Loans For Bad Credit In Florida

Imagine the Florida sun beating down, not just on pristine beaches and bustling theme parks, but on the quiet anxieties of individuals striving to build a better financial future. Perhaps it's Maria in Miami, a single mother dreaming of opening a small bakery, or David in Orlando, hoping to repair his aging car to get to his new job. Both face a common hurdle: a less-than-perfect credit score.

This article explores the landscape of loans for individuals with bad credit in Florida, shedding light on the options available, the challenges they present, and the crucial steps borrowers can take to navigate this often-complex financial terrain. While obtaining loans with poor credit is undeniably more difficult, it's far from impossible, and understanding the available avenues is the first step towards achieving financial goals.

Understanding the Florida Credit Landscape

Florida, like the rest of the nation, operates within a credit-based system. A credit score, a numerical representation of your creditworthiness, plays a significant role in determining loan eligibility and interest rates.

A lower score, often resulting from past financial missteps, can limit access to traditional loans and credit lines. This creates a barrier for many Floridians who are working to rebuild their financial lives.

What Constitutes "Bad Credit"?

Generally, a credit score below 630 is considered "bad" or "poor" by most lenders. FICO scores, the most widely used credit scoring model, range from 300 to 850.

Experian, one of the three major credit bureaus, categorizes scores below 580 as "very poor," 580-669 as "fair," 670-739 as "good," 740-799 as "very good," and 800-850 as "exceptional." The lower your score, the higher the perceived risk for lenders.

Why is Credit Important?

Credit isn't just about loans. It affects various aspects of life, from renting an apartment to securing insurance policies. A good credit history can unlock opportunities and save money on interest rates.

Navigating Loan Options for Bad Credit

Despite the challenges, several loan options are available to individuals with bad credit in Florida. Each comes with its own set of terms, conditions, and risks.

