Same Day Installment Loans No Credit Check

The rise of same day installment loans, marketed with "no credit check" promises, is prompting both scrutiny and accessibility for individuals facing immediate financial needs. These loans offer a seemingly quick solution, but consumer advocates and financial experts are raising concerns about potential risks.

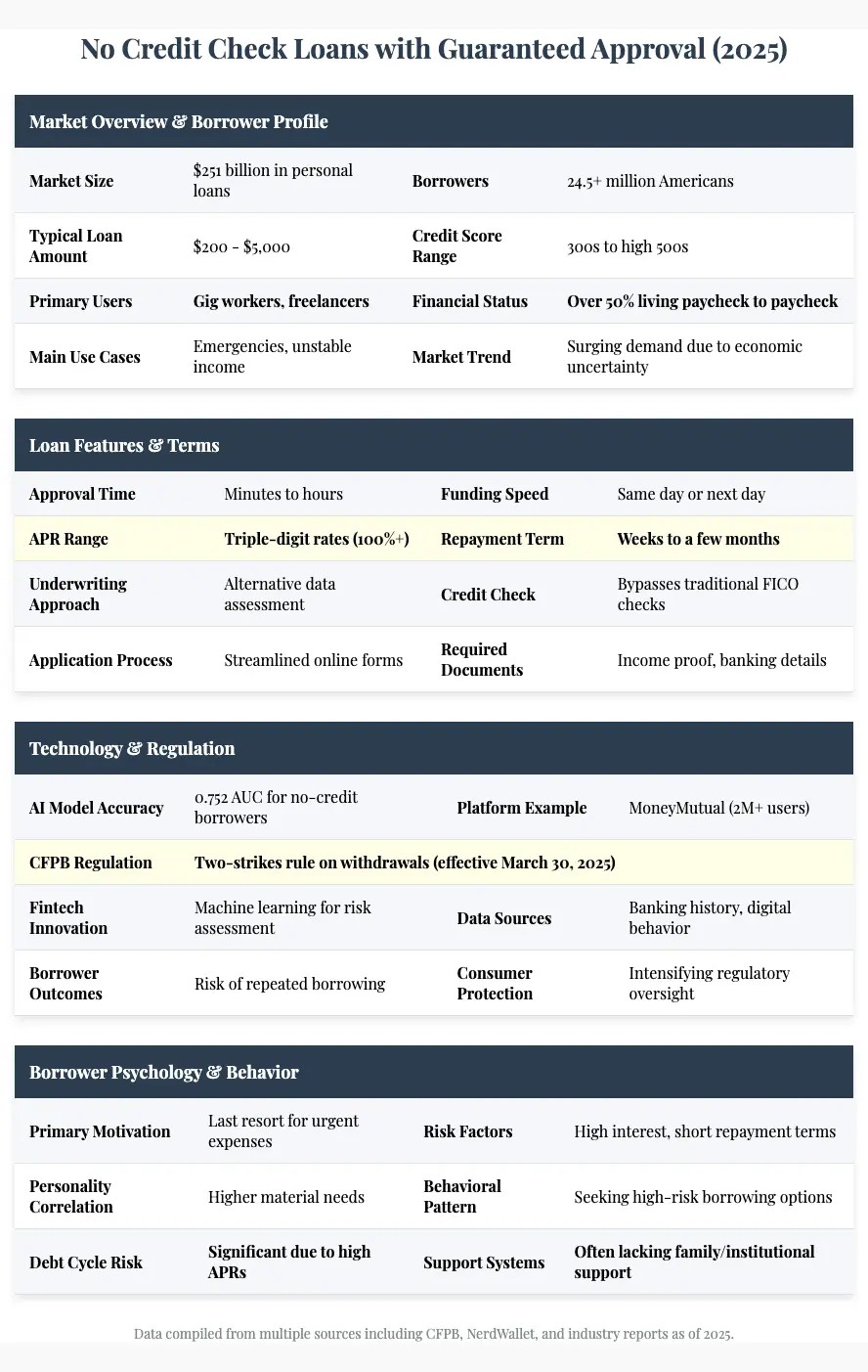

These financial products, offered by a variety of online and storefront lenders, provide borrowers with funds in a lump sum, repaid over a fixed period in scheduled installments. The key selling point is the absence of a traditional credit check, potentially attracting individuals with poor or limited credit histories.

