What Is The Point At Which Supply And Demand Intersect

Imagine a bustling farmer's market on a sunny Saturday morning. Tables overflow with vibrant produce, from ruby-red tomatoes to sunshine-yellow corn. The air buzzes with the calls of vendors and the chatter of customers, all vying for the best deals and freshest goods. But amidst this flurry of activity lies a fundamental principle: the meeting point of supply and demand, the invisible hand guiding prices and availability.

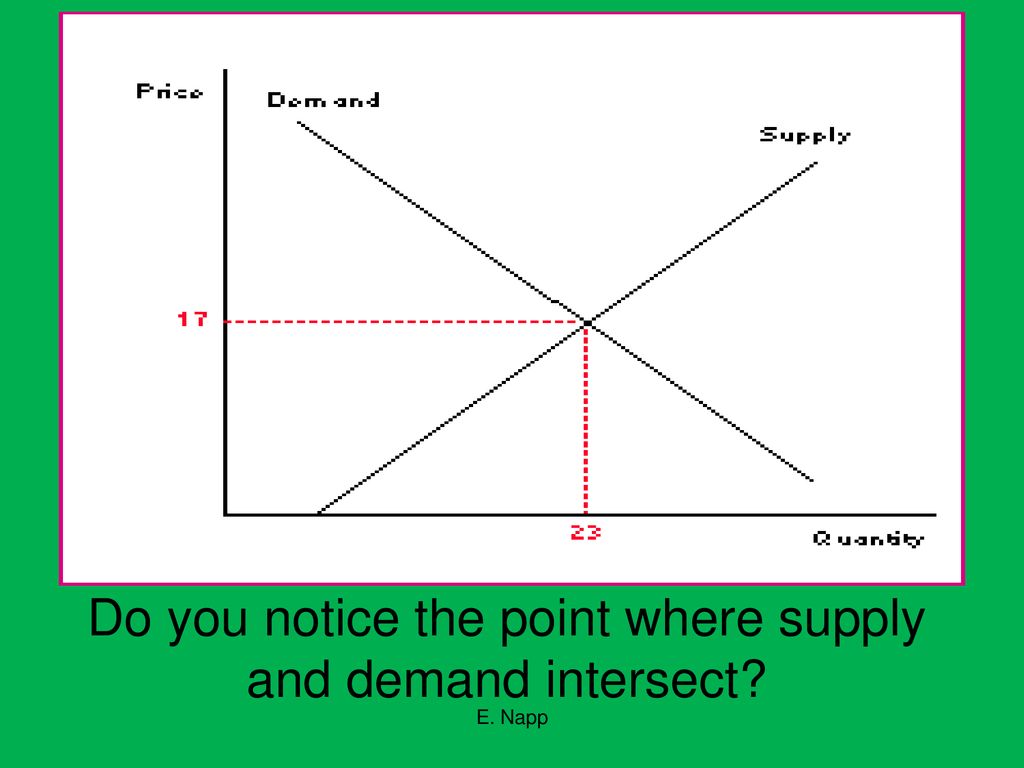

The intersection of supply and demand, known as the equilibrium point, is the price at which the quantity of a good or service that suppliers are willing to offer matches the quantity that consumers are willing to buy. This crucial concept is a cornerstone of economics, influencing everything from the cost of groceries to the value of stocks.

Understanding Supply and Demand

To fully grasp the equilibrium point, we must first understand the forces of supply and demand separately.

Demand: The Consumer's Voice

Demand reflects the desire and ability of consumers to purchase a good or service at various prices. Generally, as the price of something decreases, the demand for it increases, and vice versa. This inverse relationship is known as the law of demand.

Think about your favorite coffee. If the price suddenly doubles, you might opt for tea or make coffee at home. This demonstrates the principle of demand in action.

Factors beyond price can also influence demand. Changes in consumer income, tastes, and preferences, as well as the availability and prices of related goods (substitutes and complements), can all shift the demand curve.

