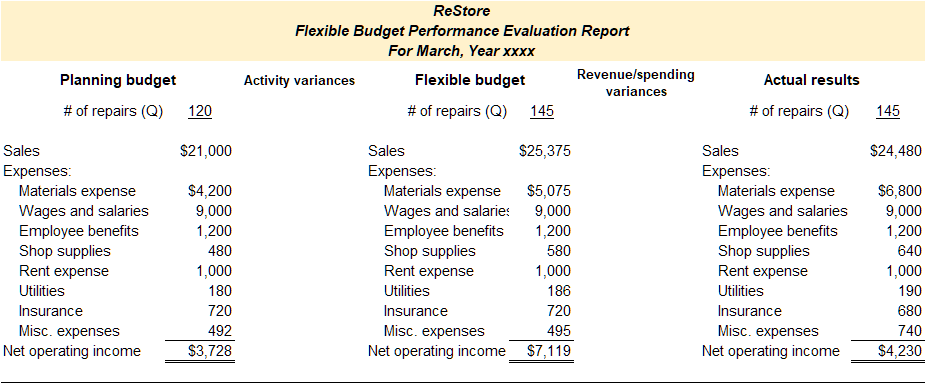

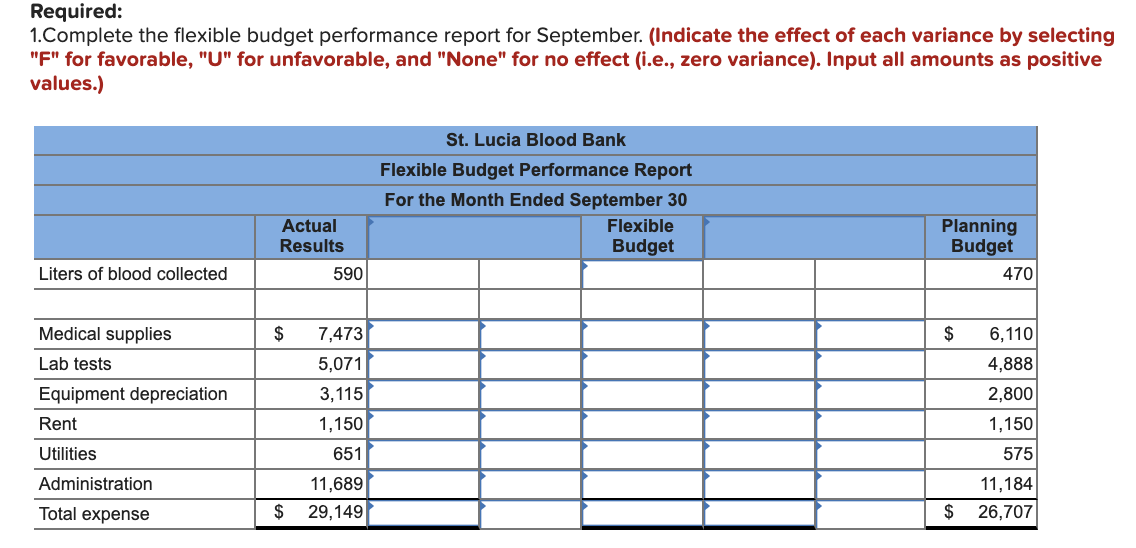

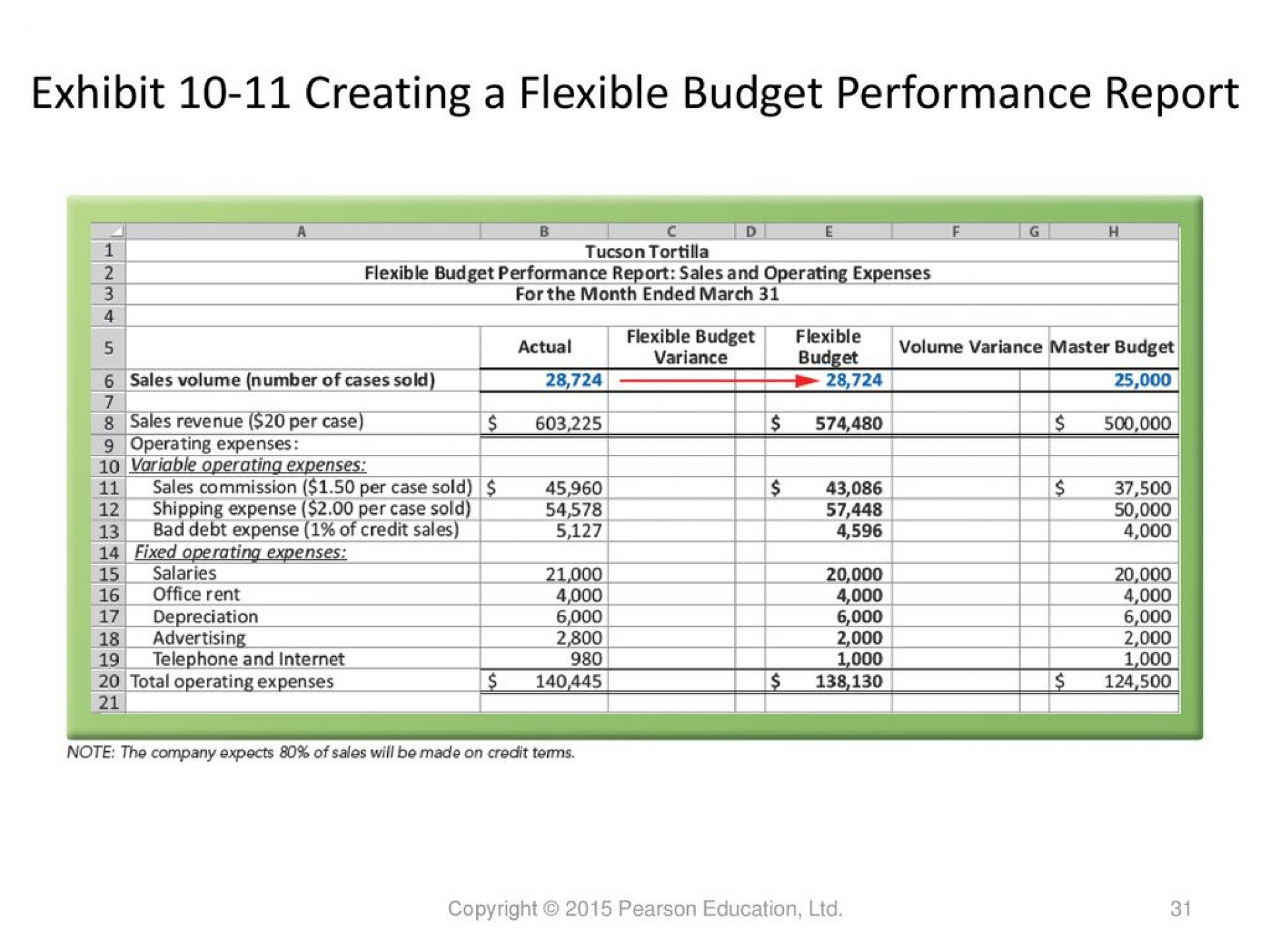

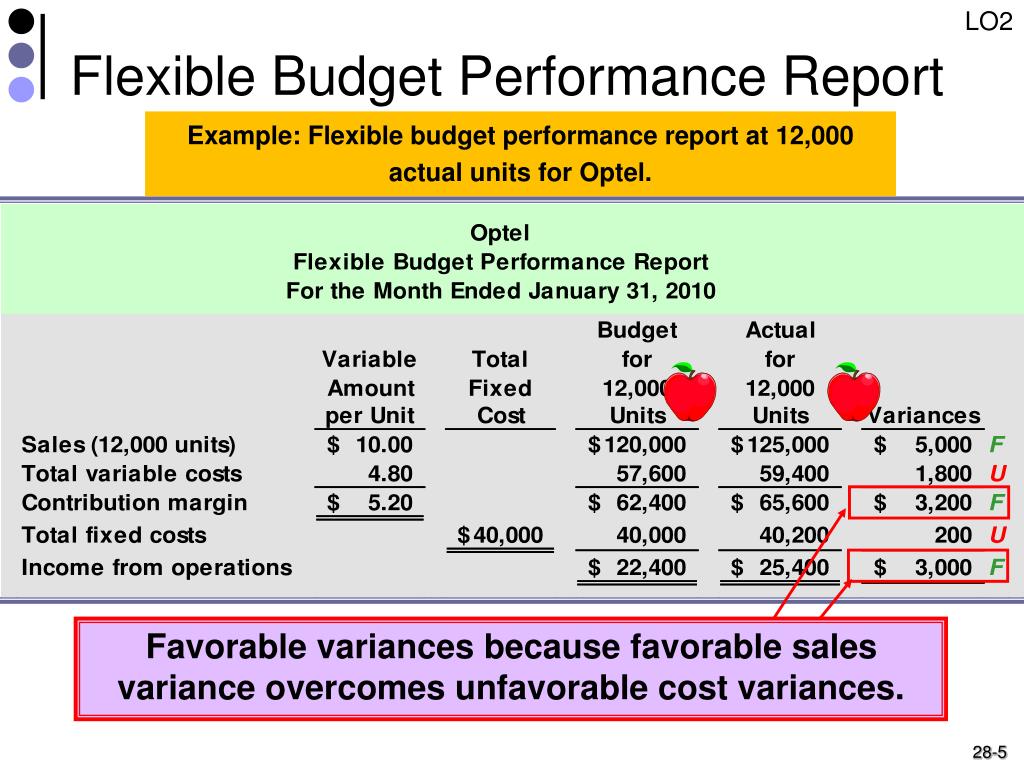

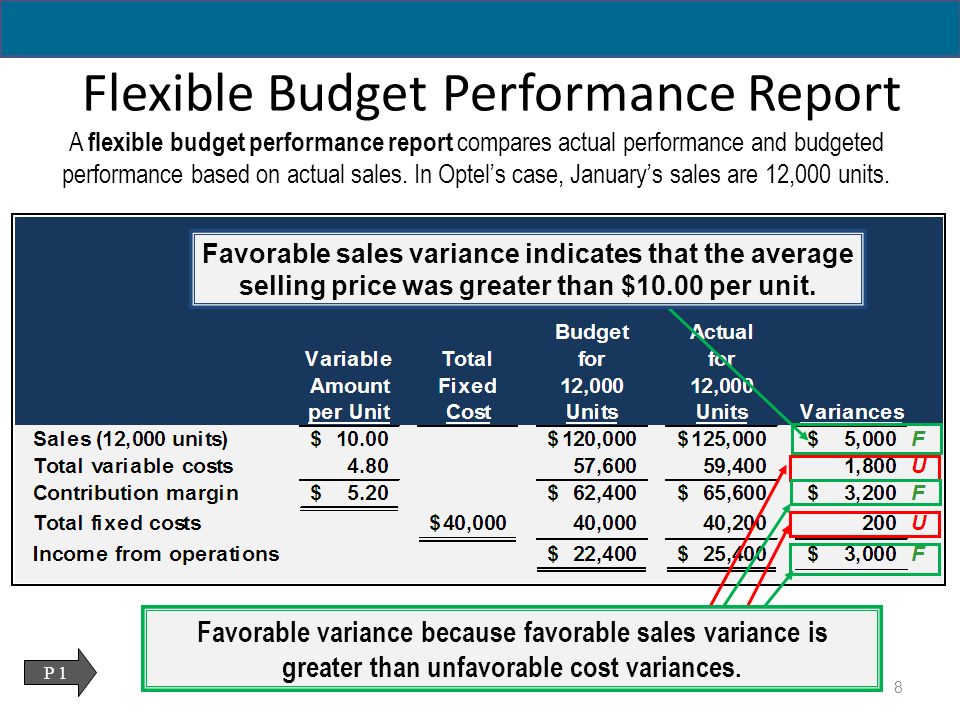

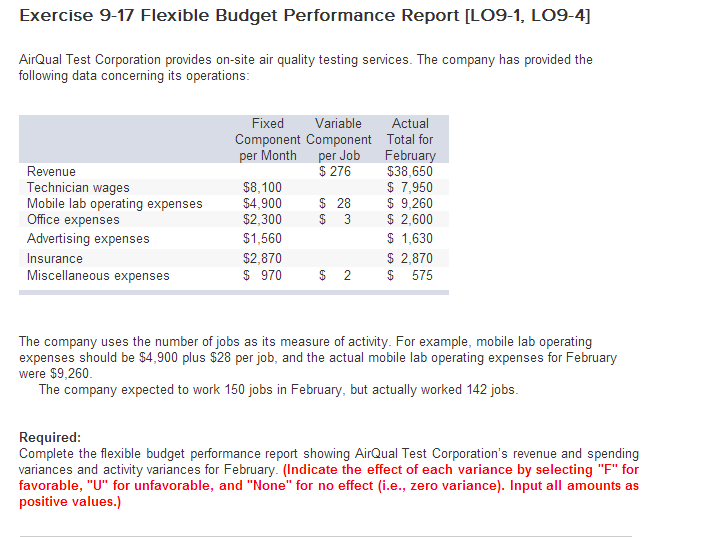

A Flexible Budget Performance Report Compares

In an era of unprecedented economic volatility, where supply chains fluctuate and consumer demand shifts on a dime, businesses are grappling with the challenge of maintaining profitability and accountability. Traditional budgeting methods, often rigid and based on static assumptions, are proving increasingly inadequate. The spotlight is now on a more dynamic tool: the flexible budget performance report.

At its core, the flexible budget performance report offers a nuanced comparison between actual results and what would have been expected given the actual level of activity, not the originally forecasted one. This allows for a more accurate assessment of managerial performance by isolating variances attributable to cost control, rather than simply penalizing managers for deviations arising from inaccurate sales projections. Its adaptability is becoming essential for navigating today's complex business landscape.

