strengthening social safety nets, investing in affordable housing, and promoting access to education and healthcare.

Ultimately, building a strong economy requires a long-term perspective and a commitment to investing in the factors that drive sustainable growth and prosperity for all.

-9160.jpg)

:max_bytes(150000):strip_icc()/TermDefinitions_Marketeconomy_finalv1-1d03048c89124873ac0350e7e96b1c4e.png)