What Is An All In One Loan

In today's complex financial landscape, homeowners are constantly seeking innovative ways to manage their debt and build wealth. One such tool gaining traction is the all-in-one loan, a financial product that merges a mortgage with a checking account, offering potential flexibility and control over finances.

But what exactly is an all-in-one loan, and how does it differ from traditional mortgages and home equity lines of credit (HELOCs)? This article delves into the mechanics of this unique financial instrument, its potential benefits, drawbacks, and overall impact on homeowners.

Understanding the All-In-One Loan

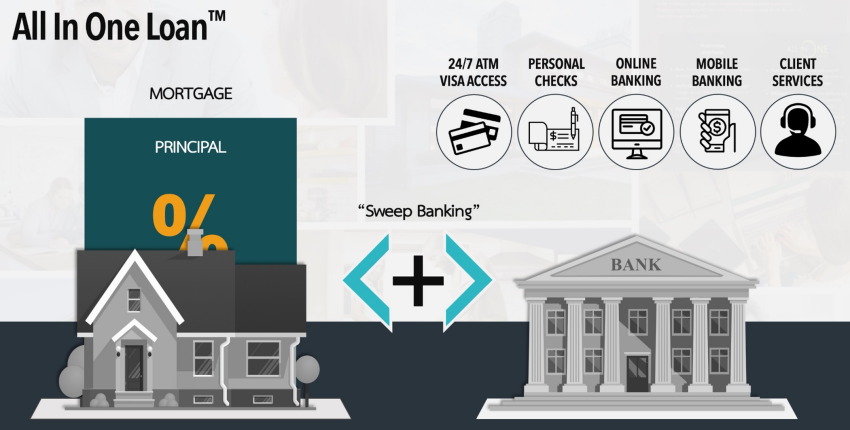

At its core, an all-in-one loan, also referred to as a mortgage offset account or a home equity line of credit mortgage, is a hybrid financial product. It combines the features of a mortgage with those of a checking account, creating a single, integrated account for managing both debt and cash flow.

The central idea is that the balance in the checking portion of the account directly offsets the principal balance of the mortgage. This means that for every dollar held in the account, the amount of interest accrued on the mortgage is reduced. This daily interest calculation is a key feature.

How It Works

Here's a simplified breakdown of how an all-in-one loan typically functions: A homeowner borrows a specific amount of money, just like a traditional mortgage. The borrowed funds are deposited into the all-in-one account. The borrower then uses this account for everyday transactions, such as paying bills, receiving income, and making purchases.

Unlike a standard mortgage, where payments are fixed over a set period, the interest charged on the all-in-one loan is calculated daily, based on the outstanding balance after considering any funds held in the account. This means if you keep a substantial amount of cash in the account, the amount of interest you pay on the mortgage decreases accordingly.

As stated by Bankrate, a leading financial information source, "All-in-one loans can be useful for people who want to pay down their mortgage quickly and are disciplined about managing their finances."

Potential Benefits and Drawbacks

The all-in-one loan presents both advantages and disadvantages. Prospective borrowers should carefully consider their financial situation and risk tolerance before committing to this type of product.

Benefits

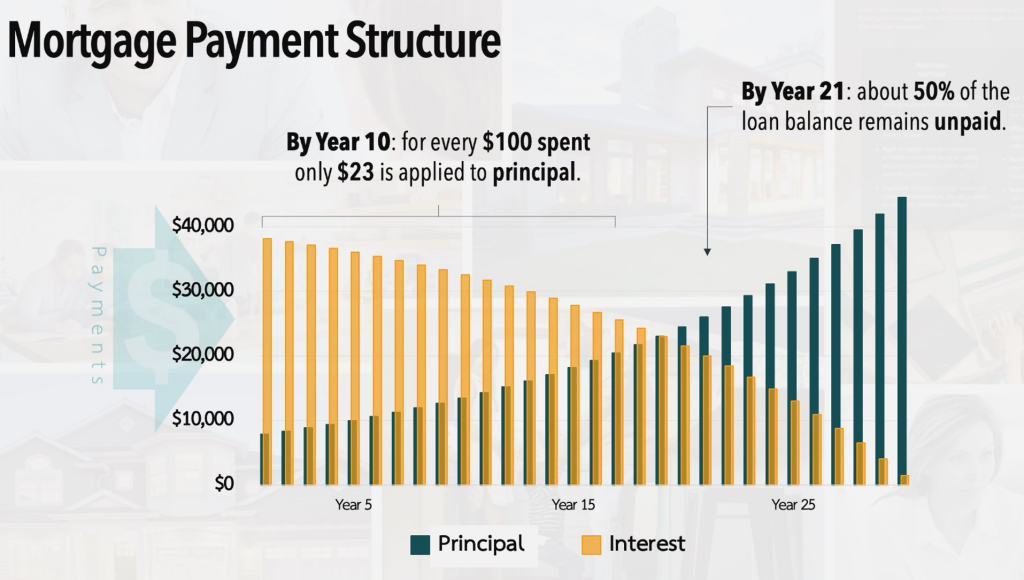

One of the most significant benefits is the potential for accelerated mortgage payoff. By consistently maintaining a higher balance in the account, borrowers can significantly reduce the principal amount of the loan, thereby shortening the overall repayment term and saving on interest payments.

