The Accounting Cycle Includes All Of The Following Except

Accounting students and professionals are facing widespread confusion over a deceptively simple question: "The accounting cycle includes all of the following except..." The ambiguity surrounding the correct answer is causing significant anxiety and raising questions about the clarity of accounting education materials.

The core issue revolves around differing interpretations and omissions in textbooks and online resources. This situation is hindering accurate understanding and application of fundamental accounting principles, with potential long-term consequences for financial reporting accuracy across various industries.

Widespread Confusion Among Students

Reports are flooding in from universities and colleges nationwide indicating widespread student frustration. Many students, prepped with standard textbook definitions, are finding themselves marked wrong on assignments and tests. The recurring question: "The accounting cycle includes all of the following except..." is consistently cited as the source of the confusion.

A recent survey of accounting students conducted by the National Association of Accounting Students (NAAS) revealed that over 70% of respondents felt inadequately prepared to answer the question accurately. Students consistently reported that their study materials did not adequately address nuanced aspects of the accounting cycle.

What's Included and What's Not?

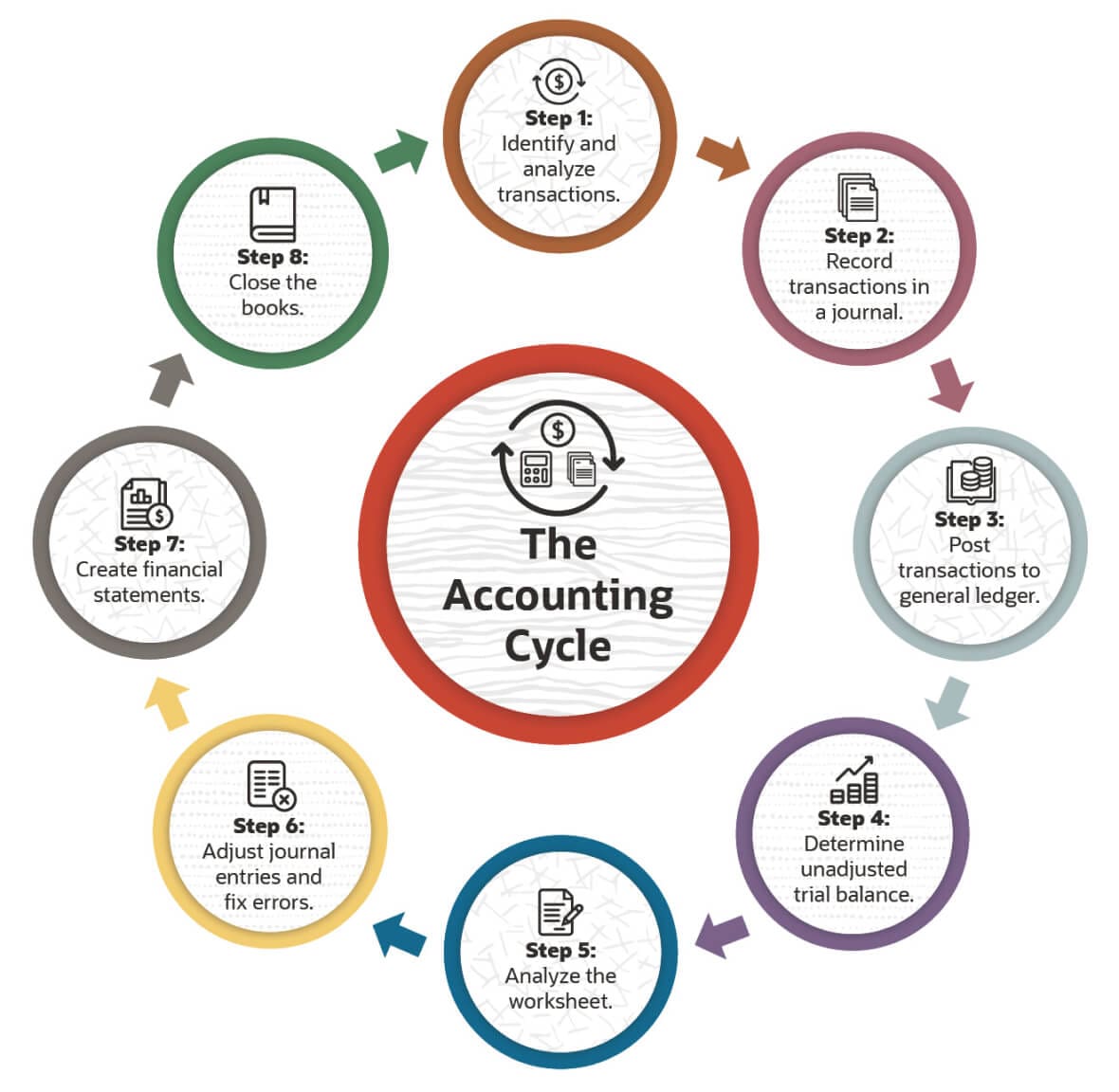

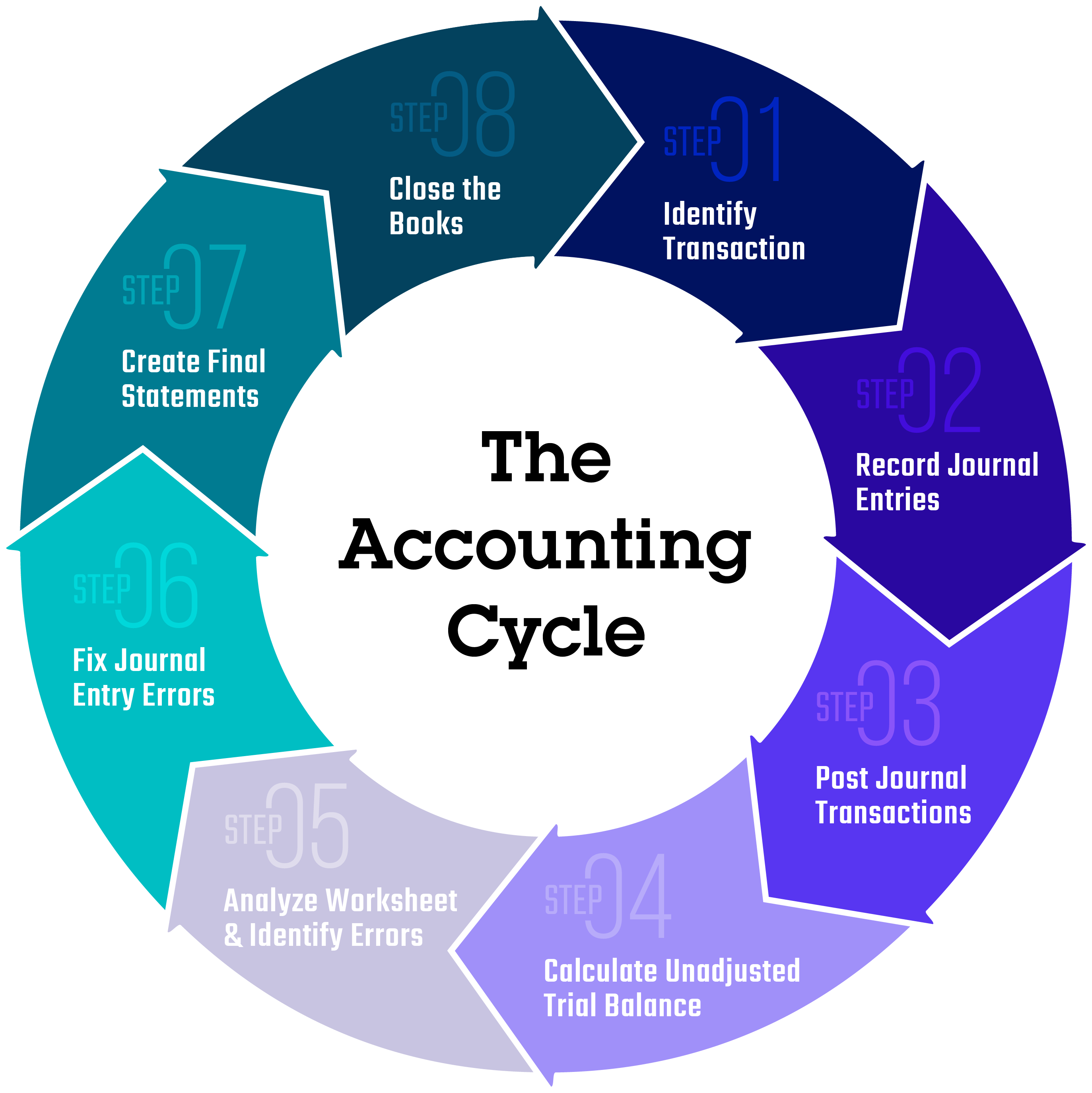

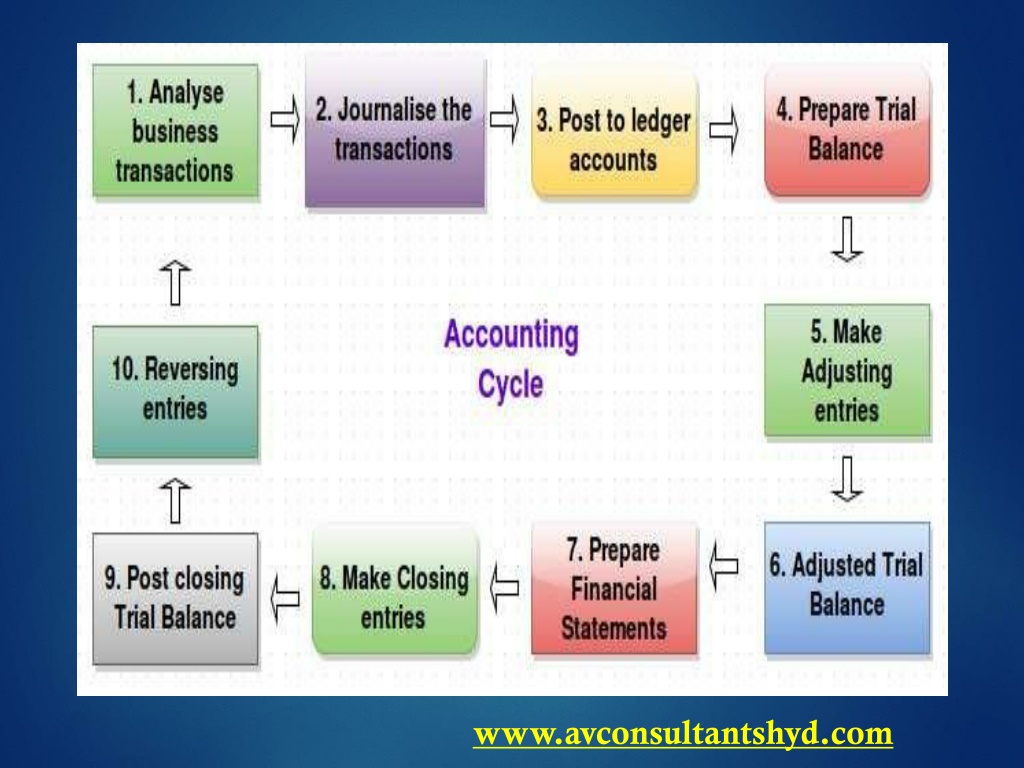

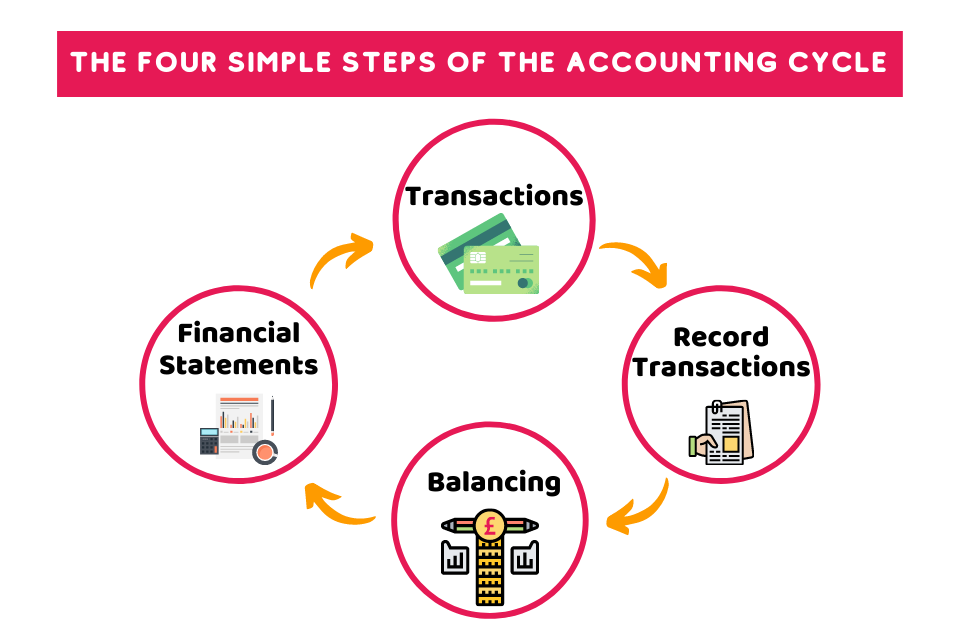

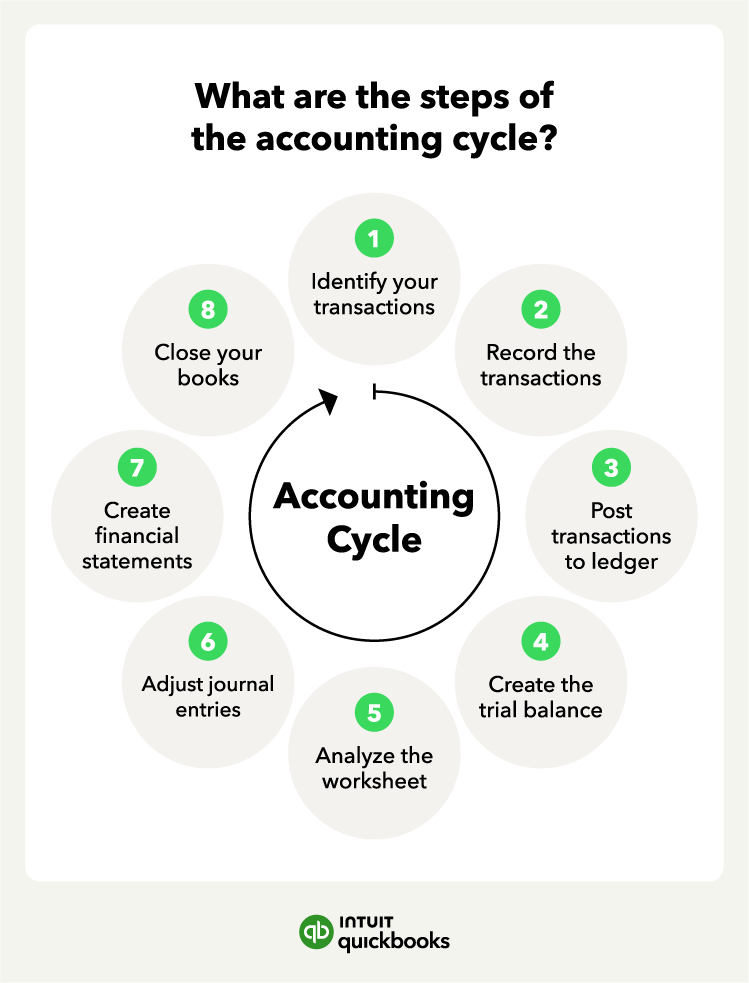