Supply: The Producer's Response

Supply represents the willingness and ability of producers to offer a good or service at various prices. Unlike demand, supply typically has a direct relationship with price. The law of supply states that as the price of something increases, the quantity supplied tends to increase as well.

Consider a baker making bread. If the price of bread rises, they might be incentivized to bake more loaves to increase their profits.

Factors that can shift the supply curve include changes in production costs (raw materials, labor), technology, government regulations, and the number of suppliers in the market.

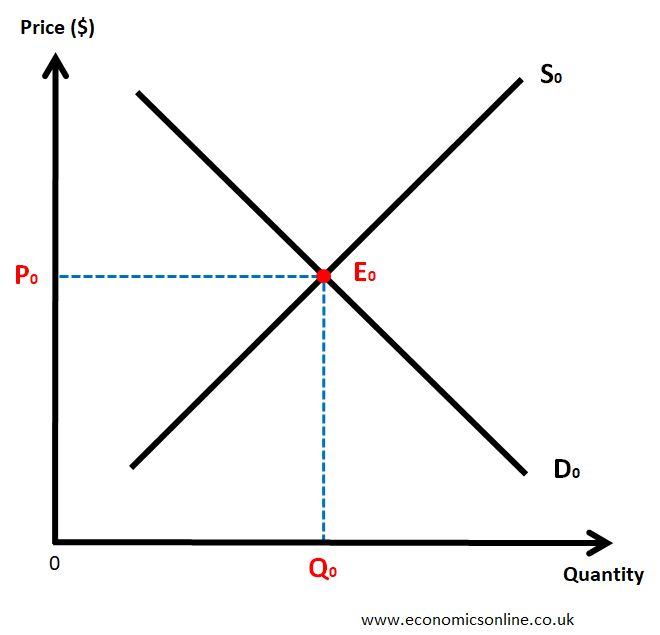

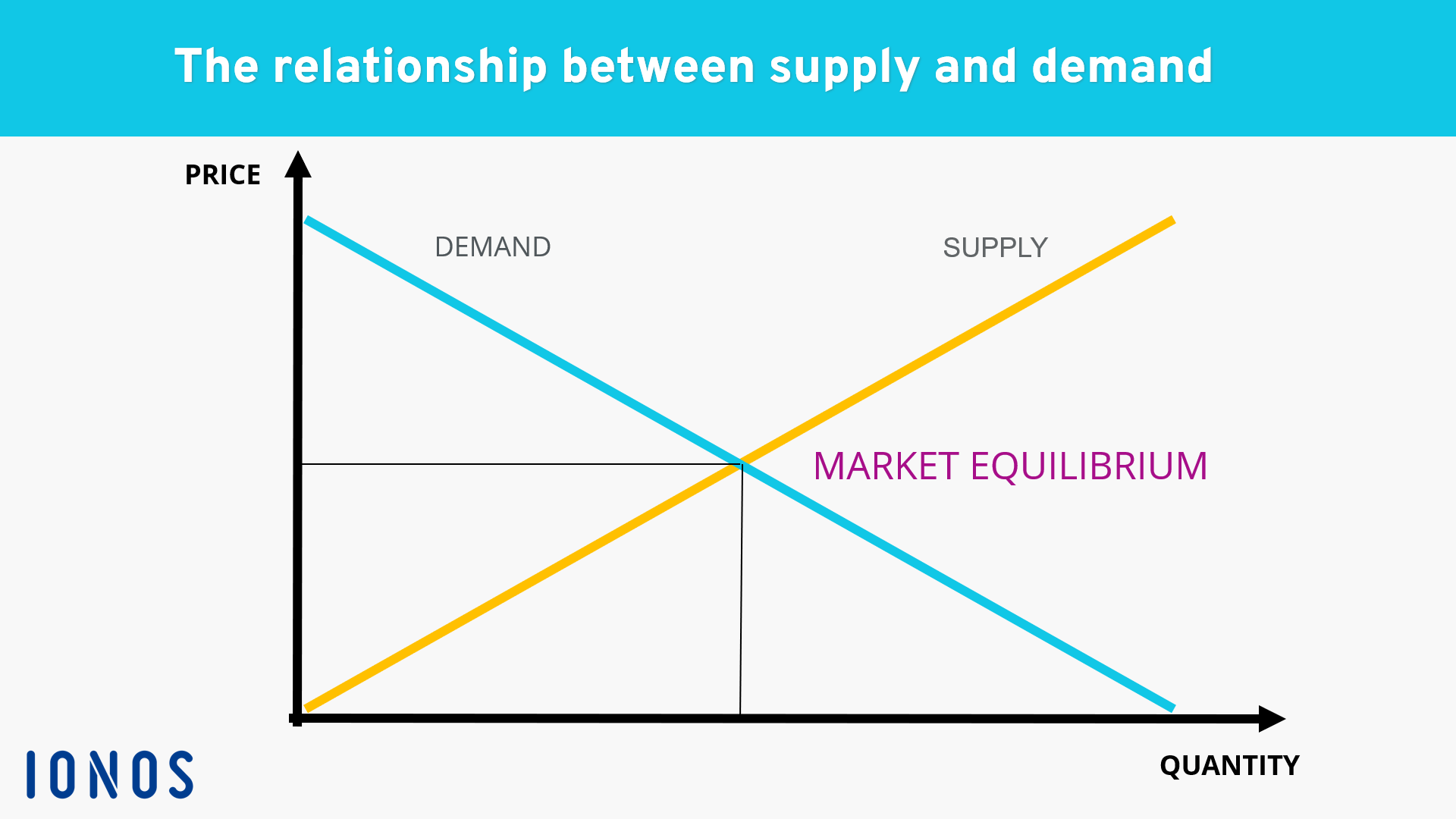

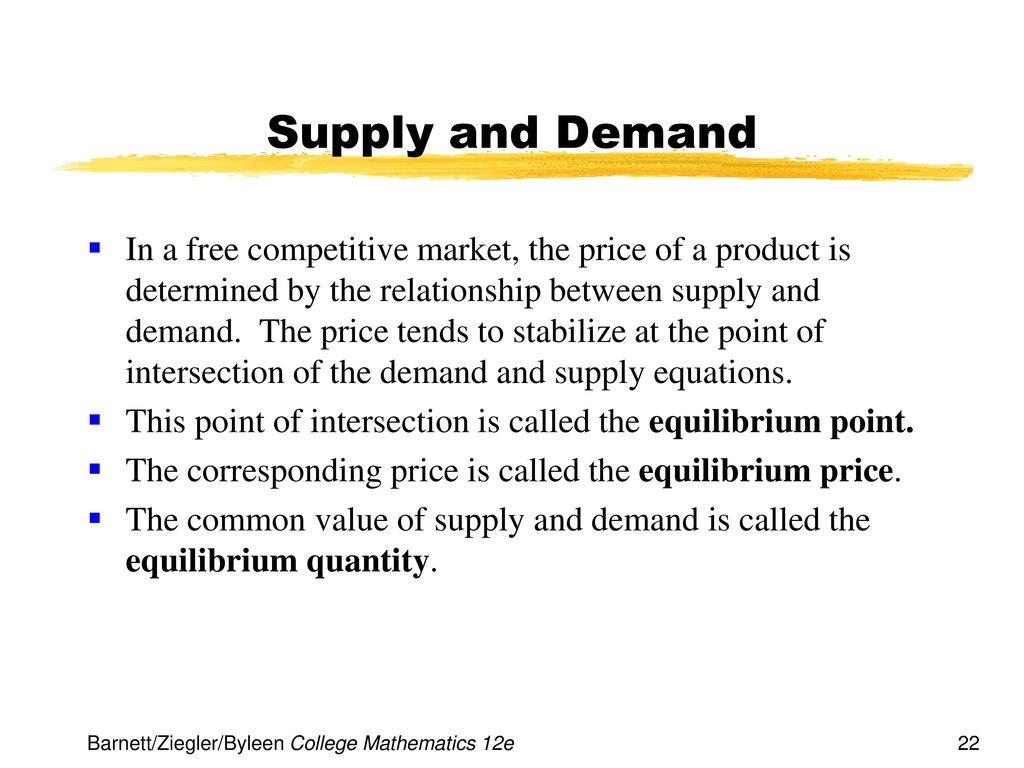

