Which Of The Following Is A Result Of Cost Distortion

In the intricate world of business and economics, where razor-thin margins and precise calculations often determine success or failure, even subtle inaccuracies can have far-reaching consequences. Among the most insidious of these is cost distortion, a phenomenon that subtly warps financial landscapes, leading to flawed decision-making and potentially devastating outcomes.

The implications of cost distortion are significant. It can lead to misallocation of resources, poor pricing strategies, and ultimately, reduced profitability. Understanding the root causes and recognizing the resulting symptoms are crucial for businesses seeking to maintain a competitive edge.

Understanding Cost Distortion

Cost distortion arises when a company's costing system inaccurately assigns costs to products or services. This inaccuracy can stem from various factors, including the overuse of broad averages, outdated allocation methods, and a failure to account for the complexities of modern production processes. The result is a skewed view of profitability, where some products appear more profitable than they are, while others are unfairly burdened with excessive costs.

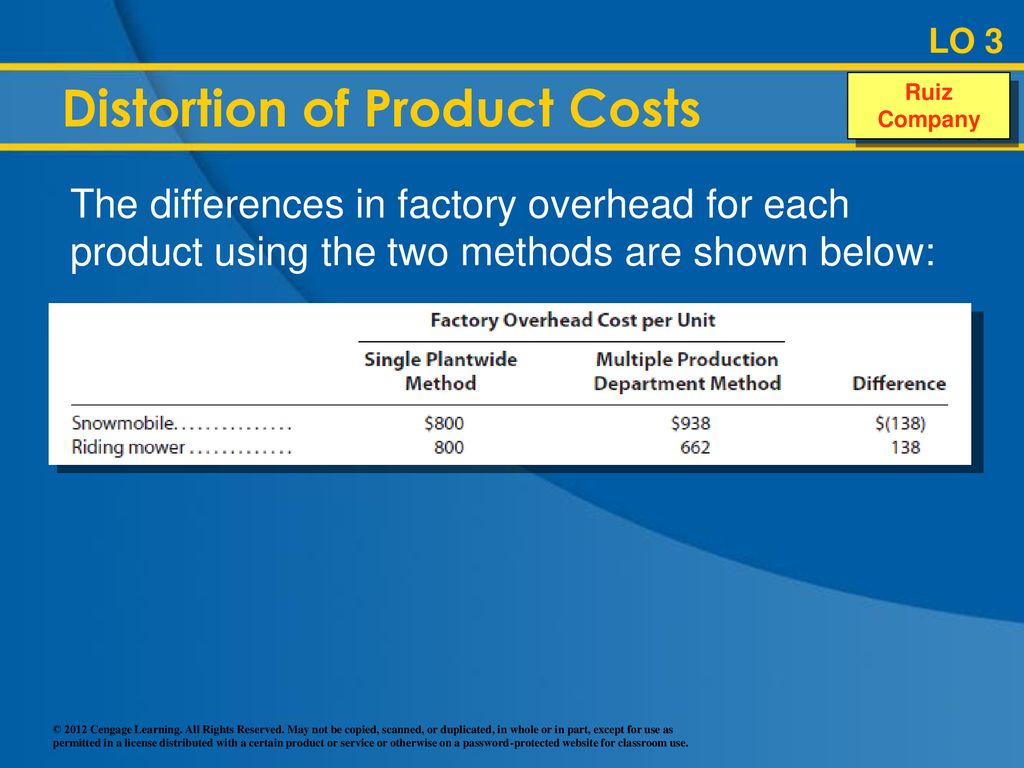

Imagine a bakery that allocates overhead costs based solely on the number of loaves of bread produced. This simple method might work if all products require roughly the same resources and processes. However, if the bakery also produces elaborate pastries that require significantly more labor and specialized equipment, the cost of these pastries will be understated, while the cost of the bread will be overstated.

This inaccurate cost allocation can lead to a range of problems.