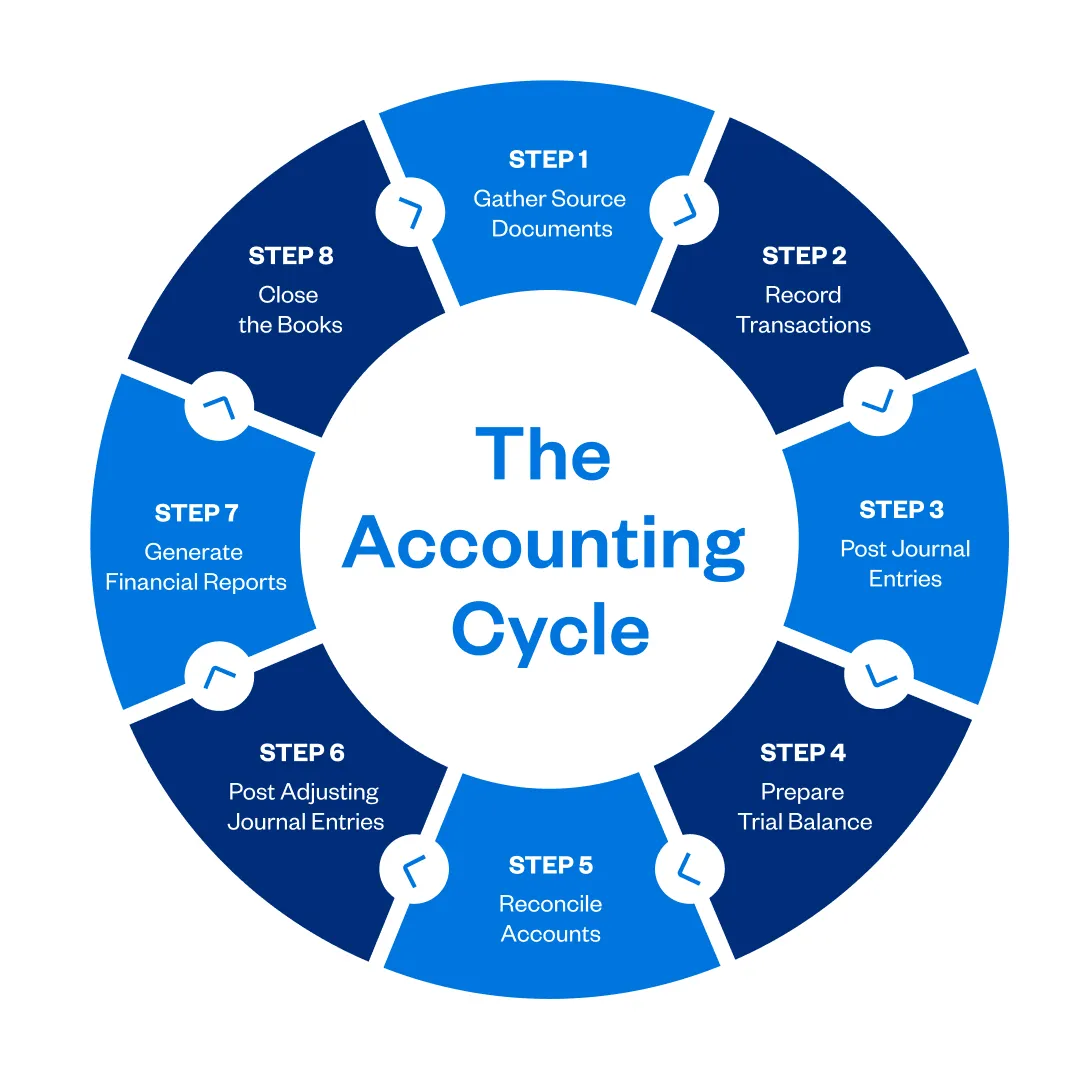

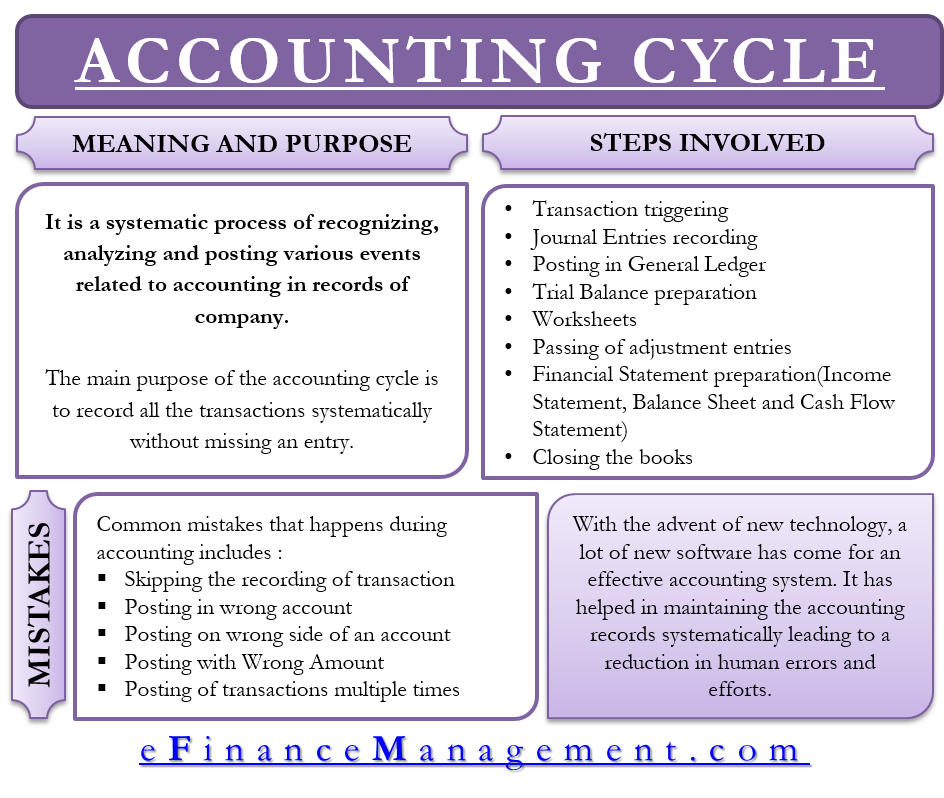

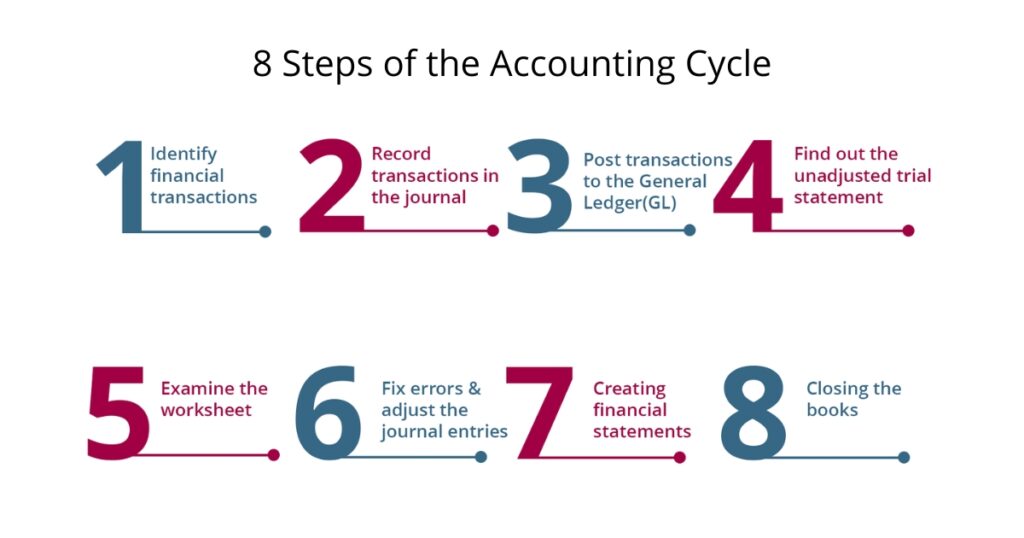

The accounting cycle typically encompasses these steps: identifying transactions, journalizing transactions, posting to the general ledger, preparing a trial balance, preparing the worksheet, preparing financial statements, and closing the books. These are the steps students are taught in most introductory courses. The ambiguity arises when additional steps, or subsets of these steps, are introduced.

For example, some sources include "adjusting entries" as a separate step, while others incorporate it into the financial statement preparation phase. The lack of a universally accepted definitive list is the core problem, creating opportunities for misinterpretation and error.