The Equilibrium: Where Supply and Demand Meet

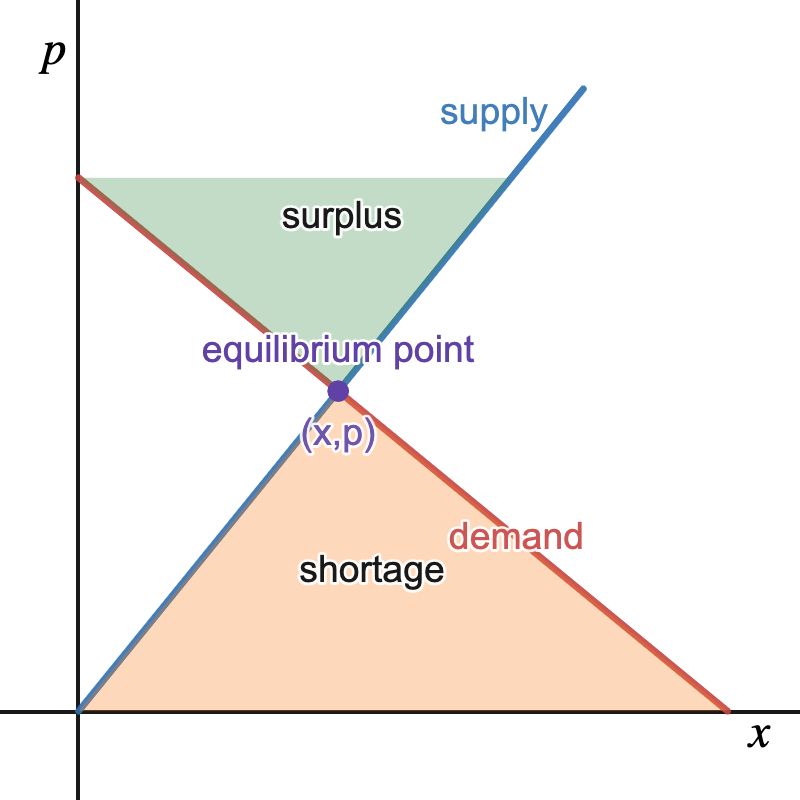

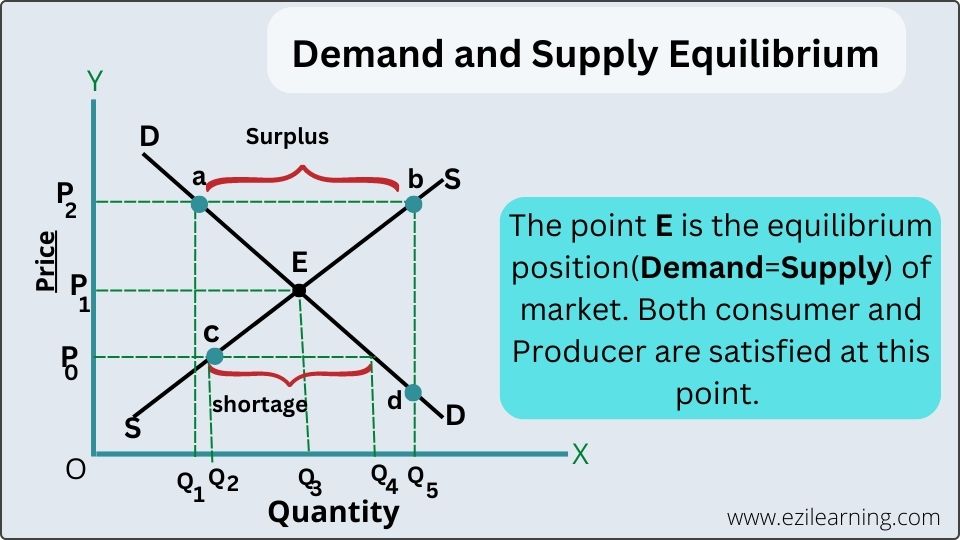

The equilibrium point is the sweet spot where the supply and demand curves intersect on a graph. At this price, the quantity supplied equals the quantity demanded, resulting in a balanced market. This point is also known as the market-clearing price.

