Debt Consolidation Loans Australia Bad Credit

For Australians grappling with the burden of multiple debts and a less-than-perfect credit history, the allure of debt consolidation loans can be strong. These loans promise a simplified path to financial stability, offering a single monthly payment and potentially lower interest rates. However, navigating the landscape of debt consolidation loans for bad credit requires careful consideration and a clear understanding of the associated risks and benefits.

Debt consolidation loans for individuals with bad credit represent a complex segment of the Australian financial market. They offer a potential solution to manage overwhelming debt, but their availability and terms are significantly different from those offered to borrowers with strong credit profiles.

Understanding the Landscape

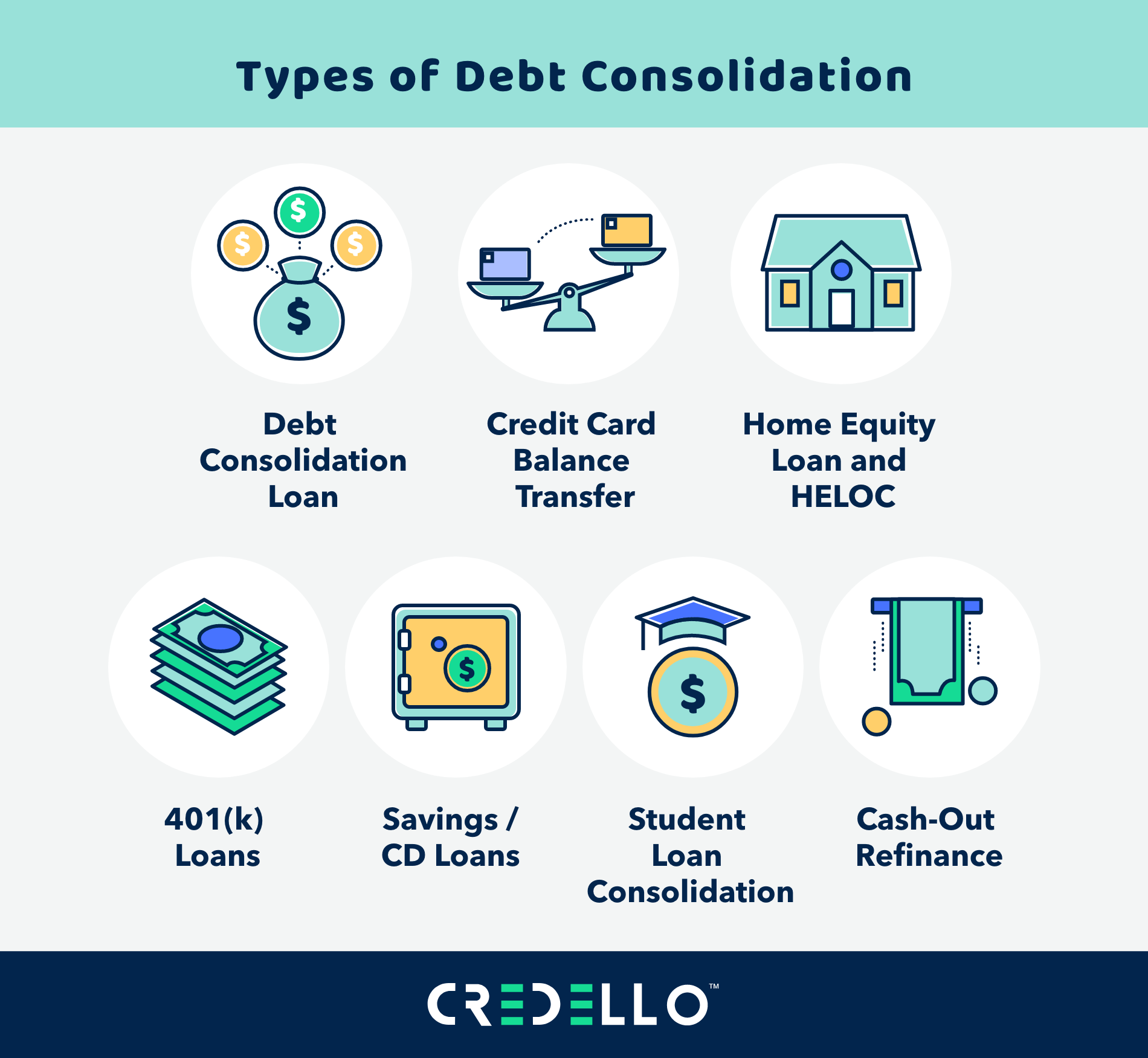

A debt consolidation loan combines multiple debts, such as credit cards, personal loans, and even some medical bills, into a single new loan. The borrower then makes one monthly payment, ideally at a lower interest rate than the combined rates of the original debts.