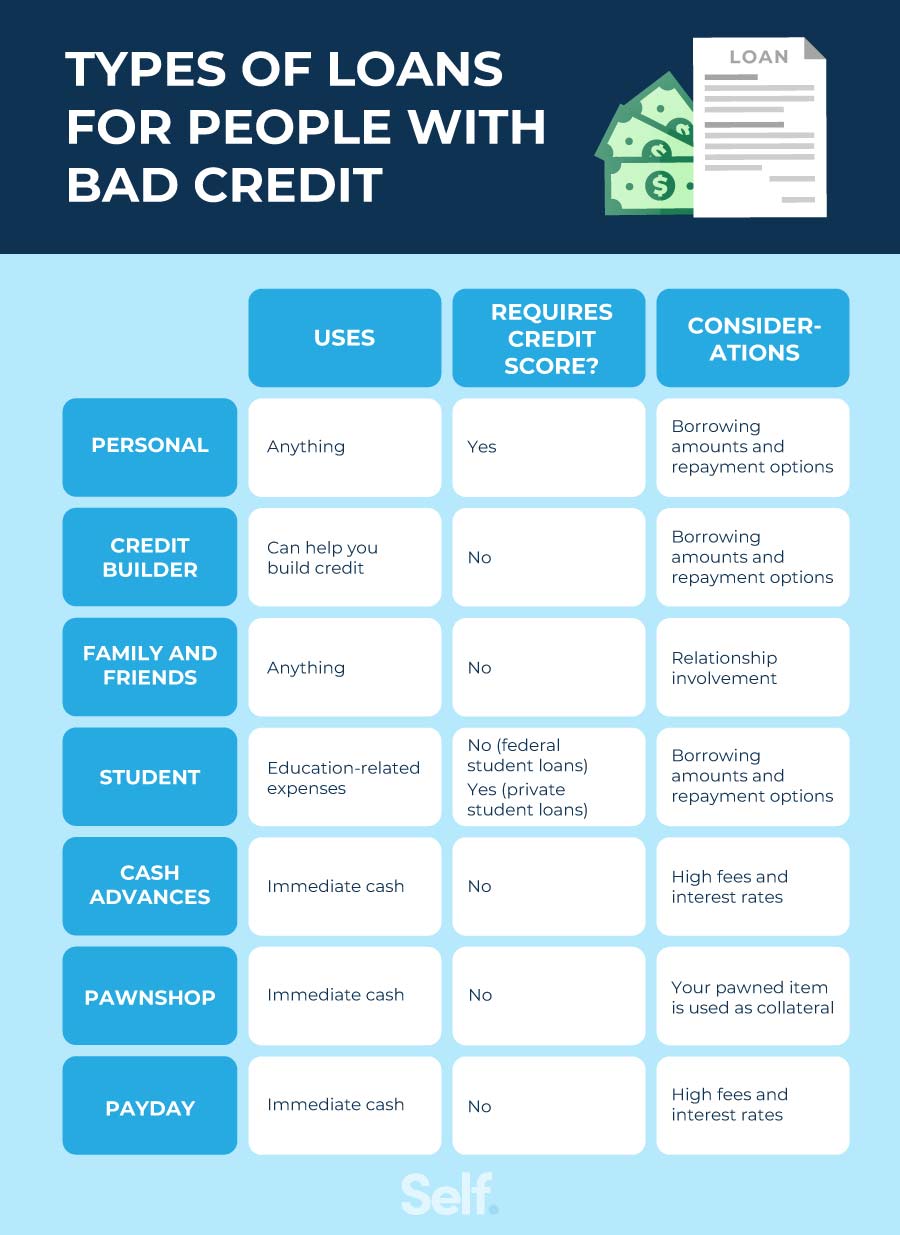

Secured Loans

Secured loans are backed by collateral, such as a car, home, or savings account. This reduces the risk for the lender, making them more willing to approve borrowers with lower credit scores.

However, if the borrower defaults on the loan, the lender can seize the collateral to recoup their losses. Car title loans and pawnshop loans are examples of secured loans often used by individuals with bad credit. Be aware that these loans often come with extremely high interest rates and fees.

Unsecured Loans

Unsecured loans, such as personal loans from online lenders, don't require collateral. Because of the increased risk, lenders typically charge higher interest rates and fees for these loans.

While the interest rates can be high, they may still be lower than those associated with payday loans or car title loans. It's crucial to carefully compare the terms and conditions of different lenders before making a decision.

Payday Loans

Payday loans are short-term, high-interest loans designed to be repaid on the borrower's next payday. These loans are readily available but come with exorbitant fees and APRs (Annual Percentage Rates), often exceeding 300% or even 400%.

Consumer advocacy groups consistently warn against using payday loans, as they can quickly lead to a cycle of debt. While they might seem like a quick fix, they can have long-term negative consequences.

Credit Union Loans

Credit unions are non-profit financial institutions that often offer more favorable loan terms than traditional banks or online lenders. They may be more willing to work with individuals who have bad credit, especially if the borrower is a member with a good standing.

Membership requirements vary, but often include living, working, or belonging to a specific group in the area. Credit unions prioritize member service and may offer financial counseling to help borrowers improve their credit.

Co-signed Loans

A co-signed loan involves another person with good credit agreeing to be responsible for the loan if the borrower defaults. This can increase the chances of approval and potentially lower the interest rate.

However, it's important to remember that the co-signer is equally liable for the debt, and their credit score will be affected if the borrower fails to make payments. Honesty and open communication are crucial in co-signing arrangements.

The Role of Online Lenders

Online lenders have become a significant player in the bad credit loan market. They often offer a wider range of loan products and may have less stringent requirements than traditional banks.

While the convenience of online lending is appealing, it's essential to be wary of predatory lenders and scams. Always verify the lender's legitimacy and read reviews before providing any personal information.

Protecting Yourself from Predatory Lending

Predatory lenders target individuals with bad credit, offering loans with exorbitant interest rates, hidden fees, and unfair terms. These practices can trap borrowers in a cycle of debt, making it even harder to improve their financial situation.

Warning signs of predatory lending include: high-pressure sales tactics, lack of transparency about loan terms, and requiring upfront fees before providing the loan. The Florida Office of Financial Regulation is a resource for consumers to learn about their rights and report predatory lending practices.

Improving Your Credit Score

While securing a loan with bad credit might be necessary in the short term, the long-term goal should be to improve your credit score. A better credit score opens doors to more favorable loan terms and financial opportunities.

Strategies for improving your credit score include: paying bills on time, reducing credit card balances, disputing errors on your credit report, and avoiding opening too many new credit accounts at once.

Consider consulting with a non-profit credit counseling agency for personalized guidance on managing debt and improving your credit. The National Foundation for Credit Counseling (NFCC) is a reputable organization that provides free or low-cost credit counseling services.

Looking Ahead: Financial Empowerment

Securing a loan with bad credit in Florida can be a challenging but achievable step towards financial stability. By understanding the available options, protecting themselves from predatory lending, and actively working to improve their credit score, Floridians can take control of their financial future.

It's a journey of perseverance, informed decisions, and a commitment to building a brighter financial horizon, one step at a time. Like Maria and David, who represent many others across the Sunshine State, the path to financial freedom begins with knowledge and action.

/cloudfront-us-east-1.images.arcpublishing.com/dmn/VQTVMZKYXBBLVECIAWNZC46WME.jpg)