Understanding the Flexible Budget

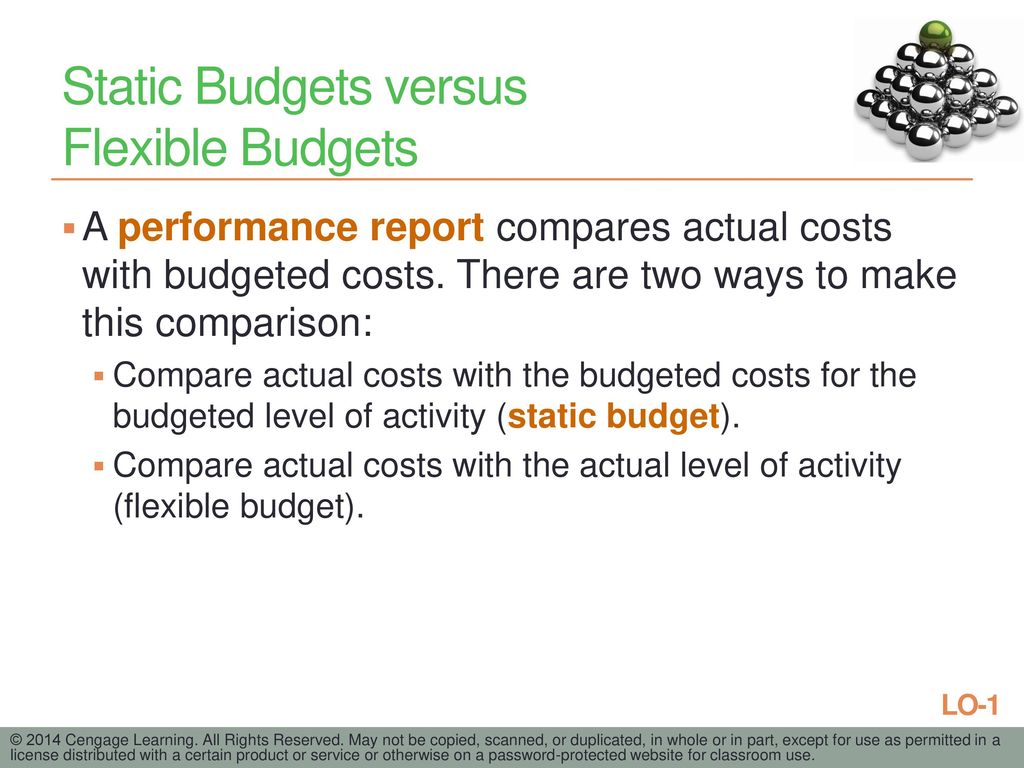

The traditional, or static, budget is prepared based on a predetermined level of activity. For example, a manufacturer might plan to produce 10,000 units of a product. All subsequent cost allocations and revenue expectations are built around this fixed production volume.

However, what if actual production falls short at 8,000 units, or exceeds expectations at 12,000? A flexible budget adjusts revenues and costs to reflect the actual level of activity achieved.

This adjustment is crucial. Imagine a scenario where sales are lower than expected due to unforeseen market downturn. A static budget will show an unfavorable variance across the board. A flexible budget, on the other hand, adjusts its projections based on the lower sales volume. It reveals whether unfavorable variances are driven by the market or by inefficiencies in operations.

