Loans In Texas With Bad Credit

Texas residents with poor credit face an uphill battle securing necessary loans. High interest rates and restrictive terms exacerbate financial struggles for those already vulnerable.

This report examines the precarious lending landscape for Texans with bad credit, revealing the limited options, predatory practices, and urgent need for consumer protections.

The Harsh Reality of Bad Credit Loans in Texas

Texans with credit scores below 620 often find themselves locked out of traditional lending avenues. Banks and credit unions typically require higher scores, forcing individuals to seek alternative, often riskier, options.

Payday loans, auto title loans, and installment loans are common, but these come with exorbitant interest rates, sometimes exceeding 400% APR. The Center for Responsible Lending has documented numerous cases of Texans trapped in cycles of debt due to these high-cost loans.

Who is Affected?

Low-income individuals, minority communities, and those experiencing job loss are disproportionately affected. Data from the Texas Office of Consumer Credit Commissioner shows a concentration of high-cost lenders in areas with higher poverty rates.

These communities often lack access to financial literacy resources and are more vulnerable to predatory lending practices. The situation is further complicated by the lack of state regulations capping interest rates on many types of loans.

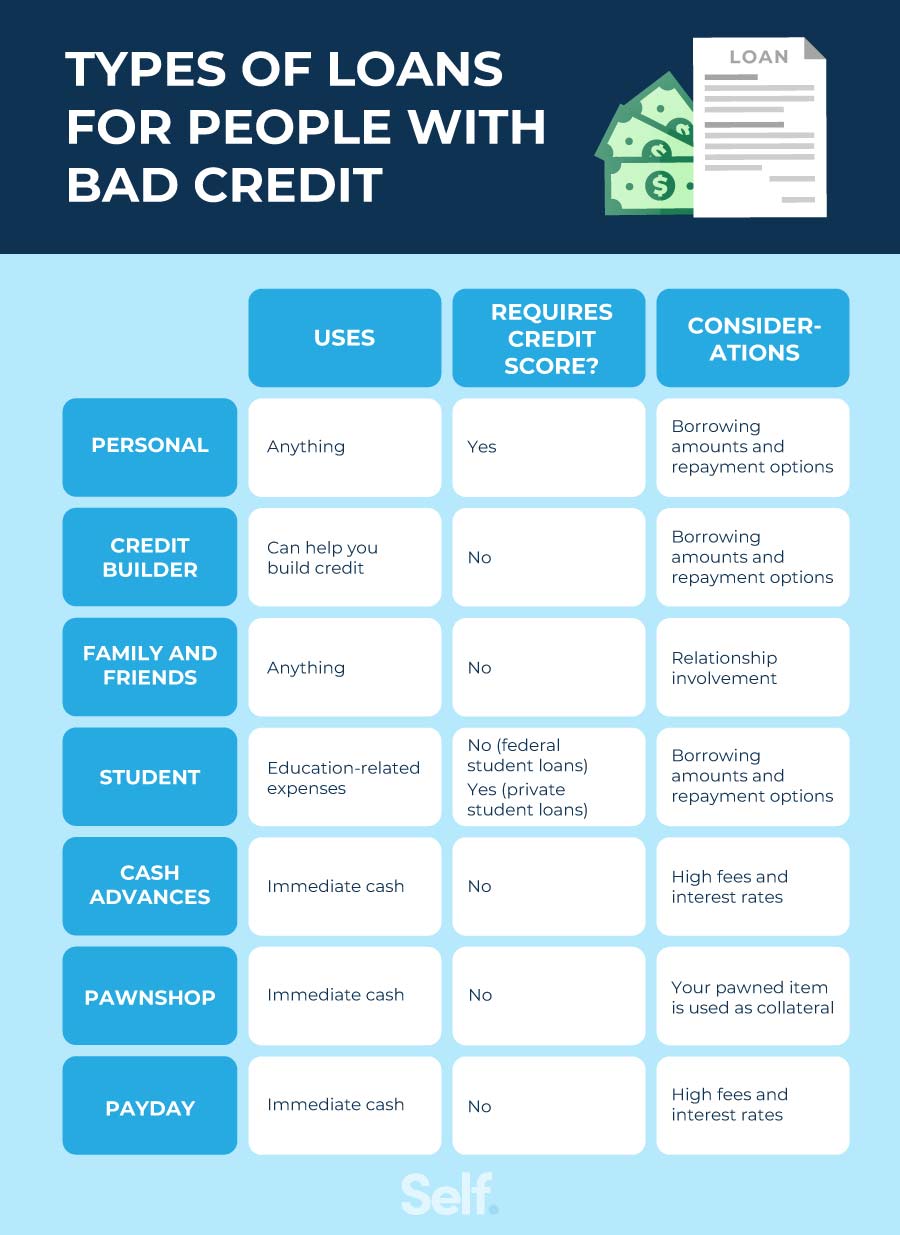

What Are the Available Loan Options?

Besides payday and title loans, some online lenders offer personal loans for borrowers with bad credit. However, these loans often come with high fees and interest rates, making them a costly long-term solution.

Credit unions may offer small-dollar loans with more reasonable terms, but eligibility requirements can be stringent. Secured loans, requiring collateral like a vehicle or property, may be an option, but risk asset loss if the borrower defaults.

Where Are These Loans Offered?

Payday and title loan stores are prevalent throughout Texas, particularly in urban areas and along major highways. Online lenders operate across the state, often targeting consumers through aggressive marketing campaigns.

The Texas Fair Lending Alliance reports that many of these lenders operate in areas with limited access to traditional banking services, creating a financial desert for vulnerable populations.

When is the Situation Most Critical?

The need for bad credit loans often arises during emergencies, such as unexpected medical bills, car repairs, or job loss. These urgent situations leave individuals with little time to shop around for the best possible terms.

The current economic climate, with rising inflation and stagnant wages, is exacerbating the problem. More Texans are finding themselves in precarious financial situations and turning to high-cost loans as a last resort.

How Do These Loans Work?

Payday loans typically require repayment within two weeks, often coinciding with the borrower's next paycheck. Title loans use the borrower's vehicle as collateral, allowing the lender to repossess the vehicle if the loan is not repaid.

Installment loans offer longer repayment periods, but the high interest rates can still result in borrowers paying significantly more than the original loan amount. Many borrowers fail to fully understand the terms and conditions of these loans before signing the agreement.

Consumer Protection and Advocacy

Consumer advocacy groups are urging state lawmakers to enact stricter regulations on high-cost lenders. Capping interest rates and requiring lenders to assess borrowers' ability to repay are key priorities.

The Consumer Financial Protection Bureau (CFPB) has also taken steps to protect consumers from predatory lending practices. However, the lack of state-level regulation leaves many Texans vulnerable.

Next Steps and Ongoing Developments

The Texas Legislature is currently considering several bills aimed at reforming the state's lending laws. The outcome of these legislative efforts will have a significant impact on the availability and affordability of credit for Texans with bad credit.

Consumers struggling with debt should seek assistance from non-profit credit counseling agencies. These agencies can provide guidance on budgeting, debt management, and alternative loan options.

The fight for fair lending practices in Texas is ongoing, and continued advocacy is crucial to protect vulnerable consumers from predatory loans. Texans need to be informed and proactive in safeguarding their financial well-being.

/cloudfront-us-east-1.images.arcpublishing.com/dmn/VQTVMZKYXBBLVECIAWNZC46WME.jpg)