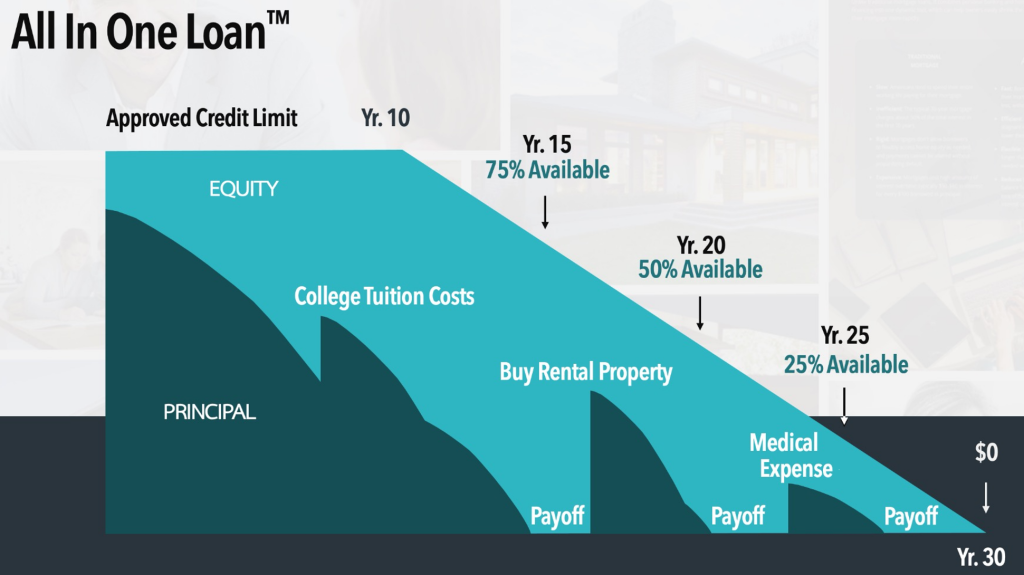

The flexibility of accessing funds is another key advantage. Borrowers can withdraw funds from the account as needed, essentially re-borrowing against their home equity up to the approved credit limit. This can be useful for unexpected expenses or investment opportunities. However, withdrawals increase the principal balance and the interest owed.

Increased control over finances is a major draw. The integrated nature of the account allows borrowers to easily track their cash flow and see the direct impact of their spending and saving habits on their mortgage balance.

Drawbacks

All-in-one loans often come with higher interest rates compared to traditional mortgages, especially if the lender perceives a higher risk associated with this type of product. Origination fees and other closing costs might also be higher.

Financial discipline is crucial. To maximize the benefits of an all-in-one loan, borrowers need to be diligent about managing their finances and consistently maintaining a substantial balance in the account. Poor financial habits can negate the advantages and even lead to increased debt.

The fluctuating interest rates of some all-in-one loans can be a concern. Because they are tied to market rates, your interest rate can change, leading to unpredictable monthly payments. This is especially true for all-in-one loans structured as a HELOC.

Impact and Considerations

The impact of all-in-one loans extends beyond individual borrowers. They can influence the broader housing market and the lending industry.

For lenders, these loans represent an opportunity to attract customers seeking greater financial control and flexibility. However, they also require careful underwriting and risk management to mitigate potential losses. Lenders like CMG Financial are among those offering all-in-one loan products.

For the housing market, wider adoption of all-in-one loans could potentially stimulate homeownership by making mortgages more manageable and attractive to certain segments of the population.

Before considering an all-in-one loan, it's essential to consult with a qualified financial advisor to assess your individual circumstances and determine if it's the right fit for your financial goals. Understanding the terms and conditions of the loan is paramount.

Always compare the costs, interest rates, and fees associated with different lenders and mortgage products. Don't rush into a decision; thoroughly research and understand all the potential risks and rewards.

Conclusion

All-in-one loans offer a novel approach to mortgage management, providing homeowners with the potential to accelerate debt payoff and gain greater control over their finances. However, they are not a one-size-fits-all solution.

Success with this type of loan hinges on financial discipline, a thorough understanding of its mechanics, and a careful evaluation of its potential benefits and drawbacks. Only then can borrowers truly harness the power of the all-in-one loan to achieve their financial objectives.

As the financial landscape continues to evolve, all-in-one loans may become an increasingly prominent tool for homeowners seeking to optimize their debt and build a more secure financial future. Staying informed and seeking expert advice will be key to navigating this evolving market.