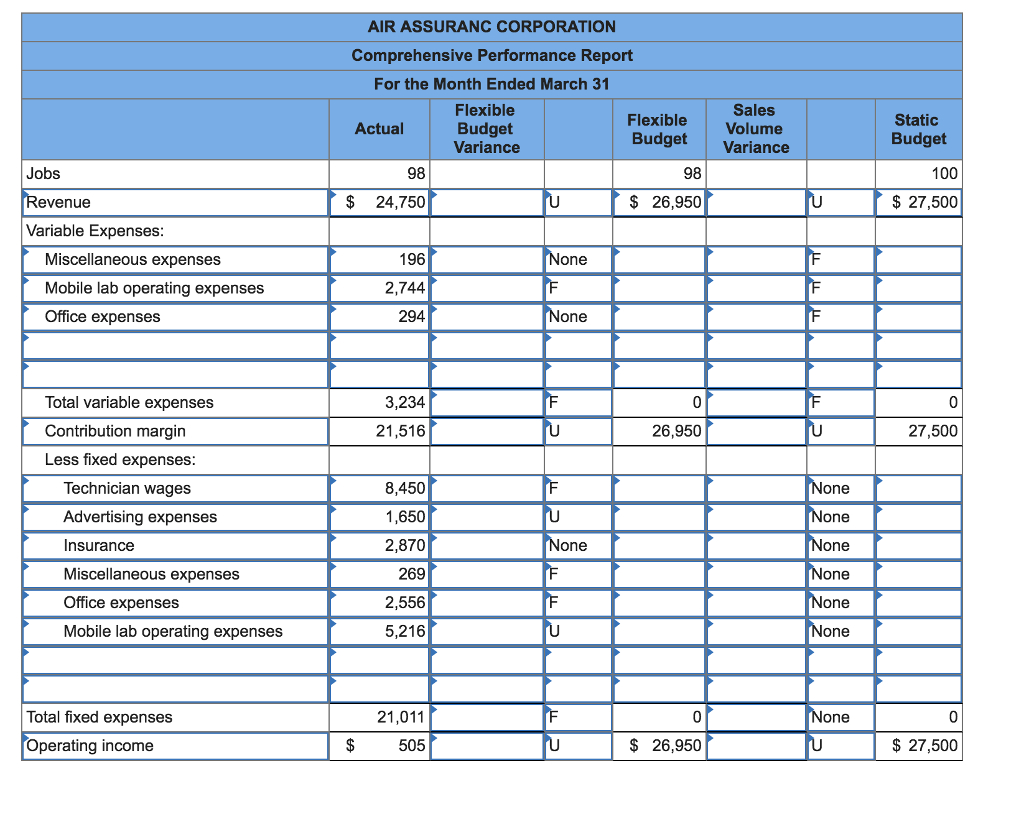

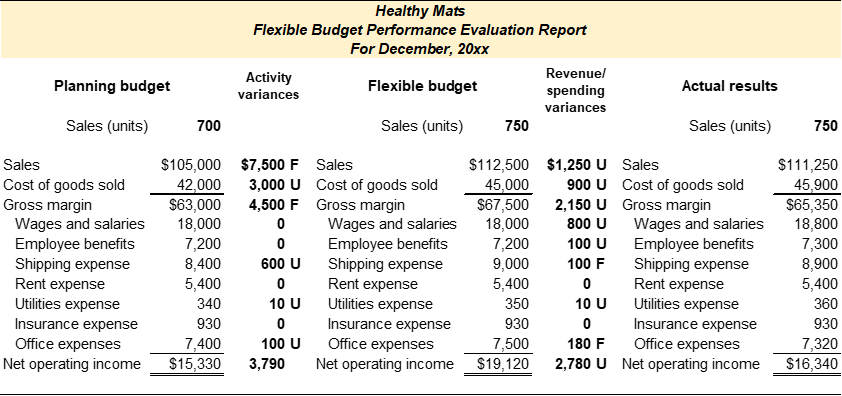

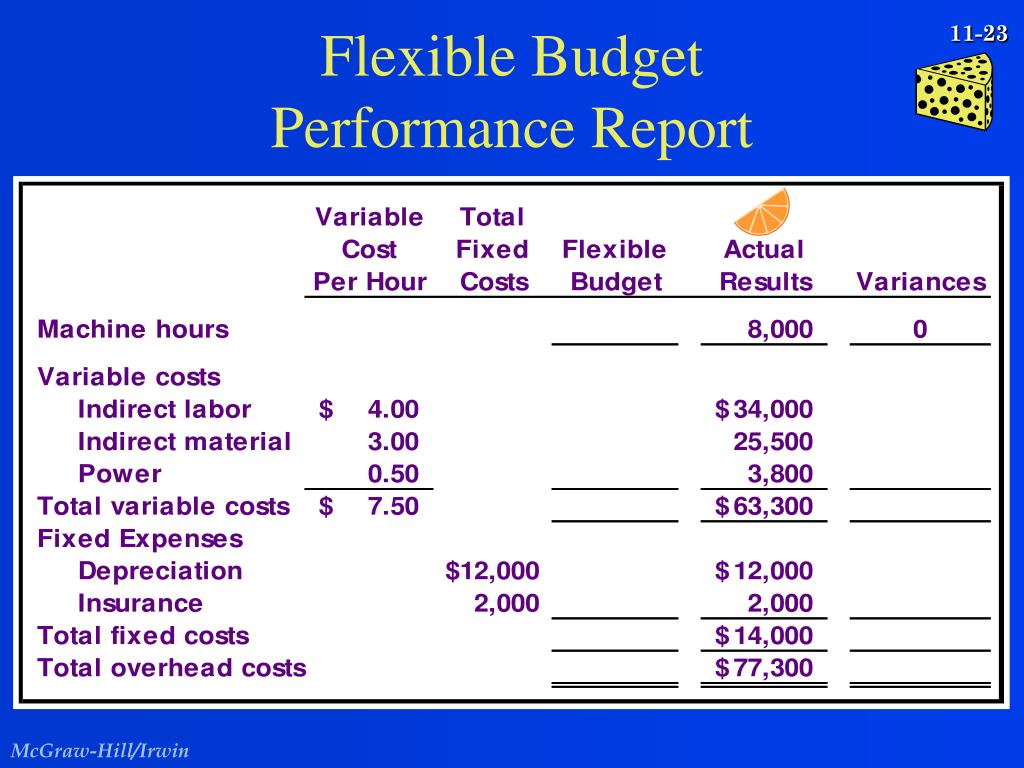

How the Flexible Budget Performance Report Works

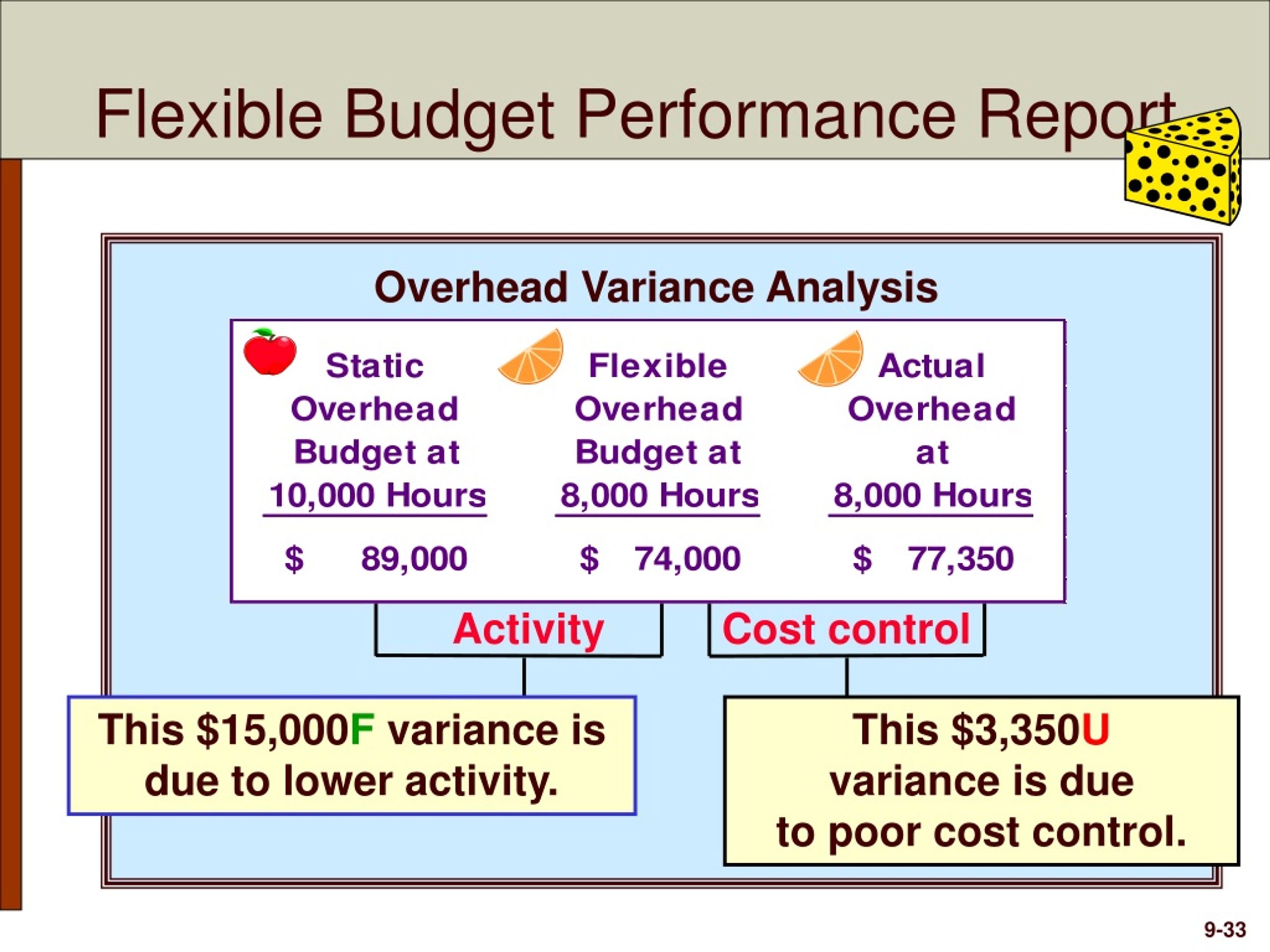

The flexible budget performance report typically presents a side-by-side comparison of the static budget, the flexible budget, and actual results. It isolates variances into two main categories: activity variances and spending variances.

Activity variances reflect the difference between the static budget and the flexible budget. These variances are solely due to the difference between the originally planned level of activity and the actual level of activity.

Spending variances, on the other hand, represent the difference between the flexible budget and the actual results. These variances are attributed to the effectiveness of cost control measures and operational efficiency, giving a better picture of actual performance.

The Benefits of Flexible Budgeting

The advantages of using a flexible budget performance report are multifaceted. Firstly, it provides a more realistic assessment of managerial performance.

By separating the impact of volume fluctuations from operational efficiencies, managers are evaluated on factors they can control. This can lead to increased motivation and accountability.

Secondly, flexible budgeting improves decision-making. By providing more accurate and timely information, management can identify problems quicker and implement corrective actions faster.