The Consequences of Cost Distortion

One of the most significant results of cost distortion is misinformed pricing decisions. When a company underestimates the true cost of a product, it may set prices too low, leading to reduced profit margins or even losses. Conversely, overestimating costs can result in prices that are too high, potentially driving away customers and losing market share.

According to a study by the Institute of Management Accountants (IMA), companies using outdated costing systems are more likely to make poor pricing decisions compared to those using activity-based costing (ABC) or other more sophisticated methods.

Another key consequence is inefficient resource allocation. If a company believes that a particular product is highly profitable due to distorted cost data, it may allocate more resources to that product, even if other products offer a better return on investment. This misallocation can hinder overall profitability and limit growth potential.

Incorrect performance evaluation is yet another outcome. Managers whose performance is based on inaccurate cost data may be unfairly rewarded or penalized. This can lead to demotivation, poor decision-making, and a general erosion of trust within the organization. Consider a scenario where a division producing a high-volume, low-margin product is penalized for high overhead costs that are actually being driven by another, more complex division.

Furthermore, cost distortion can lead to poor product mix decisions. A company may choose to focus on producing and selling products that appear to be profitable based on distorted cost data, while neglecting other products that could generate higher profits if costs were accurately assigned. This can result in a suboptimal product portfolio and missed opportunities.

Examples in Action

In the manufacturing sector, companies that heavily rely on automated processes may experience cost distortion if they allocate overhead based solely on direct labor hours. The overhead costs associated with running and maintaining sophisticated machinery can be significantly higher than the direct labor costs, leading to an underestimation of the cost of products manufactured using automated processes and an overestimation of the cost of products manufactured using more labor-intensive methods.

Consider a software development company that allocates costs based on the number of programmers assigned to a project. This method fails to account for the different skill levels and experience of the programmers. A senior programmer may contribute significantly more value to a project than a junior programmer, but if costs are allocated solely on the number of programmers, the cost of the project will be understated, potentially leading to underpricing and reduced profitability.

Within the service industry, such as healthcare, cost distortion can arise when allocating overhead based on the number of patients seen. Different types of patients require different levels of care and resources. Patients with complex medical conditions require more time, specialized equipment, and skilled personnel, which can result in an underestimation of the cost of treating complex cases and an overestimation of the cost of treating simpler cases.

Mitigating Cost Distortion

Fortunately, there are several strategies that companies can employ to mitigate cost distortion. Implementing activity-based costing (ABC) is a powerful approach. ABC involves identifying the activities that drive costs and then allocating costs based on the consumption of these activities. This provides a more accurate and granular view of product costs.

Regularly reviewing and updating costing systems is also crucial. As business processes and technologies evolve, costing systems should be updated to reflect these changes. This ensures that cost allocations remain accurate and relevant. The American Institute of Certified Public Accountants (AICPA) recommends annual reviews of costing systems.

Improving data collection and analysis is another vital step. Accurate and detailed data is essential for effective cost management. Companies should invest in systems and processes that enable them to collect and analyze data on all aspects of their operations. This data can then be used to refine costing methods and identify areas for improvement.

Finally, fostering a culture of cost awareness throughout the organization is essential. Employees at all levels should be aware of the importance of accurate cost data and the impact of their actions on costs. Training and education programs can help to promote cost awareness and encourage employees to make cost-conscious decisions.

Looking Ahead

In an increasingly competitive and complex business environment, the importance of accurate cost management cannot be overstated. Cost distortion poses a significant threat to profitability and can lead to flawed decision-making. By understanding the causes and consequences of cost distortion and implementing appropriate mitigation strategies, companies can improve their financial performance and gain a competitive advantage.

As technology continues to evolve, new costing methods and tools are likely to emerge, offering even greater accuracy and insights. Companies that embrace these advancements will be well-positioned to navigate the challenges of cost management and thrive in the years ahead. The need for careful analysis and strategic thinking regarding cost allocation will only intensify, making it a critical area for businesses seeking sustainable success.

.jpg)