When the price is above the equilibrium, a surplus occurs, with suppliers offering more than consumers are willing to buy. This forces sellers to lower prices to clear inventory, eventually moving the market towards equilibrium.

Conversely, when the price is below the equilibrium, a shortage arises, with consumers demanding more than suppliers can provide. This scarcity encourages sellers to raise prices, again pushing the market towards equilibrium.

According to Investopedia, "The equilibrium price is the only price where the plans of consumers and the plans of producers agree—that is, where the amount of the product consumers want to buy (quantity demanded) is equal to the amount producers want to sell (quantity supplied)."

Real-World Examples and Significance

The principles of supply and demand and their intersection are evident in numerous real-world scenarios. Consider the housing market. A surge in demand coupled with limited supply can drive up prices, creating a seller's market.

Conversely, an oversupply of apartments with sluggish demand can lead to lower rents and increased vacancies, favoring renters.

Another example is the oil market. Political instability, production disruptions, or increased global demand can all affect the equilibrium price of oil, impacting everything from gasoline prices to transportation costs.

Understanding the equilibrium point is crucial for businesses. It helps them determine optimal pricing strategies, predict market trends, and make informed production decisions. Ignoring these dynamics can lead to lost profits, unsold inventory, or missed opportunities.

Governments also rely on these principles when crafting economic policies. For instance, price controls, such as rent control or minimum wages, can disrupt the natural equilibrium and create unintended consequences like shortages or surpluses. According to the Congressional Budget Office (CBO), "Price controls can distort markets, leading to inefficiencies and unintended consequences."

The Dynamic Nature of Equilibrium

It is important to recognize that the equilibrium point is not static. It is constantly shifting as the forces of supply and demand fluctuate. Changes in consumer preferences, technological advancements, government policies, and global events can all disrupt the market and create new equilibrium prices and quantities.

For example, the rise of electric vehicles (EVs) is influencing the demand for gasoline-powered cars. As more consumers switch to EVs, the demand for gasoline decreases, leading to potentially lower prices and reduced production. Simultaneously, the demand for electricity and battery components increases, impacting those respective markets.

Businesses need to be agile and adapt to these dynamic changes to remain competitive. By closely monitoring market trends, analyzing consumer behavior, and adjusting their strategies accordingly, they can navigate the ever-evolving landscape of supply and demand.

Beyond the Numbers: Human Element

While the equilibrium point is often represented by graphs and equations, it is essential to remember the human element at play. Supply and demand are ultimately driven by the choices and actions of individuals, both consumers and producers.

Our desires, needs, and values shape the demand curve, while the creativity, innovation, and risk-taking of entrepreneurs drive the supply curve. The interaction between these forces creates a vibrant and dynamic economy.

Consider the ethical implications. The pursuit of profit through manipulating supply (e.g., price gouging during emergencies) can have detrimental effects on vulnerable populations. Similarly, unsustainable production practices can negatively impact the environment and future generations. A balanced understanding incorporates both economic principles and ethical considerations.

Conclusion

The point where supply and demand intersect, the equilibrium, is a fundamental concept that shapes our economic world. It is a dynamic balance, constantly adjusting to the ever-changing forces of the market. By understanding this principle, we gain a deeper appreciation for how prices are determined, how markets function, and how our individual choices contribute to the overall economic landscape.

As we navigate the complexities of the modern economy, remembering the interplay of supply and demand and the human element behind these forces allows us to make more informed decisions and contribute to a more sustainable and equitable future.