It also strengthens forecasting. As organizations gain experience with flexible budgeting, they can refine their cost behavior assumptions and improve the accuracy of future budgets.

Case Studies and Industry Adoption

Several companies have successfully implemented flexible budgeting, experiencing significant improvements in performance monitoring and cost control. For instance, a manufacturing firm specializing in custom-built machinery adopted flexible budgeting after struggling to accurately assess performance due to fluctuating order volumes.

Prior to the implementation, managers were consistently penalized for unfavorable variances arising from inaccurate sales forecasts. After switching to flexible budgeting, the firm was able to identify and address operational inefficiencies that were previously masked by volume variances.

Another notable example comes from the service industry. A hospital used flexible budgeting to better manage its staffing costs. By adjusting the budget based on patient volume, the hospital was able to avoid overstaffing during periods of low activity and understaffing during peak periods.

"Flexible budgeting has been a game-changer for us," says Dr. Emily Carter, the hospital's CFO. "It allows us to make data-driven decisions about staffing levels, ensuring that we provide high-quality patient care while controlling costs."

Challenges and Considerations

Despite its benefits, implementing flexible budgeting can pose several challenges. One of the biggest hurdles is accurately determining the cost behavior patterns. It requires a thorough understanding of which costs are fixed, variable, and mixed.

Another challenge is the increased complexity. Flexible budgeting requires more sophisticated accounting systems and a greater level of data analysis. This can place a strain on resources, particularly for smaller organizations.

Some argue that flexible budgets can be overly complex and difficult to understand for employees who are not familiar with accounting principles.

The Future of Budgeting

The rise of big data and artificial intelligence is poised to further revolutionize flexible budgeting. AI-powered tools can automate the process of analyzing cost behavior and generating flexible budgets, freeing up accounting professionals to focus on more strategic tasks.

Real-time data analytics can provide instant feedback on performance, allowing managers to make quicker decisions and respond more effectively to changing market conditions. Predictive analytics can be used to forecast future activity levels, improving the accuracy of budgets.

As businesses continue to navigate an uncertain economic landscape, the flexible budget performance report will become an increasingly essential tool for performance management and cost control. Its adaptability and focus on operational efficiency make it well-suited for today's dynamic business environment. The key will be in adapting the process to the specific needs of each organization and ensuring that the resulting information is used effectively to drive continuous improvement.