Direct Deposit Loans In Minutes No Credit Check

The allure of quick cash is powerful, especially for those facing unexpected expenses or financial hardship. A growing number of online lenders are capitalizing on this need, offering what they market as "direct deposit loans in minutes, no credit check required." These loans, often advertised heavily on social media and through targeted online ads, promise immediate access to funds without the traditional scrutiny of a credit report.

But are these promises too good to be true? This article delves into the world of these rapid-disbursement loans, examining their mechanics, potential benefits, inherent risks, and the regulatory landscape surrounding them.

What are "Direct Deposit Loans in Minutes"?

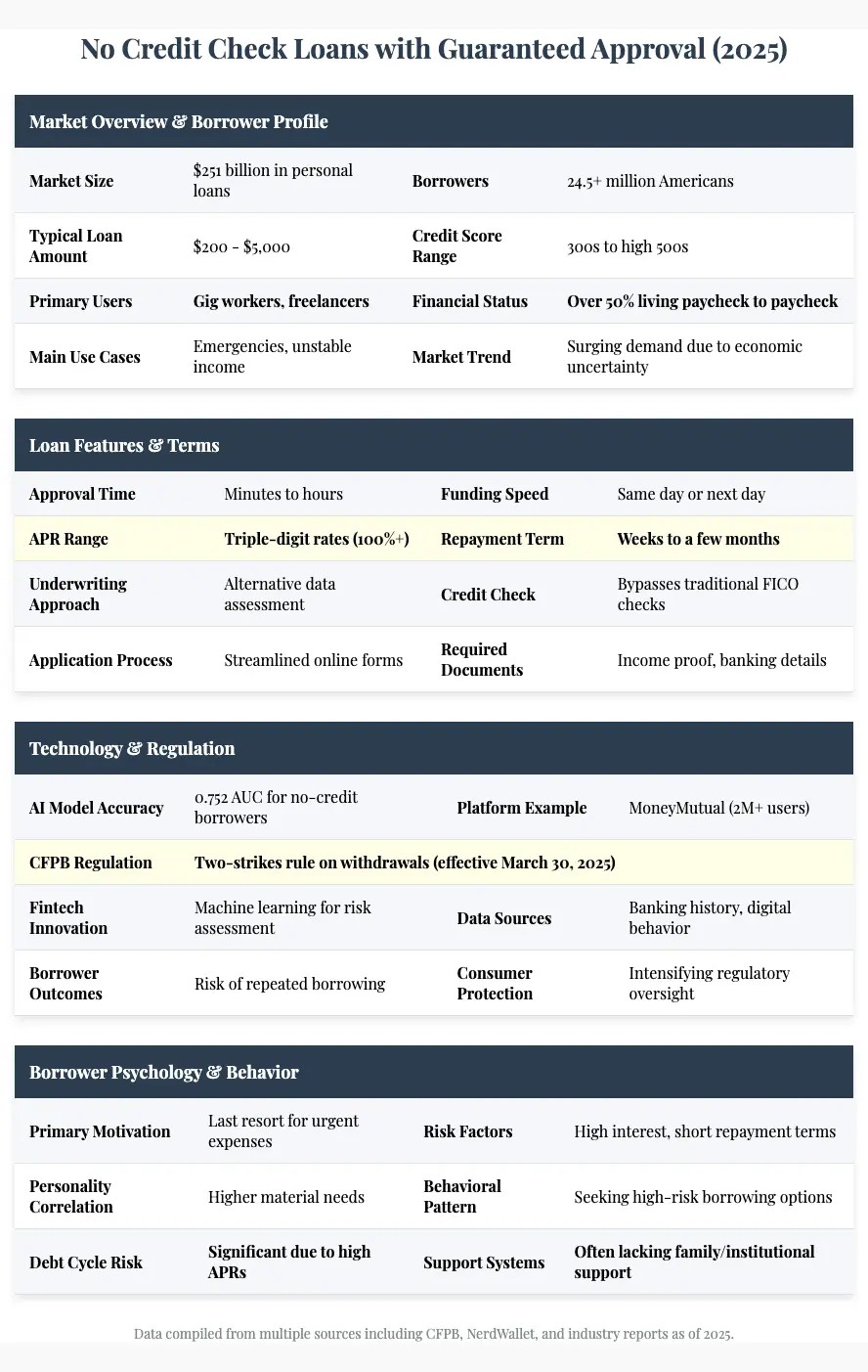

These loans, typically small-dollar loans ranging from $100 to $5000, are marketed as a solution for urgent financial needs. The appeal lies in their accessibility: borrowers can apply online, often receiving approval within minutes and the funds deposited directly into their bank accounts. The process often bypasses traditional credit checks, relying instead on factors like income verification or bank account history.

Companies offering these loans often highlight their speed and convenience. The ease of access is undeniable, especially for individuals with limited credit history or those who have been turned down by traditional lenders.

The Allure of No Credit Check

The "no credit check" aspect is a major draw for many borrowers. A credit check, a standard procedure in traditional lending, involves reviewing an individual's credit report to assess their creditworthiness. Individuals with low credit scores or limited credit history often struggle to qualify for conventional loans due to the perceived risk.

By forgoing credit checks, these lenders open their doors to a wider pool of potential borrowers. However, this convenience comes at a cost, usually in the form of substantially higher interest rates and fees.

The Reality of Rapid Loans: Risks and Concerns

While the promise of quick cash can be enticing, these loans often come with significant drawbacks. The absence of a credit check doesn't eliminate risk for the lender; it simply shifts the burden onto the borrower through higher costs.

Annual Percentage Rates (APRs) on these loans can be exorbitant, often exceeding 300% or even higher. This means that a borrower could end up paying back significantly more than the original loan amount, potentially trapping them in a cycle of debt. According to a 2023 report by the Consumer Financial Protection Bureau (CFPB), payday loans and similar short-term, high-interest loans can create "debt traps" for vulnerable consumers.