The Appeal and the Reality

The demand for quick access to funds is undeniable, especially for unexpected expenses like medical bills, car repairs, or urgent home repairs. Many individuals find traditional bank loans inaccessible due to stringent credit requirements.

Proponents argue that these loans offer a lifeline to those underserved by mainstream financial institutions. They provide a short-term solution to bridge financial gaps.

However, the "no credit check" aspect often comes with significantly higher interest rates and fees compared to traditional loans. This can lead to a cycle of debt for vulnerable borrowers.

How They Work: A Closer Look

Lenders offering same day installment loans without credit checks typically rely on alternative methods to assess risk. This can include verifying income, employment history, and bank account information.

The application process is generally streamlined, often completed online or through a short in-person visit. Loan amounts can range from a few hundred to several thousand dollars, depending on the lender and the borrower's perceived ability to repay.

Repayment terms vary, but are often shorter than traditional installment loans. This necessitates larger, more frequent payments, which can strain borrowers' budgets.

Concerns and Criticisms

Consumer advocacy groups express serious concerns about the predatory nature of some same day installment loans. The high interest rates and fees can trap borrowers in a cycle of debt.

The lack of a credit check does not necessarily mean responsible lending practices are being followed. Some lenders may not adequately assess a borrower's ability to repay, leading to defaults and further financial hardship.

The Consumer Financial Protection Bureau (CFPB) has voiced concerns about the potential for exploitation in the short-term lending market. They are advocating for greater transparency and stricter regulations.

The Regulatory Landscape

The regulation of same day installment loans varies significantly from state to state. Some states have strict usury laws that limit interest rates, while others have more lenient regulations.

Many lenders operate online, making it challenging for state regulators to enforce consumer protection laws. This creates opportunities for unscrupulous lenders to exploit loopholes and target vulnerable populations.

Federal agencies like the Federal Trade Commission (FTC) also play a role in protecting consumers from deceptive lending practices. They can take action against lenders who engage in false advertising or unfair lending terms.

Impact on Borrowers and the Economy

The availability of same day installment loans can have both positive and negative impacts on borrowers. For some, they provide a crucial safety net during times of financial distress.

However, for others, these loans can lead to a spiral of debt, negatively impacting their credit scores and overall financial well-being. This can have broader economic consequences, affecting household spending and financial stability.

The potential for increased debt and financial instability raises concerns about the long-term impact of these loans on communities and the overall economy.

Navigating the Options: Advice for Consumers

Before taking out a same day installment loan, consumers should carefully consider all their options. Explore alternatives such as borrowing from friends or family, negotiating payment plans with creditors, or seeking assistance from non-profit credit counseling agencies.

Read the fine print and understand the terms and conditions of the loan, including the interest rate, fees, and repayment schedule. Be wary of lenders who are not transparent about their fees or who pressure you into borrowing more than you need.

If you are struggling to repay a same day installment loan, seek help from a qualified financial advisor or credit counselor. They can help you develop a budget, negotiate with lenders, and explore debt relief options.

A Human Perspective

Consider the story of Maria Rodriguez, a single mother who turned to a same day installment loan to cover an unexpected car repair. While the loan allowed her to get back to work quickly, the high interest rate made it difficult to repay. She found herself taking out additional loans to cover the initial debt, leading to a cycle of financial stress.

Maria's experience highlights the potential pitfalls of these loans, even for those who initially intend to use them responsibly. Her story serves as a cautionary tale for others considering this option.

The Future of Same Day Installment Loans

The future of same day installment loans will likely depend on the ongoing debate between accessibility and consumer protection. Increased regulation and greater transparency are likely to be key factors in shaping the market.

Technology may also play a role, with the development of alternative credit scoring models and more responsible lending platforms. These innovations could potentially offer safer and more affordable options for borrowers with limited credit histories.

Ultimately, the challenge is to find a balance between providing access to credit for those who need it, while protecting consumers from predatory lending practices. This requires a multi-faceted approach involving regulators, lenders, and consumer advocates.