For individuals with poor credit scores, obtaining these loans presents unique challenges. Lenders perceive them as higher-risk borrowers, often leading to stricter eligibility criteria, higher interest rates, and additional fees.

The Australian Securities and Investments Commission (ASIC) recommends that consumers carefully assess their financial situation before taking on any debt, including debt consolidation loans. This includes evaluating the long-term cost of the loan and comparing offers from multiple lenders.

Who Offers These Loans?

A range of lenders in Australia provide debt consolidation loans to individuals with bad credit. These include traditional banks, credit unions, and online lenders specializing in subprime lending.

Non-bank lenders are often more willing to approve applications from individuals with impaired credit histories, but their interest rates and fees tend to be higher. Some lenders may require collateral, such as a home or car, as security for the loan.

It is crucial to research the lender's reputation and ensure they are licensed and regulated by the Australian Prudential Regulation Authority (APRA) or ASIC. Unlicensed lenders may engage in predatory lending practices, trapping borrowers in a cycle of debt.

The Costs Involved

The cost of a debt consolidation loan goes beyond the advertised interest rate. Borrowers should carefully consider all associated fees, including application fees, establishment fees, monthly account-keeping fees, and early repayment penalties.

High interest rates are a significant concern for individuals with bad credit. These rates can significantly increase the total cost of the loan, potentially offsetting any savings from consolidating debts.

Comparing the annual percentage rate (APR), which includes all fees and interest, is essential to accurately assess the true cost of the loan. A lower APR indicates a more affordable loan over the long term.

Potential Benefits

Despite the challenges, debt consolidation loans can offer several benefits to individuals with bad credit. One key advantage is simplified debt management, with a single monthly payment replacing multiple bills and due dates.

Consolidation may also improve cash flow if the new monthly payment is lower than the combined payments of the original debts. This can free up funds for essential expenses and help borrowers regain control of their finances.

For some, a debt consolidation loan can be a stepping stone toward improving their credit score. By making consistent, on-time payments, borrowers can demonstrate responsible financial behavior and gradually rebuild their creditworthiness.

Potential Risks

The risks associated with debt consolidation loans for bad credit are substantial. The high interest rates and fees can significantly increase the total cost of the debt, potentially making the situation worse.

If the loan is secured against an asset, such as a home, the borrower risks losing that asset if they default on the loan. This is a serious consideration and should be carefully evaluated before taking out a secured debt consolidation loan.

Another risk is the temptation to accumulate new debt after consolidating existing debts. If borrowers do not address the underlying causes of their debt, they may find themselves in a worse financial position than before.

Alternatives to Debt Consolidation

Before opting for a debt consolidation loan, individuals should explore alternative solutions. Credit counseling can provide valuable guidance and support in developing a debt management plan.

Negotiating with creditors to lower interest rates or set up payment plans can also be effective. Some creditors may be willing to work with borrowers who are struggling to repay their debts.

In some cases, bankruptcy may be the most appropriate solution. While bankruptcy has significant consequences, it can provide a fresh start for individuals overwhelmed by debt. It is important to seek professional legal advice before considering bankruptcy.

A Human Perspective

Sarah, a single mother from Melbourne, found herself struggling with mounting credit card debt after a job loss. "I was drowning in bills," she recounts. "The interest rates were crippling me."

After researching her options, Sarah opted for a debt consolidation loan. While the interest rate was higher than she would have liked, it was still lower than the combined rates of her credit cards. The single monthly payment also made it easier to manage her finances.

"It wasn't a magic bullet," Sarah admits. "But it gave me breathing room and allowed me to get back on my feet." She emphasizes the importance of budgeting and avoiding new debt after consolidating her existing debts.

Conclusion

Debt consolidation loans for bad credit can be a viable option for some Australians, but they are not a one-size-fits-all solution. A thorough assessment of the potential benefits and risks is essential before making a decision.

Seeking advice from a financial advisor or credit counselor is highly recommended. These professionals can provide personalized guidance and help borrowers make informed decisions about their financial future.

Ultimately, responsible borrowing habits and a commitment to financial discipline are crucial for long-term financial stability, regardless of whether a debt consolidation loan is used.