Furthermore, some lenders may engage in predatory lending practices. These practices can include hidden fees, unclear loan terms, and aggressive collection tactics, further exacerbating the borrower's financial difficulties. The Federal Trade Commission (FTC) warns consumers to be wary of lenders who are not transparent about their fees or who pressure borrowers into taking out loans.

The Human Cost

For individuals already struggling financially, these loans can create a spiral of debt. A single unexpected expense can trigger the need for a short-term loan, but the high interest rates and fees can quickly make it difficult to repay the loan on time. This can lead to late fees, additional interest charges, and ultimately, default. "I took out a $300 loan to cover a car repair," said *Maria Rodriguez*, a single mother. "But the interest was so high, I ended up paying back almost $900. It took me months to get back on my feet."

Regulatory Landscape and Consumer Protection

The regulation of these rapid-disbursement loans varies by state. Some states have strict usury laws that cap interest rates, while others have more lenient regulations. The lack of uniform regulation creates opportunities for lenders to operate in states with weaker consumer protections.

The CFPB has taken steps to regulate certain aspects of payday lending and other short-term loans, but more comprehensive federal regulation is needed to protect consumers from predatory lending practices. Advocacy groups like the Center for Responsible Lending are pushing for stronger consumer protections, including interest rate caps and stricter lending standards.

Alternatives to Rapid Loans

Before resorting to these high-cost loans, consumers should explore alternative options. These include seeking assistance from local charities or social service agencies, negotiating payment plans with creditors, or exploring options like personal loans from credit unions or community banks.

Building an emergency fund, however small, can also provide a buffer against unexpected expenses and reduce the need for short-term loans. Seeking financial counseling can help individuals develop a budget and manage their finances more effectively, preventing future reliance on predatory lending.

Conclusion

While the allure of "direct deposit loans in minutes, no credit check" is undeniable, consumers must proceed with caution. The convenience and speed of these loans often come at a steep price, potentially trapping borrowers in a cycle of debt. Understanding the risks, exploring alternatives, and advocating for stronger consumer protections are crucial steps in navigating the complex world of short-term lending. The promise of instant cash should not overshadow the potential for long-term financial hardship.