Differing Interpretations Fuel Uncertainty

Expert opinions on the 'correct' answer are also divided. Some accountants argue that certain sub-processes, like preparing a bank reconciliation or performing an audit, are not integral parts of the core accounting cycle. Others assert that these are essential components, especially in larger organizations.

Dr. Anya Sharma, a Professor of Accounting at State University, stated, "The problem isn't the accounting cycle itself, but rather how it's being presented. Students need to understand the underlying principles and adapt their understanding based on the context, something textbooks often fail to emphasize."

The Impact on Professional Practice

The confusion isn't confined to academic settings. Concerns are emerging about the potential impact on the accuracy of financial reporting in the professional world. Entry-level accountants grappling with these inconsistencies may inadvertently misinterpret financial data.

Accountancy firms are reporting increased time spent training recent graduates on the practical application of the accounting cycle. This added training burden represents a financial cost and highlights the need for clarity in accounting education.

The American Institute of Certified Public Accountants (AICPA) acknowledged the issue and announced they will review curriculum guidelines to address these ambiguities. “We recognize the need for clearer, more consistent educational materials. Our goal is to equip future accountants with the knowledge and skills they need to succeed," said a representative.

Moving Forward: Seeking Clarity and Consistency

The NAAS is planning a series of webinars and workshops designed to address this issue and provide students with practical guidance. These sessions will focus on critical thinking and application of accounting principles in diverse scenarios.

Accounting educators are being urged to re-evaluate their teaching methods and emphasize the importance of contextual understanding. The objective is to move beyond rote memorization and foster a deeper comprehension of the accounting cycle's underlying principles.

The AICPA review is expected to be completed within the next six months. The recommendations from this review could significantly impact accounting education standards and professional practices nationwide. The situation remains fluid, but the focus is now on achieving greater clarity and consistency in how the accounting cycle is taught and applied.